|

|

Post by Entendance on Aug 9, 2022 6:28:03 GMT -5

VANCOUVER, British Columbia, Aug. 09, 2022 (GLOBE NEWSWIRE) -- Endeavour Silver Corp. (“Endeavour” or the “Company”) (NYSE: EXK; TSX: EDR) is pleased to announce its financial and operating results for the three and six months ended June 30, 2022. As a result of the Company’s strong operating performance, Management has raised its 2022 production guidance. All dollar amounts are in US dollars (US$).

“We have continued to outperform our mine plans, by delivering an exceptional Q2 with production 15% above plan, stated Dan Dickson, CEO of Endeavour Silver. “This has prompted management to raise our production outlook for 2022 to 7.6 – 8.0 million silver equivalent ounces. The additional production has allowed us to maintain our cost guidance on per ounce metrics, but industry-wide inflation continues to be a challenge. We are seeing the largest inflationary impacts on energy costs, plant reagents and steel prices which are affecting both operating and development costs. Cost control will continue to be a key focus as cost pressures are expected to continue for the remainder of the year.”

Added Mr. Dickson, “During the 2nd quarter, again we made the decision to withhold from sale a meaningful amount of silver, due to the drop in silver price. We are holding over 1.6 million silver equivalent ounces in finished goods inventory for future sale. Short term, the increased inventory has negatively impacted our quarterly financial metrics such as revenue, earnings, cash flow and our cash balance. Longer term, we anticipate selling the inventory at higher metal prices.”

Q2 2022 Highlights Higher Production: 1,359,207 ounces (oz) of silver and 9,289 oz of gold for 2.1 million oz silver equivalent (AgEq)(1) reinforces delivery of improved consolidated production for the year.

Lower Revenue Due to Withholding Metal Sales: Revenue of $30.8 million from the sale of 602,894 oz of silver and 9,792 oz of gold at average realized prices of $22.72 per oz silver and $1,840 per oz gold.

Negative Earnings and Lower Cash Flow Due to Lower Revenue and Non-Cash Items: Net loss of $11.9 million, or $0.07 per share. Adjusted net loss of $4.3 million(2) after adjusting for a $7.6 million change in the fair value of investments. $3.6 million in operating cash flow before working capital changes(2) and Mine operating cash flow before taxes(2) of $8.8 million.

Operating Costs per Ounce In-Line with Guidance, Despite Industry-Wide Inflation: Cash costs(2) of $10.08 per oz payable silver and all-in sustaining costs(2) of $19.56 per oz payable silver, net of gold credits.

Healthy Balance Sheet: Cash position of $116.2 million and working capital(2) of $149.7 million.

Guanacevi Continued to Outperform: Production exceeded plan driven by higher grades.

Bolañitos Remained Steady: Strong silver production from higher silver grades and increased throughput were offset by lower gold production and lower gold grades.

Withheld Significant Metal Inventories: Metal inventory at quarter end totaled 1,399,356 oz silver and 2,580 oz gold of bullion inventory and 12,408 oz silver and 587 oz gold in concentrate inventory. The market value of finished goods at June 30, 2022 was $34.5 million.

Advancing the Terronera Project: Work continued on the early works program initiated last year including engineering, critical contracts, procurement of long-lead items and extensive due diligence on the project financing. The Company intends to make a formal construction decision subject to completion of a financing package and receipt of additional amended permits in the coming months. $18 million has been spent as of June 30th 2022, with an additional budget of $23 million expected to be spent through to the end of October to continue the advancement of the project.

Subsequent to Quarter End

Closed the Acquisition of the Pitarrilla Project: The addition of the Pitarrilla project enhances the company’s growth profile while maintaining a silver focus.

Revision to Full Year 2022 Guidance

The following table summarizes the updated 2022 Production Guidance for Endeavour Silver: here

Consolidated Silver Equivalent(1) Production has increased to 7.6 – 8.0 million oz from 6.7 – 7.6 million oz. The increase to consolidated production is primarily driven by higher than planned ore-grades along the El Curso orebody at Guanacevi. Production at Bolanitos has been slightly revised upwards to meet the upper end of its previous guidance.

Operating Costs Guidance is expected to remain unchanged with cash costs expected to average $9.00 - $10.00 per oz and AISC are expected to average $19.00 - $20.00 per oz. Management notes that the Company is tracking to meet the upper end of the guidance range, given persisting global inflationary pressures. Increases in prices of raw materials such as reagents, explosives, steel, diesel and power are driving continued cost escalation across the industry. The company has identified efficiencies to mitigate pressure on costs and cost metrics in the second half of the year, including enhanced monitoring and tracking at the mines, improved blasting in development, the gradual increase of tonnes milled and reduced waste handling at Guanacevi.

For the three months ended June 30, 2022, net revenue, decreased by 35% to $30.8 million (Q2 2021: $47.7 million).

Gross sales of $31.7 million in Q2 2022 represented a 34% decrease over the $48.3 million in Q2 2021. Silver oz sold decreased by 46%, due to the buildup of the larger finished goods inventory held at June 30, 2022. There was a 15% decrease in the realized silver price, resulting in a 54% decrease in proceeds from silver sales. Gold oz sold were flat with a 1% decrease in the realized gold price, resulting in a 1% decrease in proceeds from gold sales. During the period, the Company sold 602,894 oz silver and 9,792 oz gold for realized prices of $22.72 and $1,840 per oz, respectively, compared to Q2 2021 sales of 1,120,266 oz silver and 9,810 oz gold for realized prices of $26.82 and $1,866 per oz, respectively. In Q2 2022, London spot prices for silver and gold averaged $22.60 and $1,877, respectively.

The Company significantly increased its finished goods silver inventory and slightly decreased its finished goods gold inventory to 1,411,764 oz and 3,167 oz, respectively, at June 30, 2022 compared to 668,382 oz silver and 3,841 oz gold at March 31, 2022. The cost allocated to these finished goods was $20.8 million at June 30, 2022 compared to $13.5 million at March 31, 2022. At June 30, 2022, the finished goods inventory fair market value was $34.5 million, compared to $24.1 million at March 31, 2022. Earnings and other financial metrics, including mine operating cash flow(2), operating cash flow(2) and EBITDA(2) were impacted by the withholding of sales during Q2 2022.

After cost of sales of $26.3 million (Q2 2021 - $37.5 million), a decrease of 30%, mine operating earnings were $4.5 million (Q2 2021 - $10.2 million). The decrease in cost of sales was impacted by the decrease in the quantity of silver ounces sold during the period offset by increased labour, power and consumables costs with lower royalty costs. Royalties decreased 49% to $2.2 million primarily due to the decrease in silver ounces sold during the period.

The Company had an operating loss of $1.3 million (Q2 2021: operating earnings of $0.8 million) after exploration and evaluation costs of $3.8 million (Q2 2021: $5.0 million), general and administrative costs of $1.3 million (Q2 2021: $4.3 million) a write off of exploration properties of $0.5 million (Q2, 2021 - $Nil), and care and maintenance cost of $0.2 million (Q2 2021: $0.1 million).

