|

|

Post by Entendance on Apr 13, 2017 17:33:18 GMT -5

"Why did Endeavour’s share price fall 25% in just one day in early March?"  ***Endeavour Silver CEO Bradford Cooke comments on share price ***Endeavour Silver CEO Bradford Cooke comments on share price

Below is a very interesting article (in case you have not seen it) on how the GDXJ is now running into problems due to the size of the companies in the index. According to the story, Van Eck, which runs both GDX and GDXJ, is now funneling money into GDX when money comes into GDXJ because GDXJ is now an 18% holder of several index members. Seems like this is the classic "index tracking" issue you have been talking about. With 35% of GDX comprised of Barrick, Newmont, Goldcorp and Newcrest, it appears the GDXJ has gotten away from a proxy for the junior sector.

***How An ETF Gets Too Big For Its Index

Ok so I have 1 observation and 1 question:

Observation: I find it incredible that the GDXJ is having problems with only $3.3 billion of inflows since 1/1/2016 that it is has had to put 25% of its assets in 5 holdings that fall outside of its mandate. (I am assuming this means GDX and 4 intermediate to senior gold stocks.)

Question: What do think are Van Eck's options? Since it is very unlikely to close it off to new money, do you think it will do more of the same or will it open a slightly different new fund? Thanks

Fleck: There isn't any real market cap in this sector... When it finally gets really popular, the fireworks will be huge. It will be difficult to stay aboard the train, I suspect.. I dislike both GDX and GDXJ, an Eck will do whatever makes IT the most money. I concur with you.

"...The Deep State looters are mono-maniacally focused on regularly smashing precious metals prices for two primary reasons:

1) It provides them with a vast, recurring, no-lose, totally-illegal-but-never-prosecuted profit source; and,

2) it is an extremely effective way for them to scare everyday citizens away from metals, which is a key DS objective.

If the people ever figure out, en masse, that they would greatly benefit by transferring their money into physical precious metals, as opposed to keeping it in digital bank accounts that can be seized at any time and under any pretext, the Deep State’s looting opportunity will be reduced.

The Deep State works 60x60x24x365, or every second of every day to prevent the people from having that “Aha Moment” of personal financial clarity and sanity.

If the people fully understood how resilient precious metals prices have been despite the constant, multi-year, 24 hour per day, criminal, full-spectrum Deep State manipulation campaign, they would gain a new-found respect for precious metals as assets. Greed-fueled frauds always collapse in time, and when the precious metals price manipulation fraud fails, gold, silver and platinum’s reflexive revaluation will almost certainly be historic.

The Deep State agenda is to eliminate cash as soon as possible and force the people’s money to become nothing but electrons housed in digital currency prisons euphemistically called banks. Next, they will deactivate the precious metals dealers’ bank accounts, making it extremely difficult for citizens who have not already done so to acquire precious metals. This action will be taken under the totally dishonest pretext of combating drugs, crime, terrorism and other fake, so-called dreaded threats. When people get wind that this is coming, a precious metals buying stampede will break out, much the same way that the ammunition buying frenzy developed when rumors spread that Obama was going to sharply control, turbo-tax or even prohibit bullet sales. Time and time again throughout history, people have exhibited a passionate desire to buy the things they expect will be taken away from them. When the precious metals buying stampede is triggered, people throughout the west will learn in a hurry that the quantity of physical precious metals actually available to them is extremely limited and quickly vanishing. Supplies will completely disappear in a day or two, if not before, just as ammunition disappeared from the shelves, nationwide, during that buying explosion..." More here

|

|

|

|

Post by Entendance on May 8, 2017 8:31:06 GMT -5

Apr. 26, 2017 12:22 PM ET EXK Endeavour Silver - Silver Producer With Near-Term Growth Potential

Endeavour Silver beats by $0.04, beats on revenue May 3, 2017

EXK Endeavour Silver Reports First Quarter, 2017 Financial ResultsEndeavour Silver Corp (NYSE:EXK)

Q1 2017 Results Conference Call May 03, 2017 12:00 PM ET

Executives

Meg Brown - Investor Relations

Brad Cooke - CEO

Godfrey Wilson - President & COO

Dan Dickson - CFO

Analysts

Justin Stevens - Raymond James

Meg Brown

Good morning everyone and welcome to the Endeavour Silver Q1 Earnings Conference Call. On the call today, we have the company's CEO Brad Cooke as well as our President and COO Godfrey Wilson, and our CFO Dan Dickson.

Before we get started, I'm required to remind you that certain statements on this call will contain forward-looking information within the meaning of applicable Securities Laws. These may include statements regarding Endeavour's anticipated performance in 2017 and future years, including revenue and cost forecasts, silver and gold production, grades and recoveries, and the timing and expenditures required to develop new mines in mineralized zones. The Company does not intend to and does not assume any obligation to update such forward-looking statements or information other than as required by applicable law.

With that, I'll turn the call over to our CEO Brad Cooke.

Brad Cooke

Great thanks Meg, and welcome everybody to this Q1 conference call on our financial results. Our financial performance in the first quarter was actually sharply improved compared to the first quarter of last year and even though revenue and cost of sales were down due to lower production our earnings were up as a result of the higher precious metal prices, foreign exchange gains and tax recoveries. That earnings actually increased 230% to $6 million on the quarter. EBITDA was up 4% to $9 million, cash flow from operations increased 19% to $8.9 million and revenues decreased 12% to $36.4 million. Our sales actually averaged between 2 and 5% above average spot prices for silver and gold respectively. And our cash cost relatively flat up only 2% at $7.81 per ounce of silver payable metal to growth credit.

All in sustaining cost however were up 64% to $18.24 per ounce reflecting our willingness to reinvest our free cash flow to extend mine lives and grow resources. Cash was relatively flat though only 2.5% to $17.5 million on the quarter and working capital is flat at $81.9 million. Generally looking at the individual operations we enjoyed strong free cash flow at Bolanitos. We had a modest profit Cubo and a modest loss at Guanacevi. Guanacevi is actually the only mine underperforming it’s plan, it’s still very much a work in progress, recovering from some operating issues that we had last year and there's still clearly work to do to get Guanacevi back to good health.

We are however seeing rise in our Bolanitos tonnage and slow rise in our Cubo grades coming into the second quarter. So we are hopeful that those two mines will outperform their plans this year. Q1 was also a very busy time for us on a development projects. We released preliminary economic assessment for the El Compos mine which is scheduled to become our fourth mine. We hope to receive the exposes covered by the end of the quarter, break ground and see initial production by year end. That preliminary economic assessment report should be filed and available on SEDAR by May 11th. We're also very busy on our Teranera project which we hope will become mine number five. Production decisions still to be taken there as we wait for and work on the environmental permits, debt financing to help facilitate the construction of Teranera and related issues and opportunities. That report the pre-feasibility report on Teranera should actually be filed on or before May 18th. So I think operator that's the highlights for the quarter. Why don't we open this up for Q&A?

Justin Stevens

Morning guys, just a few questions from me. In terms of grade the Bolanitos there are sort of lower silver higher gold than what we were anticipating. Is the Q1 grades sort of what we're going to be looking at going forward here from that one.

Brad Cooke

Sorry, grades going forward Justin, this is Godfrey.

Justin Stevens

Yes, Bolanitos.

Brad Cooke

At Bolanitos. We were a little bit slower getting into Pateros which is why the grades were lower than we anticipated as well but we've come through some operational delicate areas and we should be back into Pateros in full steam this quarter and so you should see the grades coming up back to what they were scheduled to be.

Justin Stevens

Sounds good, and just also on the cost side, patented things very well I think but are these cost per ton sort of what we're expecting going forward here.

Dan Dickson

Justin this is Dan, those costs per ton are relatively in line with what we expect in line with our budget for the year, I'd said Guanacevi because the lower production had higher cost per ton, so if we can improve the production tonnage throughout the year we should see those cost per ton come down.

Justin Stevens

Sounds good, and just on the sort of M&A front or at least land acquisition side, are you guys looking at all to sort of pick up or consolidate new line packages, I mean if you've got a bit of extra cash to throw around.

Brad Cooke

Hi Justin, it's Brad again. We're always active on the M&A front, you know from time to time we pull the trigger on acquisitions last year we did two El Compos and Paral. Within the districts of the existing three mines we're always looking to acquire properties and expand our land positions in these districts and I think there's certainly an opportunity to do more of that this year, particularly at Guanacevi and Bolanitos and to a lesser extent at Cubo. And you know for the development projects we've also been active on expanding our footprint. So news on that later this year.