The loss before income taxes was $8.8 million (Q2 2021: earnings before taxes of $8.9 million) after finance costs of $0.3 million (Q2 2021: $0.2 million), a foreign exchange loss of $0.3 million (Q2 2021: gain of $0.7 million), and investment and other expense of $6.9 million (Q2 2021: investment and other income of $1.8 million). The investment and other expenses during Q2 2022 primarily resulted from an unrealized loss on marketable securities and warrants of $7.6 million (Q2 2021: $1.5 million).

The Company realized a net loss for the period of $11.9 million (Q2 2021: net earnings of $6.7 million) after an income tax expense of $3.1 million (Q2 2021: $2.2 million). Current income tax expense increased to $1.3 million (Q2 2021 - $1.1 million) due to increased profitability impacting the income tax and special mining duty, while deferred income tax expense of $1.8 million is primarily due to the estimated use of loss carryforwards to reduce taxable income generated at both Guanacevi and Bolanitos (Q2 2021 – $1.1 million).

Direct operating costs(2) on a per tonne basis increased to $132.63, up 11% compared with Q2 2021 due to higher operating costs at Guanaceví and Bolañitos. Guanaceví and Bolañitos have seen increased labour, power and consumables costs and at Guanaceví, increased third party ore purchased and operating development have increased compared to the prior year.

Consolidated cash costs per oz(2), net of by-product credits, decreased to $10.08 driven by increased silver grades, reduced royalty costs and increased by-product gold sales, offset by increased direct operating costs per tonne(2) AISC(2) decreased by 23% on a per oz basis compared to Q2 2021 as a result of a 27% increase in ounces produced driven by a 51% increase in silver grade, decreased allocated general and administrative costs and a decrease in mine site exploration offset by increased sustaining capital expenditures.

The complete financial statements and management’s discussion & analysis can be viewed on the Company’s website, on SEDAR at www.sedar.com and on EDGAR at www.sec.gov. All shareholders can receive a hard copy of the Company’s complete audited financial statements free of charge upon request. To receive this material in hard copy, please contact Investor Relations at 604-640-4804, toll free at 1-877-685-9775 or by email at gmeleger@edrsilver.com.

Conference Call

A conference call to discuss the Company’s Q2 2022 financial results will be held today at 10:00 a.m. PT / 1:00 p.m. ET. To participate in the conference call, please dial the numbers below.

Date & Time: Tuesday, August 9, 2022 at 10:00 a.m. PT / 1:00 p.m. ET

Telephone: Toll-free in Canada and the US +1-800-319-4610

Local or International +1-604-638-5340

Please allow up to 10 minutes to be connected to the conference call.

Replay: A replay of the conference call will be available by dialing (toll-free) +1-800-319-6413 in Canada and the US (toll-free) or +1-604-638-9010 outside of Canada and the US. The replay passcode is 9151#. The replay will also be available on the Company’s website at www.edrsilver.com.

About Endeavour Silver – Endeavour Silver Corp. is a mid-tier precious metals mining company that operates two high-grade underground silver-gold mines in Mexico. Endeavour is currently advancing the Terronera project towards a development decision, pending financing and final permits and exploring its portfolio of exploration and development projects in Mexico, Chile and the United States to facilitate its goal to become a premier senior silver producer. Our philosophy of corporate social integrity creates value for all stakeholders.

|

|

|

|

Post by Entendance on Aug 10, 2022 2:48:06 GMT -5

Endeavour Silver Corp. (NYSE:EXK) Q2 2022 Earnings Conference Call August 9, 2022

Company Participants

Galina Meleger - Vice President, Investor Relations

Dan Dickson - Chief Executive Officer

Conference Call Participants

Marcus Giannini - H.C. Wainwright

Jake Sekelsky - Alliance Global Partners

Joseph Reagor - ROTH Capital Partners

Justin Stevens - PI Financial

Galina Meleger

Good morning, everyone and welcome to today's call. Before we get started, I would ask that you view our MD&A, the cautionary language regarding forward-looking statements and the risk factors pertaining to these statements. Our MD&A and financial statements are available on our website under our disclosure portal.

You will have seen that there was a retransmission to today's news release that went through about 30 minutes ago. The amendment was with regards to a correct estimate for our 2022 all-in sustaining cost forecast of $20 to $21 per ounce net of the gold credit. This is the only change made to the news release.

With us on today’s call we have Dan Dickson, Endeavour Silver’s CEO and Christine West, our CFO. On behalf of Endeavour Silver, I'd like to thank you again for joining our call today.

And I'll now turn it over to our CEO, Dan for his formal remarks.

Dan Dickson

Thank you, Galina, and welcome everyone to this conference call for the second quarter of 2022. Before we discuss our Q2 results, I'd like to touch on current market conditions. While our operational performance has been strong, our stock price has been impacted by sell-off across equities in both the broader markets and in the precious metals. The gold miner equities have disconnected from the actual metal prices and have underperformed their underlying commodities.

Year-to-date, the S&P is down 20%, gold and silver equities are down 30% and similarly our stock is trading down about 30%, despite our robust operational performance. We remain confident that the current environment is bullish for gold and silver, especially as we are nearing peak rate expectations in this hiking cycle and inflation remains persistent. Recently, we've seen positive movements in our space. We expect this trend to accelerate in the second half of this year with the potential for precious metals to make a strong rebound.

So with that view on pricing, we have once again made a strategic decision to withhold the sale of a meaningful amount of metal. At the end of June, we were carrying approximately 1.6 million silver equivalent ounces in finished goods inventory with a market value of almost $35 million. Given that almost one full quarter's worth of metal remains in finished goods, our financial metrics were negatively impacted. Revenue decreased by 35%, earnings declined by 275%, and operating cash flow before working capital fell by 60%.

With the benefit of having more than $115 million in cash on the balance sheet and no material debt, we have both the liquidity and flexibility to support the short-term sales strategy. However, we do expect to put cash back on the balance sheet by selling our finished goods inventory when silver prices strengthened.

Our two operating mines, Guanacevi and Bolañitos have generated excellent results during Q2. Silver production increased by nearly 30%, driven by strong performance at Guanacevi, while gold production decreased by 17%, primarily due to the closure of the El Compas mine last August. Guanacevi has been outperforming due to the mining of higher-grade ore within the El Curso ore body, an increased purchase ore from local third-party miners.

While it's been very rewarding to see grades reach these levels, we expect the grades to be lower going forward, but still higher than planned. Additionally, in Q2, throughput was lower than planned as we invested in a new cone crusher at Guanacevi. This will allow us to increase throughput in the second half of the year.

For the quarter, our cost per ounce metrics have been tracking relatively in line with cash costs averaging a little over $10 per ounce and all-in sustaining costs averaging a little over $19.50 per ounce net of the gold credit. Our direct operating cost per tonne have increased by 10% due to inflationary pressures across a number of inputs.