Justin Stevens

That was good, that's it from me, thanks guys.

Brad Cooke

Thanks Justin.

Brad Cooke

Well you guys are letting us off easy this quarter must have been good news. Thank you operator, and thanks to everybody for listening in. let’s have a quick look ahead to Q2, obviously we're still very active on the exploration front with I think currently five or six drills working and we're taking a break on some of the drills just to collate results. It is reasonable however to expect some news from Paral this quarter perhaps another news release on Teranera. We've got some land acquisitions I think might be ready in the [indiscernible] district and as the operations continue to improve we're obviously hoping that Q2 will look better than Q1. So I think we're on track for another decent quarter and we look forward to chatting in early July on our operating results. Thanks all for joining us and we'll turn this back over to the operator.

May 4, 2017

EXK Endeavour Silver Announces 2017 Annual General Meeting Results

|

|

|

|

Post by Entendance on May 10, 2017 8:31:04 GMT -5

Simon Black: <His remarks started off like dozens of presentations that I had heard so many times before. . .

“Without silver,” began the speaker, “our entire society would go back to the Stone Age.”

The speaker was the CEO of one of the largest silver mining companies in the world, and he was a special keynote at the annual closed-door meeting of the Atlas 400.

CEOs of mining companies almost always start their presentations talking about how important their mineral is.

“If we didn’t have cobalt we would all be cave men again. . .” or “Without molybdenum our modern technology would cease to exist.”

It sounds impressive, but the same story applies to just about every industrial commodity in the world, from copper to lumber to recycled steel.

It’s hardly an original argument and doesn’t impress me enough to be bullish on their mineral.

The real investment thesis about silver is that it’s a precious metal that has industrial qualities and a long-standing tradition of value.

Like gold, silver was an ancient form of money. And for good reason.

Out of the 118 known elements that exist on the periodic table, gold and silver share certain chemical properties that made them ideal as a medium of exchange to our ancestors.

Gold and silver are solid at normal temperatures (as opposed to Helium). They’re not radioactive (like Plutonium).

They’re not explosive when they come into contact with water (like Cesium), nor do they rust when they get wet (like Iron).

Most importantly, gold and silver are rare enough to be valuable, but not so rare that it would be almost impossible to mine more.

Between the two, gold is obviously more rare… hence the higher price.

There’s an old estimate from the US Geological Survey from the late 1960s suggesting that the ratio of silver to gold in the earth’s crust is about 21:1.

(So assuming that’s true, the theoretical price ratio between the two should be around 21:1)

And in ancient times the price ratio between the two metals was frequently in the range of about 15:1, i.e. one ounce of gold was worth 15 ounces of silver.

Today the ratio is about 75, based on a gold price of about $1230 per ounce, and a silver price of $16.35.

This is fairly high even by modern standards as the long-term average over the past several decades is about 50.

This would suggest that silver should in increase in price relative to gold in order for the ratio to return to its historic average.

(A ratio of 50:1 would imply a silver price of $24.60 based on a gold price of $1230.)

Now, all of this is an argument that many of us have heard before.

But I did learn something over the weekend from the mining CEO; he told us that the current mining production ratio between the two metals is about 9:1.

This means that 9 ounces of silver are mined for every 1 ounce of gold that’s mined.

This is very interesting from a supply/demand perspective.

According to the Silver Institute, demand for silver hit an all-time high in 2016.

But the price of silver, at least relative to gold, is hovering near a multi-year low at 75:1. (Again, the historic average is around 50:1).

Moreover, even though the price is 75:1, the new supply of silver is only 9:1.

In theory if the new metal supply is 9:1, then the price should be 9:1 (which would be a silver price of $136.67).

Obviously that’s a purely academic postulate; reality rarely conforms to theory. And the mining CEO wasn’t projecting a $136+ silver price.

But it seemed clear to him that there’s an unsustainably wide gulf between the gold/silver price ratio versus the gold/silver supply ratio, especially when silver demand is at an all-time high.

Commodity prices tend to move dramatically when the market realizes there’s a serious supply/demand mismatch.

That seems to be the case with silver right now.

And while it would be silly to expect $100+ silver, there are certainly credible reasons why the ratio should close the gap and move MUCH lower.>

|

|

|

|

Post by Entendance on May 18, 2017 7:01:03 GMT -5

|

|

|

|

Post by Entendance on May 19, 2017 11:58:04 GMT -5

|

|

|

|

Post by Entendance on Jun 6, 2017 6:04:12 GMT -5

June 6, 2017

EXK Endeavour Silver Acquires Additional Properties in Zacatecas, Mexico

Vancouver, Canada – June 6, 2017 - Endeavour Silver Corp. (TSX: EDR, NYSE: EXK) announces it has acquired 100% interests in two small but prospective mineral property groups, Calicanto and Veta Grande, located in the historic silver mining district of Zacatecas in Zacatecas state, Mexico. For map click here.

All of the properties host old mines and/or known silver-gold veins that were underexplored by modern methods and are being acquired for their near-term mine exploration and development potential, given their proximity to Endeavour’s El Compas Mine and La Plata plant, also located in the Zacatecas district.

Bradford Cooke, Endeavour CEO and Director, stated: “We are very happy to add these new properties to our exploration portfolio in Zacatecas. The two transactions confirm there are good opportunities to consolidate a larger mineral land position in Zacatecas, one of the largest historic silver mining districts in Mexico. Drilling is now underway at the Calicanto properties and we expect to permit and drill the Veta Grande properties later this year.”

Note that all technical data reported in this news release are historical in nature and Endeavour Silver has not independently verified them; therefore, these data should not be relied upon.

Calicanto Properties

The Calicanto properties were purchased from Arian Silver Corporation for US$400,000. They cover 75 hectares over five known, silver-gold-lead-zinc veins – Calicanto, Vicochea, Nevada, Misie and Buenaventura – within an area of 1.2 by 1.2 kilometres (km).

The veins were discovered around 1600, and supported small scale, high-grade production of silver off and on for about 350 years. The mines were historically developed down to approximately 150 metres (m) depth by seven old shallow shafts, and they were closed in the mid 1950s. The upper mine workings are still open but the lower mine workings are now flooded.

In the past 10 years, Arian drove two short ramps into the Calicanto and Buenaventura veins, drilled 16 core holes totaling 3,149 m with encouraging results. Highlights of the properties are as follows:

Calicanto Highlights

•100% interest subject to a 3% NSR royalty

•Well located and readily accessible adjacent to both the city of Zacatecas and the access road to Endeavour’s recently leased La Plata 500 tonne per day (tpd) government plant

•Excellent infrastructure including grid power, water, labour, and services, with a land access agreement already in place for exploration and exploitation

•Five veins each with histories of small scale production, each traceable for over one km, averaging 1-3 m thick containing mineralized zones grading 100-300 grams per tonne (gpt) silver, 1-3 gpt gold, 1-3% lead-zinc

•Historic resources previously estimated in the Calicanto vein from underground sampling by SGM, the government geological survey

•Positive drill results by Arian included intercepts grading 8.54 gpt gold and 97 gpt silver over 4.50 m true width in the Calicanto vein, 7.17 gpt gold and 1,055 gpt silver over 4.70 m at Misie, and 0.9 gpt gold and 409 gpt silver over 1.60 m at Vicochea

•Potential to add new, shallow, small scale but high-grade resources in four veins by additional drilling along strike and down dip and develop near term production close to our plant in a stable, attractive jurisdiction with great infrastructure and no known social or security issues

•Positive synergies with Endeavour’s El Compas mine development project in Zacatecas

Veta Grande Properties

The Veta Grande properties were purchased from IMPACT Silver Corp. for US$500,000 by issuing 154,321 Endeavour common shares at US$3.24 per share. They cover 152 hectares over six known, silver-gold-lead-zinc veins plus 14 hectares of surface lands covering the dormant Santa Gabriela 200 tpd processing plant and tailings facility.

The properties are located in the vicinity of one of the largest veins in the Zacatecas district, the Veta Grande vein, and cover the Nueva Granada splays to the Veta Grande vein and several other subparallel veins. The properties saw historic, small scale, high-grade production as shown by old mine workings and dumps. Access to the old workings is limited and many are now flooded, but historic sampling of dumps and trenches returned values up to 1,070 gpt silver with significant lead and zinc values.

The Santa Gabriela processing plant is located adjacent to Endeavour’s La Plata plant five km north of the city of Zacatecas and it last operated between 2006 and 2009 as a 200 tpd flotation toll mill. The plant has been dormant since that time and none of the concessions have seen modern exploration.

Veta Grande Highlights

•100% interest with no underlying royalty

•Well located and readily accessible adjacent to both the City of Zacatecas and the access road to Endeavour’s recently leased La Plata 500 tpd government plant

•Excellent infrastructure including existing tailings storage facility, grid power, water, labour, and services

•Several vein systems each with histories of small scale production, each traceable for over one km, averaging 1-3 m thick containing high grade mineralized zones ◦The Nueva Granada concession covers the main San Jose and Armado splay veins off Veta Grande. Historic samples from the San Jose vein returned values ranging to a high of 444 gpt Ag over 1.10 m (true width) in channel samples (average 239 gpt Ag over 0.74 m true width) and up to 1,070 gpt Ag in old mine dumps (average 407 gpt Ag). The Armado vein trends 100 m west and runs parallel to the San Jose vein. Historic channel samples collected from the surface exposures of the Armado vein assayed 237 gpt Ag over 1.92 m (true width) and 1,320 gpt Ag over 0.30 m (true width). Sulphide bearing samples from old mine dumps assayed up to 358 gpt Ag. In addition, several other splay veins branch off Armado providing additional exploration targets.

◦The Anaconda Group of concessions cover portions of historic veins that trend parallel to the main Veta Grande vein, many of which have seen historic, small scale production. Historic samples from surface dumps returned 310 gpt Ag, 24.2% Pb and 8% Zn from a high-grade stockpile.

◦The San Pascual concession is the site of the historic San Pascual Mine which last saw small scale production over 20 years ago. The shaft is flooded, however historic sampling of mine dumps adjacent to the shaft returned 875 gpt Ag. Samples from other dumps assayed 525 gpt Ag.

◦The Alianza vein lies on the Alianza concession where historic production was reported to grade 4 gpt Au, 400 gpt Ag, 3% Pb and 2% Zn.

◦The Cancer concession hosts the Providencia vein. A large adit exposes a 1.25 m wide vein with silicified breccias where historic samples from dumps and vein material returned up to 649 gpt Ag.

◦The contiguous Milagro and Leo concessions lies approximately 500 m north of the Cantera Vein system, one of the three principle veins in the Zacatecas silver district; the others being Mala Noche and Veta Grande. Samples from surface exposure of veins and old mine workings returned values averaging 158 gpt Ag.

•Potential to add new, shallow, high-grade resources from numerous veins by drilling along strike and down dip and develop near term production close to the La Plata plant in a stable, attractive jurisdiction with great infrastructure and no known social or security issues

•Positive synergies with Endeavour’s El Compas mine development project in Zacatecas

Mr. Dale Mah, B.Sc., P.Geo., is the Qualified Person who reviewed and approved the technical disclosure in this news release.

About Endeavour

Endeavour Silver is a mid-tier precious metals mining company that owns three high grade, underground, silver-gold mines in Mexico. Since start-up in 2004, Endeavour has grown its mining operations organically to produce 9.7 million ounces of silver and equivalents in 2016. We find, build and operate quality silver mines in a sustainable way to create real value for all stakeholders. Endeavour Silver’s shares trade on the TSX (EDR) and the NYSE (EXK).

Contact Information - For more information, please contact:

Meghan Brown, Director Investor Relations

Toll free: (877) 685-9775

Tel: (604) 640-4804

Fax: (604) 685-9744

Email: mbrown@edrsilver.com

Website: www.edrsilver.com

EXK Endeavour Silver Corp mentioned in the new In Gold We Trust 2017 Report!

Extended & Compact Version (Vollständige & Kürzere Version) here

|

|

|

|

Post by Entendance on Jul 12, 2017 6:14:11 GMT -5

EXK Endeavour Silver Produces 1,143,788 oz Silver and 13,058 oz Gold (2.1 Million oz Silver Equivalents) in the Second Quarter, 2017

Endeavour Silver Corp. (TSX: EDR) (NYSE: EXK) reports its production results for the Second Quarter, 2017 from the Company's three silver-gold mines in Mexico: the Guanaceví mine in Durango State and the Bolañitos and El Cubo mines in Guanajuato State. Silver production in the Second Quarter, 2017 was 1,143,788 ounces (oz) and gold production was 13,057 oz resulting in silver equivalent production of 2.1 million oz using a 70:1 silver gold ratio.

Production was lower in Q2, 2017 compared to Q2, 2016 due to differences in the annual mine plans. Last year (2016), production was highest in Q1 and lowest in Q4 due to the decision at low metal prices in January 2016 to cut spending on exploration and development at all three mines, which reduced mine access to reserves and therefore reduced metal production.

In 2017, production was higher in Q2 compared to Q1 due to improved performance of the Bolañitos and El Cubo mines. This year, consolidated production should rise from Q1 to Q4 with increased access to reserves due to increased spending on exploration and development at all three mines.

Production Highlights for Second Quarter, 2017 (Compared to Second Quarter, 2016)

•Silver production decreased 26% to 1,143,788 oz

•Gold production decreased 17% to 13,058 oz

•Silver equivalent production was 2.1 million oz (at a 70:1 silver: gold ratio)

•Silver oz sold down 34% to 988,821 oz

•Gold oz sold down 20% to 12,294 oz

•Bullion inventory at quarter-end included 226,437 oz silver and 631 oz gold

•Concentrate inventory at quarter-end included 50,644 oz silver and 890 oz gold

Endeavour CEO Bradford Cooke commented, "Our second quarter production was an improvement over the first quarter thanks to higher tonnes and/or grades from the Bolañitos and El Cubo mines. Both mines are now performing in line with their operating plans for the year. The Guanaceví mine continues to lag behind plan and an internal review has been initiated in order to identify additional actions needed to improve tonnes and/or grades and production.

"We recently made a decision to develop El Compas as our fourth mine and work is now under way on developing the mine ramp to access the orebodies. We also received notice of approval for our mine and plant permits from SEMARNAT last week to build Terronera into our fifth mine. The SEMARNAT and CONAGUA waste dumps and tailings area permits for Terronera are expected later this year."

At Guanaceví, slower mine development due to narrower vein widths than in the resource model resulted in lower mine output than planned, while excess dilution of the ore resulted in lower than planned grades. Management has initiated an internal review of the Guanaceví mine plan and reserve estimate to better understand the variance in production compared to plan in recent months. Over the past year, management has implemented operational changes and made investments to improve the pumping, ventilation and electrical systems at Guanaceví to remediate the operational challenges encountered in the second half of 2016 and first half of 2017.

At Bolañitos, silver grades improved but remained below plan due to grade variations in the LL-Asunción vein. The lower silver grades were offset by higher throughput than planned. Gold production exceeded plan due to higher throughput and gold grades.

At El Cubo, both silver and gold grades were higher than plan, and throughput was slightly below plan. During the quarter, management made changes to both mining methods and ore control processes to reduce the dilution and provide higher-grade material to the plant. Grades are expected to stabilize and throughput should regain plan through year-end.

Production Tables for Second Quarter, 2017 HERE Production Tables for Six Months Ended June 30, 2017 HERE

Release of Second Quarter, 2017 Financial Results and Conference Call

The Second Quarter, 2017 financial results will be released before market on Thursday, August 3, 2017 and a telephone conference call will be held the same day at 10:00am PDT (1:00pm EDT). To participate in the conference call, please dial the numbers below. No pass-code is necessary.

Toll-free in Canada and the US: 1-800-319-4610

Local Vancouver: 604-638-5340

Outside of Canada and the US: +604-638-5340

|

|

|

|

Post by Entendance on Aug 5, 2017 2:10:00 GMT -5

EXK Q2 2017 Earnings Conference Call August 3, 2017 1:00 PM ET

Executives

Meghan Brown - Director Investor Relations

Bradford Cooke - Chief Executive Officer

Godfrey Walton - President and Chief Operating Officer

Dan Dickson - Chief Financial Officer

Analysts

Heiko Ihle - Rodman & Renshaw

Malcolm Gissen - First Republic

Bruce Zipper - Dakota Securities International

Bradford Cooke

Welcome, everybody, to this Q2 financial results call. As you saw from our news today, our second quarter financial performance was impacted by lower metal prices, lower production and increased exploration and development spending. I guess, the good news is that, the production increased incrementally from Q1 to Q2, and we expect that to continue from the first-half to the second-half, as we increase access to reserves at all 3 mines.