The additional production from the exceptional grades at Guanacevi have allowed us to maintain our cost guidance on a per ounce metrics, but industry-wide inflation continues to be relevant. Like other miners, we were impacted by similar inflationary trends. Increases in prices of raw materials, such as reagents, explosives, steel, diesel and power are all driving continued cost escalation across the industry.

As you saw in today's news release, we increased our annual production outlook to better reflect the -- reflect better than the anticipated operating performance mainly at Guanacevi. We are now targeting to produce 7.6 to 8.0 million silver equivalent ounces for this year. Overall and after factoring positive operating results in the first half of 2022, we increased our production outlook at Guanacevi by 12% in response to the higher than planned ore grades along the El Curso ore body. And we tightened up the forecast of Bolañitos to meet the upper end of its previous guidance.

While we maintained our original cost outlook, costs are likely to be at the upper end of their respective ranges with cash costs expected to average closer to $10 per ounce and all-in sustaining costs expected to average closer to $21. We acknowledge that global inflationary pressures are expected to persist for the rest of the year. As such, we have identified efficiencies to mitigate pressures on costs and cost metrics.

With our operations running well, we are getting closer to reaching a financing deal and a subsequent development decision at Terronera. To continue with the advancement of the project, the Board has approved an additional $23 million in development expenditures until the end of October. This investment is on top of the $18 million already spent up to June 30, 2022. This brings the 2022 development budget to $41 million, signaling a vote of confidence by the Board and allow us to move ahead with the early works, while we've worked tirelessly to complete the financing impact.

At the same time, we are moving forward with engineering construction of access roads, site clearing and purchasing of long lead items. With respect to equipment, I'm pleased to say that we've locked in prices on much of our long lead items to mitigate these inflationary pressures.

Since Terronera will be our largest and lowest-cost mine, it's a significant priority for our management team. We're working very hard to complete a financing package and look forward to providing with an update in the coming months.

Along with Terronera, we're building an impressive pipeline of new projects to fuel our future growth. Subsequent to quarter end, we completed the acquisition of the Pitarrilla project from SSR Mining, which is the world's largest undeveloped silver deposit. Not only does this important acquisition allow us to maintain a high leverage to silver on our pathway to growth, but it strengthens and complements our regional expertise. For the remainder of the year, our exploration team will focus initially on verifying the historic resources and then turned their attention to many exploration targets on this highly promising property.

Let me wrap this up. This is truly an exciting time for Endeavour Silver for the potential we see in the capital markets and for our operational performance. We've made operational and strategic improvements in all areas of our business, and built a remarkable pipeline of growth focused on benefiting from longer-term strength in silver prices with Terronera, Pitarrilla and Parral.

Marcus Giannini, H.C. Wainright

Congrats on the good quarter with raising guidance. So, you guys speak about cost control in the release. Obviously, it's not easy to do in the current environment with a key focus of the firm right now and pretty much for everyone else in the industry as well. Out of curiosity, can you break down where you think you can bring out some efficiencies out of the business and maybe even quantify the savings category?

Dan Dickson

Yeah. It will be difficult Marcus to quantify some of the savings by category. Some of the things that we're looking at is mainly on our development side, with the amount of meshing and bolting we're doing. So we're seeing a high increase in our bolting and meshing costs, which is really the inflationary we're seeing in steel. We're kind of relooking at how we can better deploy that going forward.

Obviously, the biggest thing for us is that, Guanaceví and it's really an economies of scale. You can see that our mining rate actually hasn't hit what our plan has been for the year. And ultimately, our processing tonnes also haven't hit as planned. For the year, we're slightly below on a tonnes per day, or on the lower end of our original guidance for tonnes per day through the plant. And that's a function of a couple of things that we did in the first half of the year.

One changing out a cone crusher, other stuff has been maintenance on leach tanks. And a lot of that work has been done and the cone crusher is installed and I think that's going to allow us to get closer to 1,200 tonnes per day. As we get up to the 1,200 tonnes per day for Guanaceví, we're going to see our cost per tonne come down, and ultimately that will make its way through. And that's some of the efficiencies that we've been looking at for the second half of the year is ensuring that we're hitting our throughput tonnes to get the economies of scale in some of those inflationary things.

Things like, diesel and power costs there is very little we can do. We're obviously accepting those costs as is it's just finding efficiencies and productivity throughout the operations. And I think, there's still a lot of opportunity at Guanaceví to be able to do that. Secondly, as prices have come down, our royalty costs at Guanaceví are going to come down as well. A big portion of our costs is the royalties that come from El Curso.

Again, when silver was over $25 we paid a 16% royalty on it between $20 to $25 we paid 13%. And below $20 we paid 9%. So ultimately, we are getting some cost savings in the royalties with these lower prices that will help push down some of our costs going forward as well. But of course, we would prefer to have higher prices and paying higher royalties.

Marcus Giannini

Okay. Perfect. Yeah. That was really helpful. And then lastly, congrats on Pitarrilla, would you be willing to venture a guess as to how much you've spent on the site since closing and an approximate estimate as to what you expect to see for the remainder of the year on a monthly basis? And then I guess, pushing a little bit further here. Any idea how to use combined funds breakdown into labor and claims fees, et cetera?

Dan Dickson

Yeah. I mean, you're not pushing too much. Claim fees and labor most of our costs that we're carrying there's 28 individuals that work – that we've acquired when we acquired the Pitarrilla project. On a monthly basis, our burn rate there is about $100,000 to $200,000 just with keeping the plant -- or sorry the camp, and those individuals employed and going through that. Since we've acquired it, which closed shortly after Q2 here, we haven't incurred all that much. I mean we're kind of mobilizing our exploration team to start a project.

And at the beginning of the year, we've had a $1.8 million exploration budget for Pitarrilla. We think we are going to come close to that $1.8 million, in the six months, depending on how we can get mobilized. As far as the breakdown between labor and actual costs I would say, probably about $1.8 million. Labor costs can be somewhere between $500,000 to $700,000. Some of that would be on new exploration geologists contractors in there.

But I don't know, if I need to give much more breakdown in those terms for Pitarrilla. We do have good plans. Like I said, we have to prove out the historic resource. That will take some time. And then ultimately, we have a couple of plans with regards to exploration. Once there's an exploration ramp it's about 1.1 kilometers in, it needs to work around. It's come through a fault that's collapsed. We'll have to work on that. And then there's targets from surface, that we're going to consider. And ultimately we'll get some of that work done here in the next four to five months, and then come up with a new plan for 2023 for Pitarrilla.

Marcus Giannini

All right.

Dan Dickson

The carrying costs and sorry the last question, which is claims. The carrying costs on, claims is very small I'd say less than $200,000 for the year. That would have been all paid normally, that's paid in January and July.

Marcus Giannini

Got it. Okay. Perfect. Thanks a lot. that’s it from me

Dan Dickson

Thanks for the questions, Marcus.

Jake Sekelsky, Alliance Global Partners

Hi, Dan and team. Thanks for taking my questions. Obviously, you had a strong first half on the back of higher grades. And you mentioned they'll moderate a bit Dan, in the second half, but still remains a little bit elevated. Are you able to quantify thi,s but I'm just trying to get a handle on what type of profile we might see in the second half?