The result of slightly higher production in Q2 compared to Q1 was thanks to improving performance at the Bolañitos and El Cubo mines, but Guanaceví continues to lag behind plan and has been struggling with a number of issues, not the same old issues, but new ones that keep popping up.

So let’s look at the financial performance, first of all. On an net earnings base, we basically broken even in the quarter. EBITDA was down to $3.7 million, and cash flow down to $4.4 million, revenue down to $32.7 million, all thanks to the combination of slightly lower production and lower metal prices.

Cash costs were up to $8.36 per ounce of silver, net of the gold credit, that’s due to the operating issues at Guanaceví. And all-in sustaining costs were up to $20.46 per ounce of silver, again, a combination of operating issues at Guanaceví plus our increased spending to extend mine life at all three mines. Interestingly, enough compared to the end of the year and even with paying down debt, our working capital has only decreased by about 8%. We are currently sitting on $75 million in working capital.

So let’s talk about Guanaceví. Last year, we had a number of issues related to breaking into effectively a hot water spring underground, which caused power outages, pump failures and some flooding. We had just recovered from that when we encountered similar problems this year.

In fact, even in July for a third time, we had a repeat of our electrical issues and pump failures and flooding of some of the deeper workings. So it’s one thing after another at Guanaceví. We have recently completed yet another repair of the electrical and ventilation systems. There is completion now of construction of a new underground pump station and all those things should help smooth our production coming into the second-half of the year at Guanaceví.

It’s pretty clear though, given the setbacks we’ve had since the start of the year that we are not going to meet our planned guidance at Guanaceví. And so we’ve accordingly reduced our consolidated production guidance and raised our consolidated cost guidance.

Let’s talk briefly about the development projects. At El Compas, work has begin on installing the project infrastructure, collaring the mine access ramp and refurbishing the plant. There’s ongoing refinements to the project engineering, optimization studies are underway on various mining methods and crushing and grinding alternatives.

We have, however, postponed not for very much time, but we’ve had to delay the anticipated commissioning of our mining plant in the first quarter, specifically due to delays in our explosives permit. And that’s government-wide permitting slowdown that we’ve seen at all of our permitting applications in Mexico, so that applies to Terronera as well.

Speaking of which work is currently focused on refining our project engineering and optimization studies at Terronera, looking at different mining methods, crushing and grinding alternatives and power options, and like El Compas, mine and plant commissioning has been delayed into 2019.

So our revised guidance is now somewhere around 5 million ounces of silver production, 50,000 ounces of gold production, 8.7 million ounces of silver equivalent production for the year, plus or minus.

Heiko Ihle of Rodman

Listen, you had in there, excuse me, that there was slower than planned mine development due to narrow vein biz at Guanaceví. Has this – is this continuing? Is this accord from the ore body, sort of walk in on geologists through how this happened?

Bradford Cooke

Well, apparently at every year-end, we do resource modeling and that’s how we reestimate reserves and resources. What we are finding in the deepest levels of the Santa Cruz mine at Guanaceví, and this is something that’s come up just in the last quarter is that, we couldn’t reconcile the model with what we are seeing underground. And we’ve – since then both in internal reconciliation and we asked the independent consultants, Hardrock, to come back and reassess their model. And then the conclusion is that, there was an overestimation of width and to a lesser extent grade in the deeper levels of Santa Cruz.

So it – strictly speaking, obviously impacts what we were expecting to see in reserves for 2017. I guess, the only ray of light is that, we’ve been drilling and expanding that area in terms of reserve for placement and resource expansion. So the net-net effect may be neutral based on exploration successes. But it’s one of the factors that really held back our production this year, narrow width there.

Heiko Ihle

With the flooding at Guanaceví, can you just sort of walk us through how many meters got flooded, the pumping capacity at the site, just so to quantify it a little bit?

Bradford Cooke

Well, it’s not that the capacity has changed, it’s – the system – we had dozen small pumps and pump stations to lift the water, effectively 600 meters vertical to surface. And with the completion of a new and much larger pump station, we are now looking at only two lifts from the deepest levels to surface. And so that’s a significant increase in productivity and decrease in cost, decrease in power consumption, et cetera. So that pump station is just coming on this week.

Heiko Ihle

But quantify the pumping capacity?

Bradford Cooke

Godfrey, do you have the amount out of water we’re pumping?

Godfrey Walton

I don’t actually have the actual amount of water. But we are about 400 meters below the water table, that have been like for several years. So it’s been the – over time, we’ve added a pump as each level goes down, and that’s why the efficiencies and all the electrical issues that we’ve had. Typically, when we have a power issue, we will end up with two or three levels to get flooded. And then it takes us about a week to take – to dry up those two or three levels each time.

So – and in June, we had a lightning strike on one of our power lines and that knocked out the electrical system in the mine. Although, we do have backup generators, it will only cover part of the total electrical need for the mine.

Heiko Ihle

Yes.

Godfrey Walton

So, everything else is – with the refinements and the electrical capacity and the pumping, it should be far more efficient.

Heiko Ihle

Got it. Okay. Moving on to Bolañitos, it seems like gold grades came in quite a bit higher than expected. You expect this to continue for the rest of the year? Is there something where we should, maybe amend our models a bit, or was this a Q2 phenomenon and its probably going to come to an end?

Godfrey Walton

Gold grades are definitely higher at Bolañitos. We’ve actually intersected some sections in the Plateros vein that are coming – averaging 5 to 6 grams gold. And so those have been very welcome. But we will find that the silver grades will start coming back to the 100 grams, as we stop mining higher up in the Plateros.

Heiko Ihle

Excellent. Well, thank you, guys, so much for the heads up there. I appreciate it.

Godfrey Walton

Okay.

Bradford Cooke

Yes, thanks, Heiko, just finishing off on Guanaceví, we’ve obviously been wrestling with this mine for a year now. But it’s not – it’s different issues that keep coming up and we keep fixing them. And I think, we are through this latest round of electrical pump and flooding issues. There’s no guarantees that we won’t get hit by lightning again. But we are optimistic that the operations are going to start regularizing themselves and we’ve overcome a number of setbacks.

And I think, even though, it’s not going to meet guidance this year, there’s still a very healthy future for the mine. I mentioned in the news release that the longer-term outlook actually depends on the development of two new ore bodies that were found in recent years, but have yet to be developed.

Development is now underway on the Milache ore body, and we are timing the future development of Santa Cruz Sur to match that, so both come into production midyear next year. And then the Guanaceví will actually look like a very different mine than it does today, both from a production profile and from the cost profile. Let’s move on to...

Malcolm Gissen of First Republic

Hi, Brad. The news has not been terrific and the market undid. What can you do – and you alluded toward a little bit in the comments you made at the end of the last question. What can you do to restore confidence in the market in the management team and your operations after these recurring setbacks?

Bradford Cooke

What we are segueing at Guanaceví from the deep high-cost bottoms of the Santa Cruz and Porvenir Norte mines to the shallower higher-grade tops of the Milache and Santa Cruz Sur mines. And that’s the transition, that will take us another year. But that alone completely remakes the mine. And it could well become one of our more profitable operations within a year.

So we are obviously still thinking, we can help turn the quarter on the existing deep mines, but there’s still a lot of life in the old grill, and like I said, it will look like a very different mine within the next year. We always look to other mines to try and outperform when one mine is struggling. As you recall, we struggled with Cubo for 3.5 years and had some outperformance from Bolañitos the Guanaceví during that time.

So we can’t comment on that now. But both Bolañitos and Cubo are certainly on plan, and we’re constantly looking out for ways to be planned and help our production and our costs.

Bruce Zipper of Dakota Securities International

Can you guys discuss with the guidance that you gave today for the rest of 2017? How that correlates into profitability or lack thereof, give us a little color in that area based on the numbers you think you can do? Bradford Cooke Well, you’ve seen our all-in costs guidance jump from around 15-ish to 16.5.

Bruce Zipper

Yes.

Bradford Cooke

So that’s the impact on profitability is that, we are expecting a slightly less cash flow because of the slightly higher all-in sustaining costs, really halfway through the year though. So, as I mentioned earlier, we are going to continue to look for opportunities to outperform at the other mines and that will help.

Dan Dickson

If I can add that, Bruce, it’s Dan, the CFO. We front-end loaded a lot of our sustaining capital to the first-half of the year. So a lot of that’s come through. A lot of the improvements that we’ve done at Guanaceví is going through our capital investments that impacts all-in sustaining costs. And I know the markets are quite fixated on all-in sustaining costs.

But some of those capital items are going to benefit us for the next three or four years, it’s just that certain metric that the market looks to, it impacts today. And I think it’s important to realize that it’s not just today’s capital, but that capital is going to benefit us hopefully for the next three or four years that we are putting into the ground.

So I think, we need to look at both cash costs and all-in sustaining costs and recognize that we are putting investments back into these mines today, because basically over 2015 and 2016, we reduced our investments to make sure we can get through some of the trough periods in the prices. And hopefully, now we are coming back into a period, where silver price is going to gain, and we are going to try to keep these costs where they are.

Bradford Cooke

And I think, what Dan saying is that the all-in sustaining costs peaked in the second quarter, and we do expect them to decline because the bulk of our all-in sustaining capital has been invested in the first-half. So we are not looking for massive changes in our costs forecast. But if you just do the math on our revised all-in sustaining costs forecast versus the second quarter, obviously costs have to come down to meet our forecast.

Bruce Zipper

Right. Okay. But as far as declines that I have in your company’s stock, can you discuss your balance sheet, your cash in the bank, so on and so forth? How is that continuing to look?

Dan Dickson

Yes, Bruce, we touched on it early on. We have $53 million of cash in the bank and that’s come down from December 31, 2016, as we invested into the long-term future of the company. But our working capital has only come down by $8 million. Today, we sit on $75 million of working capital. At the end of the quarter, we had $4 million in debt, $2.5 million and that’s going to be paid by September 30. So really on a net cash basis, we have $48 million. We are healthy, but we want to take some of that working capital and put into the long-term benefit of the company.

Bruce Zipper

Yes. Well, that’s one of the pluses that we think you’ve got is that balance sheet. One last question, would a healthy balance sheet – I know, things have been rough in the first half, but if there’s an opportunity, you have your eyes on any other prize or potential mines or other companies that might fit into your situation, or is that off the table until things get better?

Bradford Cooke

Well, Bruce, let’s look at three different timeframes. Short-term, I think, the most important things we can do on M&A is actually related to the three operating mines. And I’m working with Dale on additional strategic acquisitions in and around Guanaceví, Bolañitos and El Cubo. And what those acquisitions do is help to extend the mine lives. So

that’s very much in the forefront of our thinking for short-term growth and sustainability.

In terms of medium-term growth, you are well aware of our growth profile. We had acquired some projects last year plus our discovery of Terronera, they are all slated for future development. Two of them, El Compas and Terronera, are already in development. And so we do have, I think, one of the more aggressive growth profiles medium-term in the silver sector.

Long-term, we are acting to look for even bigger and better projects to put into the development pipeline. We have to ask ourselves, what happens when Terronera is up and running? It has the potential to become our largest and certainly one of our lowest-cost mines by 2019. But what about after that?

So Dale and I have been looking at a number of opportunities. It’s a process, obviously. We’ve turned over a lot of stones and kissed a lot of frogs, but none of them have turned into princesses yet. The process continues.

Bruce Zipper

Okay. Well, that’s interesting and I appreciate that comment. And all the best you guys.

Stephen Epstein, a private investor

I just wanted to ask what your thoughts might be on, whatever the changes might be in the metals market going forward up or down, whether it’s significant or trending up or down. How much does that impact your decision to sell your reserves or process them and restore concentrates or sell? Are you able to – or do you want to even deal with that kind of issue, or is that something that you are not even affected by as much, you had process it to go forward with the cash flow? Does that make sense?

Bradford Cooke

First on the metal prices, clearly, we are looking at the bear market of the last 5.5 years, 6 years in the rearview mirror. I think it’s also clear, based on last year’s balance that we are looking at a bull market out the front window. But it hasn’t arrived full bore yet. So we are kind of in an in-between period, a consolidation period, in the precious metal prices. We certainly are bulls. We think that the precious metals only have one way to go over the long-term and that’s upwards.

In terms of how that affects our strategy and our cash flows, well, obviously with low metal prices, our revenues and cash flows and profits are lower than when metal prices are higher. And we, as a strategy every year develop our spending models based on our cash flow models.

So we try to cover all of our spending by our cash flow. That is the sustainability spending, so that only growth spending comes out of cash. And if you recall, we did raise some cash last year that was specifically to fund our growth going forward. And El Compas is fully funded, Terronera is partly funded. But we are not yet breaking ground there and we fully expect to put a small debt facility in place, effectively a bank line of credit to talk up the Terronera financing for full production.

So we typically manage our spending based on our anticipated cash flows and we expect those cash flows to rise. Certainly, next year, we are looking at a bump in production, and we certainly hope there will be a bump in metal prices.

And maybe I’ll ask Dan Dickson, our CFO to say something.

Dan Dickson

Thanks, Brad. Yes, I think, the general sense on the call has been obviously, the Guanaceví and some of the operational issues that we’ve had at Guanaceví, and we hope that we are coming out of that here in the second-half of the year and 2018 will get back to guidance.

I think one of the key things that Brad touched on, on one of the caller’s questions was on restoring confidence in the market. I think one of the important things that we’ve got to realize is, over the last five years, we typically met our guidance. And in this case with Guanaceví having these operational issues is probably the first time in the last five years that we’ve actually had to come out and revise our guidance downwards.

In 2016, we revised upwards. And we recognize that it’s not a great thing for the company to have to come out and revise guidance downwards. But I think it’s good for us to come out to the market and be honest for where we are with our production, and hopefully we can be there in the second-half of the year. So thanks a lot for, everyone, attending the call, and look forward to putting out news in the second-half of the year that will simulate the stock to move higher.

If you like this beach, then you can help your friends locate it by letting them know about Fred & EntendanceInvestors Beach.

Let's all make this place a thriving sheltered Club for excellence, education and information!

|

|

|

|

Post by Entendance on Aug 10, 2017 6:12:13 GMT -5

EXK August 10, 2017

Endeavour Silver Appoints New Vice President, Engineering to Lead New Technical Services and Mine Development Group

Vancouver, Canada – August 10, 2017 - Endeavour Silver Corp. (TSX: EDR, NYSE: EXK) announces the appointment of Andrew Sharp as its new Vice President, Engineering to lead the Company’s new Technical Services and Mine Development Group.

Mr. Sharp, B.Eng., FAusIMM., is a professional engineer with 30 years of experience in the mining industry, is fluent in Spanish and has worked many years in Mexico. He brings to Endeavour a wealth of experience in executive and mine management, mine planning and operations, mine startups and turnarounds, mine evaluations and feasibility studies, mine permitting and government relations.

Bradford Cooke, CEO and Director, commented, “I am thrilled to welcome Andrew to the Endeavour management team. His skills and experience are a nice fit with our senior group, and his depth and breadth of knowledge in the mining sector will enhance our ability to become bigger and better going forward as we optimize our three current mines and develop new mines to fuel our future growth.”

Mr. Sharp started his mining career in 1982 working part time as an underground labourer at various mines in Western Australia while studying to earn his Bachelor of Engineering degree. After graduation in 1987, Andrew worked for 10 years as a mining engineer for Newmont and others at gold mines in Australia and Malaysia. From 1997 to 2005, he ran his own consulting practice in Australia, was Chief Mining Engineer at a gold mine in Ghana, and became Manager of Mine Planning Services for Ok Tedi Mining in Papua New Guinea. Over the past 12 years, Andrew took on a number of more senior roles, including Manager of Planning, Mine Manager, General Manager, Vice President of Technical Services and Executive Vice President of Mining Operations for companies such as Pan American Silver, Silver Standard and others.

Andrew’s primary responsibilities at Endeavour will include leading the Company’s new Technical Services and Mine Development Group, ensuring engineering excellence throughout the organization, overseeing the design, permitting and construction of development projects to production, supporting mine operations and acquisitions, completing optimization studies, introducing technological advances, and helping improve operational performance.

Endeavour’s new Technical Services and Mine Development Group will include the existing construction and metallurgical managers, and will be joined by new managers of mining, geology and permitting, as well as project leaders for each of the two development projects, El Compas and Terronera.