Dan Dickson

Yes. I think we're just always concerned that, some of the grades that we're seeing come through Guanaceví have been higher than what our reserve grades are. We are continually seeing the grades in this area being higher. And you can even point to some of the drill results that we put out earlier this year, on an extension of El Curso, which had a significantly higher grades even that we've mined.

And ultimately, we do think there'll be a reversion to what the reserves actually are and we want to be kind of protective to that. But still again, we expect that we're going to be higher than planned. I don't know -- I can't put a specific number on it, at this point. I think we averaged close to 450 grams per tonne of silver equivalents, in the last quarter and I think that would come down almost kind of 8% to 10%. So we're closer to the 400 grams silver equivalent per tonne.

Jake Sekelsky

Okay. That's, helpful. And then just looking at the disconnect, that you mentioned between precious metals equities and where prices are right now. Realizing that development is accelerating at Terronera, you just closed on Pitarrilla, do you think you'll continue to take an opportunistic stance from an M&A standpoint, or do you sort of feel that your plate is kind of full right now?

Dan Dickson

No. Yes, our plate is definitely full right now. But at the same time, we haven't put down the pens with regards to potential that's out there to build the company. Ultimately, I think being opportunistic is a good approach to take especially on M&A. And we do have a long-term view that silver prices are going to be higher than where they are now.

And ultimately. we think that will persist for a long time. It's hard to find silver assets -- predominantly silver assets in the space. And I don't think it's prudent to kind of put pens down and not look at things. So, we continue to look at things. Of course as we grow, cash flow is going to become more meaningful and trying to find cash flow in operations would probably take a priority over development project just on you'd be able to use of funds. But at the same time we don't stop looking at those things because if there's value to be had, we want to be able to take advantage of that.

Jake Sekelsky

Got it. Okay, that’s all for me. Thanks again.

Joseph Reagor, ROTH Capital Partners

Hey Dan and team. Thanks for taking my questions. I think -- most of the stuff I want to touch on was already touched on by the prior two people. But maybe a little bit more detail on cost inflation. How do you guys think about the impact of these cost inflation you're seeing when it comes to the Terronera project? Do you feel that the estimates you have out there publicly you're comfortable with? Do you expect that you'll have to change them? Do you take a proactive approach of doing a larger financing package? Like what are the puts and takes there?

Dan Dickson

Yes. Thanks Joe. I think that's a very fair question. It's something that we are very mindful of. I think the good news from our standpoint with Terronera is we've locked in a lot of lead items. So, our mobile equipment fleet with Sandvik I think 22 of 33 pieces of equipment have arrived and are on site. We've procured a number of plant equipment items that have locked in those prices.

So, really it's going to come down to the inflation on the infrastructure. And we've looked at it. And it's not that we're uncomfortable with the $175 million that's in that feasibility study. But things have obviously changed over the past year with regards to inflation and I think that's going to come its way through.

I think when we come out with a development decision for Terronera we're going to be able to come up with a new estimate from a capital standpoint taking into consideration what we've already purchased, which would be locked in and then inflationary costs that would be built into the project.

Again I think we'll come out with that when we come out with a development decision. But there's definitely been inflation across the space and we're quite mindful of that. I want to make sure that when we go to build Terronera we have a budget that's actually reflective of what's happened out there and what we can purchase for and be able to guide the market appropriately.

Joseph Reagor

Okay. Maybe a little bit further detail there. What percentage of the $175 million did you guys already lock in?

Dan Dickson

We've locked in almost. So, we've got a $41 million development budget, which includes equipment that we've already purchased. As far as the $175 million of what percentage is already locked in I don't have that in front of me, but I'm guessing it's more towards the 25%, 30% range.

Joseph Reagor

Okay. Okay, fair enough. My figures enough in there. And then looking at Guanacevi, I think Jake tried to get up this too. Even with the guidance raise, it feels as though there's still some room to the upside there. If grades were even for silver at least 50 grams lower than they were even in Q1, you would easily get to the midpoint of guidance -- of the revised guidance there. And that's even at the low end of your tonnage guidance.

So is it that you guys have some concerns with -- that the tonnage may end up being a little lighter than originally expected? I know you said you've been behind schedule, but is there some thought that you might not be able to catch up, or is the grade really going to fall that much? Like, how do I account for that?

Dan Dickson

Yes. No, I think, it's a fair question. And we don't expect our tonnage in the second half of the year to be lighter. In fact, we expect it to be better than the first half of the year, just because of the work that we've done in the plant and our expectations.

One of the things that makes it difficult for us to guide is, how much a third-party ore comes to the plant. With the higher prices, more ore comes to the plant and we actually saw some of the highest grade ore delivered to the plant by third-party miners in the first half of the year. So that's one aspect of it that we have to be cautious of when we guide what grades are ultimately going forward.

That can vary, like I say, just because of prices or we don't specifically have transparency into the minds of some of the third local miners of what grades they're going to have. And ultimately, they don't probably really know either. So it's -- we're taking a guesstimate there. And ultimately, as we move into down the El Curso ore body, we do have estimates done through reserves and we have to use that as a guide. Now, we have been seeing higher grades than those reserves, but we can't just go and change our reserve grades with the idea that it's going to improve, other than us putting out further data on it.

And I think, we're being relatively cautious with our expectations of where grades are going to be in the second half of the year. But, yes, there's quite a possibility that we beat that middle of guidance for sure if grades continue to be elevated compared to what we had in our operating plan.

Joseph Reagor

Okay. And then, on the third-party ore, just real quick. How many tonnes of third-party ore did you process in the first half?

Dan Dickson

In the first half, we did about 13% of our tonnes were in third-party ore. I think almost 15% in Q2 and 11% in Q1.

Justin Stevens, PI Financial

Hey, guys. Yes. Congrats on a really solid start to the year here. I think I was going to start just by following on from Joe's question there. When you guys pay for third-party ore is that a percentage of metal content, or do you pay sort of a flat rate per tonne?

Dan Dickson

No, we pay at a percentage of metal content. So when it's delivered, we actually make a payment and it's about 60% to 66% just depending on what's in that ore of payment per tonne on metal content. So with the higher metal content coming in with higher prices, we pay more on a third-party ore basis and that shows up in our overall cost per tonne.

Justin Stevens

Got it. Yeah. That makes sense. I think the other, sort of, question I had was in terms of the El Curso, obviously, you guys are paying higher royalty rates for all the ore comes off that lease. Do you have a rough idea in terms of either tonnage or metal content in terms of the Guanaceví feed what is coming from the leased properties versus sort of the existing wholly-owned?

Dan Dickson

Yes. So we're required under our agreement with Frisco that over -- minimum 600 tonnes per day comes from El Curso. So ultimately almost half. I think we've been closer to 60% to 65% of our throughput related to the El Curso material rollout of first six months of the year.

Justin Stevens

Perfect. That's great. And, I guess, the only other question I had was, I know obviously you put out a couple of lines on Bruner Gold looking to twin some holes and sort of validate historical resource there. Any updates just on the time line or sort of how that's going?