About Endeavour Silver – Endeavour Silver is a mid-tier precious metals mining company that owns three high grade, underground, silver-gold mines in Mexico. Since start?up in 2004, Endeavour has grown its mining operations organically to produce 9.7 million ounces of silver and equivalents in 2016. We find, build and operate quality silver mines in a sustainable way to create real value for all stakeholders. Endeavour Silver’s shares trade on the TSX (EDR) and the NYSE (EXK).

|

|

|

|

Post by Entendance on Aug 30, 2017 6:05:39 GMT -5

Endeavour Silver announces that exploration drilling at the Guanacev mine in Durango State, Mexico has extended high grade silver-gold mineralization along strike within the Santa Cruz vein and discovered new ore grade mineralization within a shallow, parallel splay of the Santa Cruz vein known as the La Negra vein

6:56 AM ET 8/30/17 | Briefing.com

These holes extend the boundaries of the current resource area (dated December 31, 2016). Drilling highlights include 786 grams per tonne (gpt) silver and 0.71 gpt gold (836 gpt AgEq) over 3.4 m true width (24.4 opT AgEq over 11.2 feet (ft)), with an internal interval assaying 2,260 gpt silver and 1.73 gpt gold (2,381 gpt AgEq) over 0.3 m true width (69.4 opT AgEq over 1.0 ft)

EXK Endeavour Silver Drilling Extends High Grade Silver-Gold Mineralization in Santa Cruz Vein at the Guanaceví Mine in Durango, Mexico

Vancouver, Canada – August 30, 2017 – Endeavour Silver Corp. (NYSE: EXK, TSX: EDR) announces that exploration drilling at the Guanaceví mine in Durango State, Mexico has extended high grade silver-gold mineralization along strike within the Santa Cruz vein and discovered new ore grade mineralization within a shallow, parallel splay of the Santa Cruz vein known as the La Negra vein.

These holes extend the boundaries of the current resource area (dated December 31, 2016). Drilling highlights include 786 grams per tonne (gpt) silver and 0.71 gpt gold (836 gpt AgEq) over 3.4 m true width (24.4 opT AgEq over 11.2 feet (ft)), with an internal interval assaying 2,260 gpt silver and 1.73 gpt gold (2,381 gpt AgEq) over 0.3 m true width (69.4 opT AgEq over 1.0 ft) (view long sections here).

Results for nine new drill holes are summarized in the table below Click Here Silver equivalents are calculated at a ratio of 70:1 silver:gold.

Bradford Cooke, CEO of Endeavour Silver, commented, “These encouraging drill results continue to extend the resource envelope in the Santa Cruz vein at Guanaceví along strike from our current reserves and operating production areas. Another 15 drill holes have been completed and are in the lab for assaying. The 2017 drill program will wrap up this month below budget and ahead of schedule. We will then commence the process of the year-end resource and reserve estimation.”

Godfrey Walton, M.Sc., P.Geo., Endeavour’s President and COO, is the Qualified Person who reviewed and approved this news release and supervised the drilling programs in Mexico. A Quality Control sampling program of reference standards, blanks and duplicates has been instituted to monitor the integrity of all assay results. All samples are split at the local field office and shipped to ALS-Chemex Labs, where they are dried, crushed, split and 50 gram pulp samples are prepared for analysis. Gold and silver are determined by fire assay with an atomic absorption (AA) finish.

|

|

|

|

Post by Entendance on Sept 11, 2017 6:12:07 GMT -5

6:56 AM ET 9/11/17 | Briefing.com

EXK Endeavour Silver acquires the right to explore and mine for precious metals above the elevation of 2,000 metres above sea level on the 181-hectare Toro del Cobre concessions owned by Capstone Mining. In return, Endeavour has granted Capstone the right to explore and mine for base metals below the elevation of 2,000 masl on the Endeavour's Calicanto concessions.

For the purpose of this agreement, precious metal mineralization is defined as having greater than 60% net smelter revenue (NSR) value in gold and silver, and base metal mineralization is defined as having greater than 60% NSR value in copper, lead and zinc. Capstone has granted Endeavour a 1% NSR on all Capstone base metal production on Endeavour property, and Endeavour has granted Capstone a 1% NSR on all Endeavour precious metal production on Capstone property.

EXK Endeavour Silver and Capstone Mining Exchange Mineral Rights on Adjacent Properties in Zacatecas, Mexico

VANCOUVER, BC--(Marketwired - September 11, 2017) - Endeavour Silver Corp. (NYSE: EXK) (TSX: EDR) announces it has acquired the right to explore and mine for precious metals above the elevation of 2,000 metres above sea level (masl) on the 181-hectare Toro del Cobre concessions owned by Capstone Mining. Capstone's concessions are adjacent to the 75-hectare Calicanto concessions held by Endeavour in Zacatecas, Mexico. In return, Endeavour has granted Capstone the right to explore and mine for base metals below the elevation of 2,000 masl on the Endeavour's Calicanto concessions. Click here for a map.

The unique agreement is based on the observation that vein mineralization locally in the Zacatecas mining district is typically zoned vertically, with precious metal-rich vein mineralization historically found and mined above 2,000 masl, and base metal-rich vein mineralization historically found and mined below 2,000 masl. Both the Toro del Cobre and Endeavour concessions were historically mined for precious metals above 2,000 masl, but they lie adjacent to Capstone's Cozamin mine, which is currently mining base metals below 2,000 masl.

The Calicanto, Nevada and El Misie veins on Endeavour's Calicanto concessions all trend northwest onto the Toro del Cobre concessions. Endeavour is interested in tracing the precious metal mineralization from its own property onto Capstone's property. In the same way, Capstone is interested in exploring the deeper portions of these and other veins for base metals on Endeavour's property.

For the purpose of this agreement, precious metal mineralization is defined as having greater than 60% net smelter revenue (NSR) value in gold and silver, and base metal mineralization is defined as having greater than 60% NSR value in copper, lead and zinc. Capstone has granted Endeavour a 1% NSR on all Capstone base metal production on Endeavour property, and Endeavour has granted Capstone a 1% NSR on all Endeavour precious metal production on Capstone property.

Should Endeavour's exploration efforts on the Toro del Cobre concessions indicate a continuation of precious metals mineralization below 2,000 masl elevation, Endeavour will be entitled to conduct exploration and mining of >60% precious metal ores below 2,000 masl. In the same way, should Capstone's exploration on the Calicanto concessions indicate a continuation of base metals mineralization above 2,000 masl elevation, Capstone will be entitled to conduct exploration and mining of >60% base metal ores above 2,000 masl.

About Endeavour Silver -- Endeavour Silver is a mid-tier precious metals mining company that owns three high grade, underground, silver-gold mines in Mexico. Since start-up in 2004, Endeavour has grown its mining operations organically to produce 9.7 million ounces of silver and equivalents in 2016. We find, build and operate quality silver mines in a sustainable way to create real value for all stakeholders. Endeavour Silver's shares trade on the TSX (EDR) and the NYSE (EXK).

***Major Gold-Stock Breakouts

|

|

|

|

Post by Entendance on Oct 24, 2017 6:04:04 GMT -5

Endeavour Silver announces that exploration drilling on the Parral property in Chihuahua State, Mexico has verified high grade silver mineralization within the Argentina-Remedios area of the Veta Colorada

6:56 AM ET 10/24/17 | Briefing.com

Drilling highlights include 457 gpt silver over a 9.3 m true width (13.3 opT Ag over 30.5 feet (ft)) in hole CV26.5-1. Another high grade intercept assayed 4,641 gpt silver over a 2.3 m true width (135.3 opT Ag over 7.5 ft) in hole CV27-2.

EXK Endeavour Silver Drilling Verifies High Grade Silver Mineralization in the Veta Colorada on the Parral Project, Chihuahua, Mexico VANCOUVER, British Columbia, Oct. 24, 2017 (GLOBE NEWSWIRE) -- Endeavour Silver Corp. (NYSE:EXK) (TSX:EDR) announces that exploration drilling on the Parral property in Chihuahua State, Mexico has verified high grade silver mineralization within the Argentina-Remedios area of the Veta Colorada, which was drilled but never mined by a previous owner, IMMSA.

Industrial Minera Mexico, S.A. de C.V. (IMMSA) operated a high grade silver mine on the Veta Colorada until 1990 and on closing left behind a 32.1 million oz historical silver resource contained in 4.0 million tonnes (t) grading 248.5 grams per tonne (gpt). A qualified person has not done sufficient work to classify this historical estimate as a current mineral resource, Endeavour has not verified the historical resource and is not relying on it as a current mineral resource.

Twenty-one drill holes totaling 6,928 metres (m) of core were drilled to test the portion of the historic resource located within the Argentina-Remedios area of the Veta Colorada. (View long section here). The drill holes were spaced at approximately 100 m centres over an area 400 m long by 400 m deep.

Drilling highlights include 457 gpt silver over a 9.3 m true width (13.3 opT Ag over 30.5 feet (ft)) in hole CV26.5-1. Another high grade intercept assayed 4,641 gpt silver over a 2.3 m true width (135.3 opT Ag over 7.5 ft) in hole CV27-2.

Results for 12 high grade drill intercepts are summarized in the table HERE. Luis Castro, Vice President, Exploration for Endeavour Silver, commented, “These encouraging drill results help to verify the portion of the historic resource within the Argentina-Remedios area of the Veta Colorada. A new resource estimate will be prepared at year-end for release in the 1st quarter of 2018.

“Drilling is ongoing at other areas of the Parral property such as Palmilla and San Patricio, where there was a history of high grade mining but very little drilling and no previous resources, to test for new silver resources. We plan to release additional drill results during the 4th quarter of 2017.”

Godfrey Walton, M.Sc., P.Geo., Endeavour’s President and COO, is the Qualified Person who reviewed and approved this news release and supervised the drilling programs in Mexico. A Quality Control sampling program of reference standards, blanks and duplicates has been instituted to monitor the integrity of all assay results. All samples are split at the local field office and shipped to ALS-Chemex Labs, where they are dried, crushed, split and 50 gram pulp samples are prepared for analysis. Gold and silver are determined by fire assay with an atomic absorption (AA) finish.

About Endeavour Silver – Endeavour Silver is a mid-tier precious metals mining company that owns three high grade, underground, silver-gold mines in Mexico. Since start‑up in 2004, Endeavour has grown its mining operations organically to produce 9.7 million ounces of silver and equivalents in 2016. We find, build and operate quality silver mines in a sustainable way to create real value for all stakeholders. Endeavour Silver’s shares trade on the TSX (EDR) and the NYSE (EXK).

Contact Information - For more information, please contact:

Bradford Cooke, Chief Executive Officer

Toll free: (877) 685-9775

Main: (604) 685-9775

Fax: (604) 685-9744

Website: www.edrsilver.com

|

|

|

|

Post by Entendance on Nov 2, 2017 5:59:41 GMT -5

EXK Endeavour Silver Reports Financial Results for Third Quarter, 2017 VANCOUVER, British Columbia, Nov. 02, 2017 (GLOBE NEWSWIRE) -- Endeavour Silver Corp. (NYSE:EXK) (TSX:EDR) released today its financial results for the third quarter ended September 30, 2017. Endeavour owns and operates three underground silver-gold mines in Mexico: the Guanaceví mine in Durango state, and the Bolañitos and El Cubo mines in Guanajuato state.

The Company's financial performance in the Third Quarter, 2017 was down compared to the Third Quarter, 2016 due to lower production, higher operating costs and increased exploration and development expenditures. Production was slightly lower in Q3, 2017 compared to Q3, 2016 primarily due to operating issues at the Guanacevi mine, now partly resolved, and revised annual mine plans which led to lower throughput for the nine months ended September 30, 2017.

However, production was higher in Q3, 2017 compared to Q2, 2017 primarily due to improved performance at all three mines. As a result, the Company's financial performance in the Third Quarter, 2017 was up compared to the Second Quarter, 2017, with higher revenues, cash flow and earnings and lower cash and all-in sustaining costs.

Highlights of Third Quarter 2017 (Compared to Third Quarter 2016)

Financial

•Net earnings of $1.0 million(1) ($0.01 per share) compared to net earnings of $5.6 million ($0.04 per share)

•EBITDA(2) decreased 39% to $6.1 million

•Cash flow from operations before working capital changes decreased 31% to $5.7 million

•Mine operating cash flow before taxes(1) decreased 33% to $11.9 million

•Revenue decreased 5% to $39.8 million

•Realized silver price decreased 10% to $17.20 per ounce (oz) sold

•Realized gold price decreased 3% to $1,299 per oz sold

•Cash costs(2) increased 54% to $8.11 per oz silver payable (net of gold credits)

•All-in sustaining costs (AISC)(2) increased 53% to $17.53 per oz silver payable (net of gold credits)

•Working capital decreased 6% to $70.3 million from Q2, 2017

Operations

•Silver production decreased 2% to 1,262,064 oz

•Gold production decreased 5% to 13,648 oz

•Silver equivalent production was 2.2 million oz (at a 70:1 silver: gold ratio)

•Silver oz sold increased 6% to 1,275,922 oz

•Gold oz sold down 3% to 13,759 oz

•Bullion inventory at quarter-end included 196,092 oz silver and 466 oz gold

•Concentrate inventory at quarter-end included 37,043 oz silver and 633 oz gold

Exploration and Development

•Made production decision and commenced development of El Compas mine in Zacatecas

•Acquired additional prospective exploration properties near El Compas in Zacatecas

•Released high grade drill results for Santa Cruz orebody in Guanacevi

•Commenced development of mine ramp to access Milache orebody at Guanacevi by mid-2018

•Released high grade drill results for Terronera and La Luz mineralized zones at Terronera

•Received mine and plant permits for Terronera

•Appointed Vice President, Engineering to oversee technical services and development projects

1.The Consolidated Interim Financial Statements and Management’s Discussion & Analysis can be viewed on the Company’s website at www.edrsilver.com, on SEDAR at www.sedar.com and EDGAR at www.sec.gov. All amounts are reported in US$

2.Mine operating cash flow, EBITDA, cash costs and all-in sustaining costs are non-IFRS measures. Please refer to the definitions in the Company’s Management Discussion & Analysis

Endeavour CEO Bradford Cooke commented, “Our Third Quarter earnings, cash flow and revenues were down from Q3, 2016 but improved significantly compared to the Q2, 2017. Given that Guanacevi had to deal with new electrical and pump issues due to a lightning strike in July, now partly resolved, we anticipate continued improvement of our operating and financial performance in the Fourth Quarter 2017.

“Returning Guanaceví to long-term profitability relies in part on developing two new orebodies, Milache and Santa Cruz Sur. Underground ramp access is already underway towards Milache with initial production expected in the second half of 2018. Mine development at Santa Cruz Sur is scheduled to commence this quarter with initial production to coincide with production from Milache.

“Development of the El Compas mine and refurbishment of the La Plata plant are now well underway, with initial production scheduled to commence by the end of the First Quarter, 2018. We also received the mine and plant permits for Terronera and continue to conduct engineering trade-off studies while we await receipt of the dumps and tailings permits.

“We appointed Andrew Sharp as our new VP, Engineering to oversee our technical services and development projects. Over the past three months, he has built a core engineering team including managers of mining, metallurgy, construction, permitting and resource estimation to significantly expand our internal capabilities.

Third Quarter Financial Results

For the third quarter ended September 30, 2017, the Company generated revenue totaling $39.8 million (2016 - $42.1 million). During the quarter, the Company sold 1,275,922 silver oz and 13,759 gold oz at realized prices of $17.20 and $1,299 per oz respectively, compared to sales of 1,200,467 silver oz and 14,228 gold oz at realized prices of $19.16 and $1,340 per oz respectively in Q3, 2016.

After cost of sales of $32.5 million (2016 - $26.9 million), mine operating earnings amounted to $7.3 million (2016 –$15.2 million). Excluding depreciation and depletion of $4.4 million (2016 - $2.8 million), and share-based compensation of $0.1 million (2016- $0.2 million), mine operating cash flow before taxes was $11.9 million (2016 – $17.8 million) in Q3, 2017. Net earnings were $1.0 million (2016 –$5.6 million) after exploration expenses of $3.4 million (2016 – $2.4 million) and corporate general and administrative costs of $1.6 million (2016 – $2.8 million).

Direct production costs per tonne in Q3, 2017 increased 19% compared with Q3, 2016. Reduced production at Guancevi was the key driver behind the higher costs. Cash costs rose 54% on a consolidated basis due to the higher costs per tonne offset by slight improvement in grades and recoveries. All?in sustaining costs rose as a result of management significantly increasing capital investments for the long-term benefit of Guanaceví and El Cubo after a two?year period of reduced capital investment to maximize cash flow and ensure the viability of its operations during low silver and gold prices.

Working capital was $70.3 million, down 14% and 6%, respectively from December 31, 2016 and June 30, 2017. The working capital on-hand is determined to be sufficient for the Company to meet its short and medium term goals.

Conference Call

A conference call to discuss the results will be held today, Thursday, November 2nd at 10am PDT (1pm EDT). To participate in the conference call, please dial the following:

Toll-free in Canada and the US: 1-800-319-4610

Local Vancouver: 604-638-5340

Outside of Canada and the US: 1-604-638-5340

No pass-code is necessary to participate in the conference call.