Dan Dickson

Yes. We've got geologists on the ground. We actually don't have drills on the ground yet that was planned in the fourth quarter -- end of third quarter into the fourth quarter. With where prices are we could look to slow that down. But at this point in time, it's on schedule for like I say end of third quarter early fourth quarter.

Justin Stevens

That's for the drilling. And then by the time I guess you get results QA/QC and then actually look at the modeling it'd probably be into the next year then right?

Dan Dickson

Into next year or the end of Q4.

Justin Stevens

Got it. Great. All right. That’s it from me. Thank you so much.

Dan Dickson

Thanks, Justin. Good questions.

I want to thank everybody for attending today's call. I know it's the doldrums this summer. I think we put together a really good first half of the year with our operational performance and I expect second half of the year to be hopefully as good as the first half of the year.

Of course, the main things that we're working on in this company is trying push an era forward and ultimately put a finance active together so we can announce development for us to continue to grow in the silver space, and keep pushing to what our goal is to become a senior silver producer. Thanks again for everybody attending and talking.

|

|

|

|

Post by Entendance on Aug 17, 2022 10:41:54 GMT -5

|

|

|

|

Post by Entendance on Aug 18, 2022 4:30:37 GMT -5

August 17, 2022

2022 is off to a strong start. We have continued to outperform our mine plans, with production 15% above plan. This has prompted management to raise our production outlook for 2022 to 7.6 – 8.0 million silver equivalent ounces. The additional production has allowed us to maintain our cost guidance on per ounce metrics, but industry-wide inflation continues to be a challenge. We are seeing the largest inflationary impacts on energy costs, plant reagents and steel prices which are affecting both operating and development costs. Cost control will continue to be a key focus as cost pressures are expected to continue for the remainder of the year.

With our operations running well, we are getting closer to reaching a financing deal and a subsequent development decision at Terronera. To continue with the advancement of the project, the board has approved an additional $23 million in development expenditures until the end of October. This investment is on top of the $18 million already spent up to June 30, 2022. This brings the 2022 development budget to $41 million, signalling a vote of confidence by the board and allowing us to move ahead with early works while we work tirelessly to complete a finance package.

|

|

|

|

Post by Entendance on Aug 19, 2022 3:38:07 GMT -5

Endeavour Silver Corp. (“Endeavour” or the “Company”) (NYSE: EXK; TSX: EDR) regrets to announce that the Company’s founder, Director and Executive Chairman, Bradford Cooke passed away suddenly and unexpectedly in Vancouver, BC at the age of 67. Endeavour wishes to extend our sincere condolences to his family, friends, business associates and his extensive network amongst the investment community.

Brad Cooke is well known as an accomplished geologist with nearly five decades of experience in the metals and mining industry. Brad has been a vibrant member of the mining community and will be dearly missed. As a professional geologist and entrepreneur, he has created shareholder value for stakeholders around the world through discovery, development and operations in his long-standing successful career. He has earned a reputation as an eternal optimist trying to shape the world for the greater good with constructive hard work.

Throughout all his success in business, he never forgot the difficulties of the less fortunate. He collaborated on numerous humanitarian projects over many years to make a positive difference. He instilled corporate social responsibility at Endeavour from the start in the communities near our mines. He also served as President of the Silver Institute, as an industry voice in creating public awareness of the silver industry.

Brad Cooke formed Endeavour together with Godfrey Walton in 2003 for the purpose of acquiring and developing high grade silver-gold projects in Mexico. Since that time, the Company has acquired, rebuilt and expanded four silver mines and made a significant discovery with potential to become Endeavour’s next cornerstone mine.

Dan Dickson, CEO of Endeavour stated, “We are incredibly saddened by this sudden loss. Brad was extremely loyal to his people. He will be sincerely missed and always remembered by a large group of family and friends around the world. I have known and worked with Brad for 15 years and I consider him my dear friend. I will always remember him for his passion, commitment and hard-working attitude. With his vibrant energy, he strove to bring out the best in those who worked with him.” |

|

|

|

Post by Entendance on Aug 24, 2022 7:09:03 GMT -5

Endeavour Silver Honours Bradford Cooke with Company Tribute and Details on Celebration of Life Endeavour Silver Honours Bradford Cooke with Company Tribute and Details on Celebration of LifeVANCOUVER, British Columbia, Aug. 24, 2022 -- Endeavour Silver Corp. (“Endeavour” or the “Company”) (NYSE: EXK; TSX: EDR) has been showered with loving condolences and widespread sympathies from the mining and investment community for the recent passing of the company’s founder, Director and Executive Chairman, Bradford Cooke. Today we are honouring his memory with a special company presentation and details about his memorial.

Company Tribute PDFIn response to the high volume of positive messages, we are publishing a special company tribute for Brad, who was an inspiration to many over his long-standing successful career. The following company presentation, “A Tribute: In Loving Memory of Bradford Cooke”, contains a photo gallery and quotes from the leadership team and closest friends at Endeavour.

Celebration of Life Event and Online Memorial PageOn behalf of the Cooke Family, a celebration of life will be held in Vancouver, BC on Sunday August 28, 2022. An online Memorial Page has also been set up and anyone who knew Brad is encouraged to share personal stories and memories about the ways in which he impacted them.

Statement from the Cooke Family: “We have all been deeply touched by the outpouring of love and support on the occasion of Brad’s recent passing. Brad had deep respect and love for his wider business family and community and was loved and cherished by so many. It is a great comfort to know that Brad passed in a state of deep peace. Thank you for the many thoughtful messages of condolence. It would be a great gift to receive your stories, photos, reflections and memories of Brad on the Memorial page we created for him. Our deepest thanks - Brad’s family: Susana, Devon, Shaun, Matt, Sasha, & Maria”

Date: Sunday August 28, 2022

Time: Arrival 12:30pm, 1pm start

Venue: Celebration Hall & Courtyard at the Mountainview Cemetery, Vancouver

Venue Details: Note: the hall is located within the cemetery, use this Google Maps link for exact location: goo.gl/maps/WJHdqCLxnzR7xNmF8

Live Streaming Link: bradcookememorial.ca/memorial-livestream/

Replay available upon request

Address for Mailing Sympathy Cards & Gifts:

Mail to Endeavour Silver Head Office:

Attn: The Cooke Family

PO Box 10328

Suite 1130-609 Granville Street

Vancouver, BC

Canada V7Y 1G5 |

|

|

|

Post by Entendance on Aug 29, 2022 8:37:12 GMT -5

VANCOUVER, British Columbia, Aug. 29, 2022 -- Endeavour Silver Corp. (“Endeavour” or the “Company”) (NYSE: EXK; TSX: EDR) announces that its Board of Directors (the “Board”) has appointed the Company’s Lead Director, Rex McLennan, as Chairman of the Board. Mr. McLennan steps into the Chairman position to replace former Executive Chairman, Bradford Cooke, who passed away suddenly and unexpectedly last week (see news releases dated August 18 and August 24 , 2022).