A replay of the conference call will be available by dialing 1-800-319-6413 in Canada and the US (toll-free) or 1-604-638-9010 outside of Canada and the US. The required pass-code is 1722 followed by the # sign. The audio replay and a written transcript will also be made available on the Company’s website at www.edrsilver.com

|

|

|

|

Post by Entendance on Nov 7, 2017 13:27:15 GMT -5

banksters Cartel International

"...Financial services industry employees are trained to talk customers out of buying gold. They do this by pointing out its price volatility and riskiness. (The public has no idea that the gold price is manipulated, and fake.) If the customer still wants to buy it, then the broker steers them into electronic gold, such as bullion bank-controlled ETFs and major mining company equities.

This sterilizes the investor’s funds, and prevents them from being used to buy physical precious metals, which would interfere with the price rigging crime by increasing physical demand for and the price of gold, given its consistently tight supplies. It would also lessen capital flows onto the Gold Looting Field, the exact opposite of the Deep State manipulators’ agenda...

...The larger purpose behind the Deep State’s electronic gold products, beyond current profits, is to concentrate investment gold in a select number of locations that will be easy to control and raid when the time comes...

...For investors, electronic gold is nothing but modern day Fools’ gold. For the Deep State, it is a free ride, on investors’ backs, to the most massive physical gold theft of all times.

Taken together, we believe these factors present a compelling argument why investors should exit all of the electronic gold products specified at the beginning of this article, and convert the proceeds into physical gold and/or non-Deep State-controlled equities of companies in which they have full confidence that managements are working for them, not the bullion banks. The fact is that the Deep State manipulation of the gold price is never going to end until people stop buying electronic gold and providing the liquidity the Deep State needs to continue perpetrating the gold price rigging crime..." ***Electronic Gold: The Deep State’s Corrupt Threat to Human Prosperity and Freedom

|

|

|

|

Post by Entendance on Apr 9, 2018 5:50:14 GMT -5

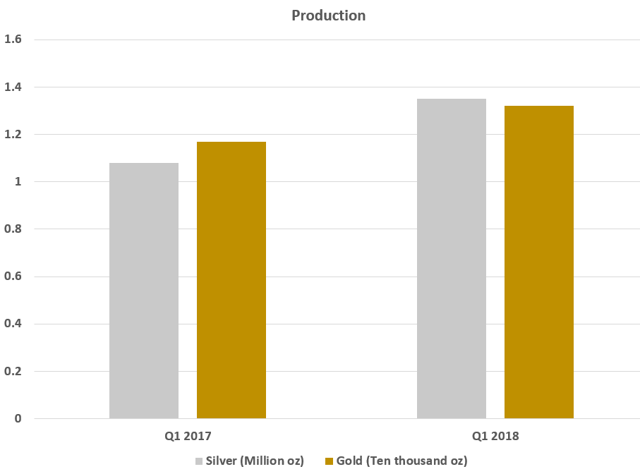

Endeavour Silver reports Q1 production results 6:10 AM ET 4/9/18 | Briefing.com Silver production in the First Quarter, 2018 increased 25% to 1,350,840 ounces (oz) compared to 1,076,974 oz silver in Q1, 2017 and gold production rose 13% to 13,208 oz compared to 11,724 oz gold in Q1, 2017, resulting in silver equivalent production of 2.3 million oz using a 75:1 silver-gold ratio.Silver production was higher in Q1, 2018 compared to Q1, 2017 due to higher mine output and ore grades at El Cubo and Bolaitos, partly offset by lower mine output at Guanacevi as the mine continues to recover from some operating issues last year. Gold production in Q1, 2018 compared to Q1, 2017 was higher at El Cubo and Guanacevi and lower at Bolaitos due to variations in gold grades at each mine.The El Compas mine development project remains on schedule for mine and plant commissioning to commence in April and commercial production to be achieved by the end of July.

At the Entendance Beach we continue to like Endeavour Silver in 2018

April 09, 2018 ***Endeavour Silver Produces 1,350,840 oz Silver and 13,208 oz Gold (2.3 Million oz Silver Equivalents) in the First Quarter, 2018; Provides Update of the El Compas Mine Development Project VANCOUVER, British Columbia, April 09, 2018 (GLOBE NEWSWIRE) -- Endeavour Silver Corp. (TSX:EDR) (NYSE:EXK) reports its production results for the First Quarter, 2018 from the Company’s three silver-gold mines in Mexico: the Guanaceví mine in Durango state and the Bolañitos and El Cubo mines in Guanajuato state.

Silver production in the First Quarter, 2018 increased 25% to 1,350,840 ounces (oz) compared to 1,076,974 oz silver in Q1, 2017 and gold production rose 13% to 13,208 oz compared to 11,724 oz gold in Q1, 2017, resulting in silver equivalent production of 2.3 million oz using a 75:1 silver-gold ratio.

Silver production was higher in Q1, 2018 compared to Q1, 2017 due to higher mine output and ore grades at El Cubo and Bolañitos, partly offset by lower mine output at Guanacevi as the mine continues to recover from some operating issues last year. Gold production in Q1, 2018 compared to Q1, 2017 was higher at El Cubo and Guanacevi and lower at Bolañitos due to variations in gold grades at each mine.

Production Highlights for First Quarter, 2018 (Compared to First Quarter, 2017)

•Silver production increased 25% to 1,350,840 oz

•Gold production increased 13% to 13,208 oz

•Silver equivalent production was 2.3 million oz (at a 75:1 silver:gold ratio)

•Silver oz sold increased 14% to 1,406,143 oz

•Gold oz sold increased 12% to 12,674 oz

•Bullion inventory at quarter-end included 85,675 oz silver and 302 oz gold

•Concentrate inventory at quarter-end included 74,359 oz silver and 1,195 oz gold

Bradford Cooke, Endeavour CEO, commented, “Our First Quarter production was much improved over last year. As a result, we are on track to deliver higher production and lower costs in 2018 thanks to improved operating performance at each of the three existing mines and the development of our fourth mine at El Compas into commercial production by the end of July.

“Our quarterly production profile should continue to improve this year as Guanacevi benefits from the productivity optimization program now underway and Bolañitos and El Cubo continue mining higher silver grades as per their 2018 mine plans. Metal recoveries were a bit lower than planned in Q1, 2018 but are expected to improve during the year.”

Operations Summary for First Quarter, 2018

At Guanacevi, mine output was lower due to mine development falling behind schedule in 2017 and the reallocation of mine personnel to implement a productivity optimization program. Silver and gold grades were both higher due to better dilution control, so that silver equivalent production in Q1, 2018 was only slightly lower than Q1, 2017. Mine output, development and productivity should improve in Q2, 2018.

At Bolañitos, mine output and silver grades were higher but gold grades were lower due to variations within the LL-Asunción vein. Silver equivalent production in Q1, 2018 was significantly higher than Q1, 2017. Grades are expected to return to plan during the year.

At El Cubo, mine output, silver grades and gold grades were all higher in Q1, 2018 compared to Q1, 2017, which resulted in a sharp increase in production in Q1, 2018.

El Compas Mine Development Project Update

The El Compas mine development project remains on schedule for mine and plant commissioning to commence in April and commercial production to be achieved by the end of July.

El Compas finally received its explosives permit in March, which allowed the mine to accelerate the development of the main access ramp. The main ramp was at 355 metres as of March 31. The San Juan vein was intersected and 28 metres were developed along the vein. Mining should commence on the main El Compas vein later this month.

The last plant component, a mobile crushing circuit, arrived on site in March and is currently being installed. The rest of the plant, tailings dam and surface infrastructure construction projects are essentially complete. A small stockpile of low grade ore has been started. To view the March 31, 2018 photographic update for the El Compas Project, click HERE or visit our website under the Mining Assets section.

Production Tables for First Quarter, 2018

Release of First Quarter, 2018 Financial Results and Conference Call

The 2018 First Quarter Financial Results will be released before market on Thursday, May 3, 2018 and a telephone conference call will be held the same day at 9:00am PT (12:00pm ET). To participate in the conference call, please dial the numbers below. No pass-code is necessary.

Toll-free in Canada and the US: 1-800-319-4610

Local Vancouver: 604-638-5340

Outside of Canada and the US: +604-638-5340

A replay of the conference call will be available by dialing 1-800-319-6413 in Canada and the US (toll-free) or +604-638-9010 outside of Canada and the US. The required pass-code is 2164#. The audio replay and a written transcript will be available on the Company's website at www.edrsilver.com under the Investor Relations, Events section.