Rex McLennan joined the Company as an Independent Director in June 2007, appointed as Chair of the Audit Committee. As an Independent Corporate Director, he has chaired the audit committees of a number of publicly traded companies, and was appointed Lead Director for Endeavour in May 2021; chairing the Corporate Governance and Nominating committee, as well as serving on the Audit and Safety & Sustainability committees. He is a past Director of Pinnacle Renewable Energy Inc, Boart Longyear Ltd, and the World Gold Council, London UK.

His professional and executive career spans over 40 years including C-level executive positions serving as Chief Financial Officer for Viterra, prior to its acquisition by Glencore PLC in 2012, and Placer Dome, a global mining company acquired by Barrick Gold in 2006; with an earlier career with Imperial Oil, a major subsidiary of Exxon.

Mr. McLennan holds a Master of Business Administration from McGill University in Finance/Accounting and a Bachelor of Science in Mathematics/Economics from the University of British Columbia. He also holds the ICD.D designation from the Institute of Corporate Directors.

“Rex has been a Director of Endeavour Silver for 15 years and we have benefitted tremendously from his guidance during this time,” said Dan Dickson, CEO of Endeavour Silver. “He has been instrumental in the evolution of the Company and exemplifies our vision in sustaining growth for all of our stakeholders.”

|

|

|

|

Post by Entendance on Sept 8, 2022 7:41:38 GMT -5

Parral Project, MexicoEndeavour Silver acquired the Parral Project from SSR Mining in 2016 as a past producing silver mine of IMMSA that closed in 1990. Endeavour silver controls 4 district mineralized veins systems totaling 3,450 hectares. Endeavour is focused on drilling high priority targets and increasing the resource on this large, prospective property to be able to model production in the future.

District

Parral is a top 10, large, multi-vein, silver-rich historic mining district in Mexico measuring 10 km long by 10 km wide, discovered in the 1500’s, the Palmilla mine provided silver to Mexican mint in 1800s

Property

3,450 hectares

Infrastructure

Adjacent to city of Parral, with paved and gravel road access, on power grid, readily available water, labour and services in Parral

Widths

Four main high grade veins extend over eight km and up to 40 m thick, and bulk tonnage stockworks range from 10 to 50 meters thick

Grades

High grade veins range from 100 to 1000 gpt silver and bulk tonnage stockworks range from 30 to 150 gpt silver

Recoveries

Historically 60-90%

Potential

Multiple targets to discover new high grade zones for underground mining, and new low-grade zones for open pit mining

VANCOUVER, British Columbia, Sept. 08, 2022 --

Endeavour Silver Corp. (TSX: EDR, NYSE: EXK) is pleased to report positive drill results from its ongoing drill program at its Parral project in the State of Chihuahua, Mexico. The high-grade silver results show the potential for resource expansion at depth and along strike in the El Verde and Sierra Plata Deep areas along the Veta Colorada structure. Since April of this year, the Company has drilled over 5,300 meters in 23 holes, totaling 8,100 meters year to date, with the aim to define and extend mineralized zones.

Considerable exploration potential remains along the 35 square kilometre land package and exploration will be on-going, with additional testing for new discoveries with surface mapping and sampling underway. This program will aid the Company’s goal to define a mineral resource large enough to support a preliminary economic assessment.

Highlights from Recent Drill Results

199 gpt Ag, 4.68% Pb and 2.64% Zn for 428 gpt AgEq over a 3.48 m ETW , including 501 gpt Ag, 8.08% Pb and 6.50% Zn for 971 gpt AgEq over 0.27 m (VCU-78)

322 gpt Ag, 5.19% Pb and 1.62% Zn for 528 gpt AgEq over a 1.67 m ETW , including 605 gpt Ag, 14.8% Pb and 3.46% Zn for 1,150 gpt AgEq over 0.53 m (VCU-80)

664 gpt Ag, 1.88% Pb and 0.80% Zn for 747 gpt AgEq over a 5.56 m ETW , including 5,600 gpt Ag, 15.35% Pb and 1.75% Zn for 6,096 gpt AgEq over 0.22 m (VCU-90)

242 gpt Ag, 0.48% Pb and 1.66% Zn for 317 gpt AgEq over a 5.34 m ETW , including 711 gpt Ag, 0.53% Pb and 2.13% Zn for 806 gpt AgEq over 0.52 m (VCU-96)

Abbreviations include: gpt: grams per tonne; Ag: silver; Pb: lead; Zn: zinc; ETW: estimated true width; m: metre; HW: hanging wall. Silver equivalents are calculated using a silver price of $22 per troy ounce, lead price of $0.90 per pound and zinc price of $1.20 per pound.

“In the areas of the El Verde and Sierra Plata historically mined areas, we continue to verify extensions of the mineralized zones at depth and along strike,” stated Dan Dickson, Chief Executive Officer. “The focus for the rest of the year will be to test the northern part of the project with a surface drilling program on various north to south striking structures, such as the northern extension of Veta Colorada, San Alberto and the El Cabezón systems; as well as resuming drilling of the San Patricio vein.”

Latest Drill Results

|

|

|

|

Post by Entendance on Sept 12, 2022 6:55:04 GMT -5

VANCOUVER, British Columbia, Sept. 12, 2022

Endeavour Silver Corp. (“Endeavour” or the “Company”) (NYSE: EXK; TSX: EDR) is pleased to announce it has entered into an agreement to sell a 100% interest in Minera Oro Silver de Mexico, S.A. de C.V. (“MOS”), a wholly owned subsidiary of Endeavour to Grupo ROSGO, S.A. de C.V., (“Grupo ROSGO”). MOS holds the El Compas property and the lease on the La Plata processing plant in Zacatecas, Mexico. All references to dollars ($) in this news release are to United States dollars.

Pursuant to the agreement, Grupo ROSGO will pay Endeavour $5 million cash over five years with an initial payment of $250,000 on signing of the definitive agreement. Instalment payments of $500,000 will be made every six months other than the third payment, which will be $750,000. The payments are secured by a pledge of the shares of MOS.

Endeavour CEO, Dan Dickson commented, “We are pleased with the sale of El Compas to Grupo ROSGO as it streamlines our project portfolio and frees up management time to focus on advancing our extensive growth pipeline, including the Terronera project and Pitarrilla.”

|

|

|

|

Post by Entendance on Sept 26, 2022 11:44:32 GMT -5

Endeavour Silver Continues to Intersect High-Grade Mineralization at the Guanacevi Mine including 3.54 g/t Gold and 1,129 g/t Silver for 1,412 g/t Silver Equivalents over 7.28 meters

VANCOUVER, British Columbia, Sept. 26, 2022 -- Endeavour Silver Corp. (TSX: EDR, NYSE: EXK) (“Endeavour” or the “Company”) is pleased to report positive drill results from its ongoing drill program at the Guanacevi Mine in Durango state, Mexico. Drilling continues along the prolific Santa Cruz vein in two areas (view Santa Cruz Vein longitudinal section ), with the objective to convert, expand, and discover new resources.

The 2022 drill program has continued to focus on the El Curso property, establishing lateral and vertical extents of the mineralized zone between the Porvenir Cuatro and Milache mines. The exploration and exploitation rights to the El Curso property were obtained in 2019 from Ocampo Mining S.A. de CV., and have become an integral contributor to the operation. Recently, under the same agreement terms, the Company has tested the northwest extension of the Porvenir Dos orebody with encouraging results from initial drilling.

Highlights from Recent El Curso Drill Results

3.50 gpt Au and 1,150 gpt Ag for 1,430 gpt AgEq over a 1.16 m ETW , including 12.80 gpt Au and 4,240 gpt Ag for 5,264 gpt AgEq over 0.24 m (UCM-102)

3.54 gpt Au and 1,129 gpt Ag for 1,412 gpt AgEq over a 7.28 m ETW , including 25.40 gpt Au and 7,080 gpt Ag for 9,112 gpt AgEq over 0.43 m (UCM-106)

Highlights from Recent Porvenir Dos Drill Results

1.43 gpt Au and 967 gpt Ag for 1,081 gpt AgEq over a 2.43 m ETW , including 3.64 gpt Au and 5,120 gpt Ag for 5,411 gpt AgEq over 0.23 m (APD-03)

1.60 gpt Au and 1,460 gpt Ag for 1,589 gpt AgEq over a 1.17 m ETW , including 2.91 gpt Au and 3,340 gpt Ag for 3,573 gpt AgEq over 0.25 m (APD-04)

Abbreviations include: gpt: grams per tonne; Au: gold; Ag: silver; ETW: estimated true width; m: metre; HW: hanging wall. Silver equivalents are calculated at a ratio of 80:1 silver:gold.

“We are encouraged by the drill results at Guanacevi, as we continue to delineate high grades in areas which are proximal to the mill and historic working areas. The results announced today demonstrate both growth and steady improvement of the deposit and mine plan,” stated Dan Dickson, Chief Executive Officer. “Our focus remains on delineating mineralized extensions to mining horizons and resource growth.”

|

|

|

|

Post by Entendance on Oct 11, 2022 6:23:32 GMT -5

Endeavour Silver: output trending towards upper end of full-year guidance

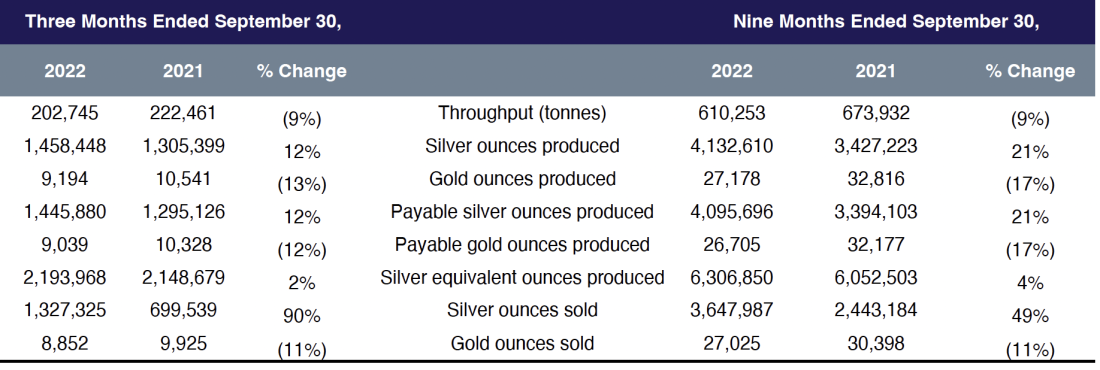

Endeavour Silver Corp. (“Endeavour” or the “Company”) (NYSE: EXK; TSX: EDR) (“Endeavour” or the “Company”) is pleased to report third quarter 2022 production of 1,458,448 silver ounces (oz) and 9,194 gold oz, for silver equivalent (“AgEq”) production of 2.2 million oz, totalling 6.3 million AgEq oz for the 9 months ended September 30, 2022. Annual production is trending towards the upper end of the guidance range for the year, forecasted at 7.6 to 8.0 million AgEq oz.

“The ore grades processed at Guanacevi continue to exceed plan, which has positioned the Company to meet the upper end of our improved production guidance. The outperformance is well timed, as we continue to face financial pressure from lower metal prices and inflationary effects on inputs” stated Dan Dickson, Chief Executive Officer. “We announced impressive drill results from our exploration program in the quarter at Guanacevi, where we are extending and defining the vertical extents of the Porvenir Dos orebody, which is near historic working areas.”

Q3 2022 Highlights

Steady Focus on Safety Improvement: Lost time injury frequency and severity rates continue to trend down as employees keep focus on our proactive safety orientated culture through the “Te Cuido” safety philosophy.

Guanacevi Continued to Outperform: Silver and gold production on plan, driven by higher grades.

Bolañitos Performance Remained Steady: Strong silver production, higher silver grades and increased throughput were offset by the impact of lower than expected gold production and gold grades.

Metal Sales and Inventories: Sold 1,327,325 oz silver and 8,852 oz gold during the quarter. Held 1,527,548 oz silver and 3,210 oz gold of bullion inventory and 2,769 oz silver and 144 oz gold in concentrate inventory at quarter end.

Guanacevi Delivers Positive Drill Results: Further exploration results from near mine drilling in easily accessible areas are intersecting high-grade silver-gold mineralization on the El Curso property (see News Release dated September 26, 2022).

Positive Exploration Results at Parral: Drilling is intersecting some of the highest grades to date, with significant widths along the Veta Colorada structure (see News Release dated September 8, 2022).

Advancing the Terronera Project: The early works program initiated last year continued, including detail engineering, critical contracts and the procurement of long lead items. Extensive due diligence work continued for project financing. The Company intends to make a formal construction decision subject to completion of a financing package and receipt of additional amended permits in the coming months.

Completed the Acquisition of the Pitarrilla Project: The world’s largest undeveloped silver project that will form the cornerstone of the Company’s growth profile, together with Terronera and Parral.

Divested the El Compas Property to Grupo ROSGO: Completed the sale of the property and the plant for US$5 million over five years (see News Release dated September 12, 2022).

Q3 2022 Mine Operations

Consolidated silver production increased 12% to 1,458,448 ounces in Q3 2022 compared to Q3 2021, primarily driven by increased silver production at the Guanacevi mine. The high grades at the El Curso orebody have led to improved production, allowing for production targets to be met during a period of decreased plant throughput. Local third-party ores continued to supplement mine production, amounting to 12% of quarterly processed tonnes and contributing to higher ore grades. Guanacevi throughput was 4% higher than the prior quarter but lower than plan, due to heavy rainfall in a short, concentrated period during September. Management continues to review alternatives to further increase throughput above the current 1,200 tpd capacity with changes in grinding size and leach time.

Gold production decreased by 13% to 9,194 ounces primarily due lower gold grades mined at the Bolañitos mine. The increased gold production from Guanacevi offset the gold produced from the El Compas mine, which suspended operations in Q3, 2021.

Bolañitos Q3 2022 throughput was 3% lower Q3 2021 with silver grades 5% higher and gold grades 5% lower. Silver production increased by 2% while gold production decreased by 11% at the Bolañitos mine. The change in grades were due to typical variations in the ore body.

Production Highlights for the Three and Nine Months Ended September 30, 2022 Mine-by-mine production in the third quarter and the nine months ended September 30 was:

Production Tables for the Nine Months Ended September 30, 2022 by Mine (1)

Q3 2022 Financial Results and Conference Call

The Company’s Q3 2022 financial results will be released before markets open on Tuesday, November 8, 2022 and a telephone conference call will be held the same day at 10:00 a.m. PT / 1:00 p.m. ET. To participate in the conference call, please dial the numbers below.

Date & Time: Tuesday, November 8, 2022 at 10:00 a.m. PT / 1:00 p.m. ET

Telephone: Toll-free in Canada and the US +1-800-319-4610

Local or International +1-604-638-5340

Please allow up to 10 minutes to be connected to the conference call. Replay: A replay of the conference call will be available by dialing (toll-free)

+1-800-319-6413 in Canada and the US (toll-free) or +1-604-638-9010 outside

of Canada and the US. The replay passcode is 9479#. The replay will also

be available on the Company’s website at www.edrsilver.com

|

|

|

|

Post by Entendance on Oct 18, 2022 3:49:06 GMT -5

|

|

|

|

Post by Entendance on Nov 8, 2022 7:08:31 GMT -5

Endeavour Silver Announces Q3 Financial Results; Earnings Conference Call at 10am PST (1pm EST) Today VANCOUVER, British Columbia, Nov. 08, 2022 (GLOBE NEWSWIRE) -- Endeavour Silver Corp. (“Endeavour” or the “Company”) (NYSE: EXK; TSX: EDR) is pleased to announce its unaudited financial and operating results for the three and nine months ended September 30, 2022. All amounts reported are in United States (US) dollars.

Dan Dickson, CEO, commented, “This quarter is a continuation of our strong operational performance. With production guidance reaffirmed, and a strong fourth quarter expected, we are feeling confident about our 2022 production results. Like the rest of the industry, profit margins are under pressure. The strength of the USD is weighing on commodity prices, and inflation is increasing direct costs. We are fortunate that the elevated grade profile at Guanacevi and strong operational performance has allowed us to stay within or near our guided cost ranges on a per ounce basis.”

“We continue to focus on business improvement and cost management initiatives, while being mindful of the future. Continuing to advance the Terronera project in a deliberate and disciplined manner towards a construction decision and the completion of the Pitarrilla acquisition, are both significant developments towards the future of the Company.”

Q3 2022 Highlights

Continued Strong Production: 1,458,448 ounces (oz) of silver and 9,194 oz of gold for 2.2 million oz silver equivalent (AgEq) (1) at an 80:1 silver:gold ratio, totaling 6.3 million AgEq oz for the 9 months ended September 30, 2022. Strong year to date production reinforces delivery of 2022 guidance.

Revenue Impacted by Withholding Metal Sales & Lower Realized Prices: Generated $40.4 million from the sale of 1,327,325 oz silver and 8,852 oz gold at average realized prices of $19.24 per oz silver and $1,678 per oz gold. Management continued to carry higher metal inventory totaling 1,527,549 oz silver and 3,210 oz gold of bullion inventory and 2,770 oz silver and 143 oz gold in concentrate inventory, with a market value of approximately $35 million at September 30, 2022.

Operating Costs per Ounce In-Line with Guidance, Despite Industry-Wide Inflation: Cash costs(2) of $10.32 per oz payable silver and all-in sustaining costs (AISC)(2) of $20.27 per oz payable silver, net of gold credits.

Negative Earnings and Lower Cash Flow Due to Impacted Revenue: Net loss of $1.5 million or $0.01 loss per share. $7.3 million in cash flow from operations before working capital changes(2) and mine operating cash flow before taxes(2) of $12.3 million. The Company continued to hold significant finished goods held at costs on the balance sheet at quarter end.

Healthy Balance Sheet: Cash position of $69.2 million and $101.6 million in working capital(2). Cash decreased in the quarter, as funds were spent to complete the acquisition of the Pitarrilla Project with a $35 million cash payment and early works expenditures to advance the Terronera project.

Strong Liquidity Remains: While the cash balance decreased during the quarter, the realized sale of finished goods inventory, with a market value of approximately $35 million at quarter end, would imply a cash balance closer to $100 million.

Advancing the Terronera Project: Work continued on predevelopment activities initiated last year including detailed engineering, critical contracts, procurement of long-lead items and road and camp construction. The Company intends to make a formal construction decision subject to completion of a financing package and receipt of additional amended permits in the coming months. Budgeted development expenditures for 2022 are estimated to be $41.0 million.

Completed the Acquisition of the Pitarrilla Project: The world’s largest undeveloped silver project that will form the cornerstone of the Company’s growth profile, together with Terronera and Parral (see News Release dated July 6, 2022).

Divested the El Compas Property to Grupo ROSGO: Completed the sale of the property and the plant for US$5 million over five years (see News Release dated September 12, 2022).

For the three months ended September 30, 2022, net revenue, increased by 15% to $39.7 million (Q3 2021: $34.6 million).

Gross sales of $40.4 million in Q3 2022 represented a 15% increase over the $35.0 million in Q3 2021. Silver oz sold increased by 90%, due to both a 12% increase in silver production and a significantly smaller buildup of finished goods inventory during Q3, 2022 compared to Q3, 2021. There was a 22% decrease in the realized silver price resulting in a 48% increase to silver sales. Gold oz sold decreased 11% with a 6% decrease in realized gold prices resulting in a 16% decrease in gold sales. The decrease in gold sales is primarily driven by the decreased gold grades at the Bolañitos mine and the suspension of production from the El Compas mine. During the period, the Company sold 1,327,325 oz silver and 8,852 oz gold, for realized prices of $19.24 and $1,678 per oz, respectively, compared to sales of 699,539 oz silver and 9,925 oz gold, for realized prices of $24.56 and $1,791 per oz, respectively, in the same period of 2021. For the three months ended September 30, 2022, the realized prices of silver and gold were within 3% of the London spot prices. Silver and gold London spot prices averaged $19.23 and $1,729, respectively, during the three months ended September 30, 2022

The Company increased its finished goods silver and finished goods gold inventory to 1,530,319 oz silver and 3,353 oz gold, at September 30, 2022 compared to 1,411,764 oz silver and 3,167 oz gold at June 30, 2022. The cost allocated to these finished goods was $22.1 million at September 30, 2022, compared to $20.8 million at June 30, 2022 and $18.3 million at September 30, 2021. At September 30, 2022, the finished goods inventory fair market value was $34.7 million, compared to $34.5 million at June 30, 2022. Earnings and other financial metrics, including mine operating cash flow(2), operating cash flow(2) and EBITDA(2) were impacted by the withholding of sales during Q3 2022.

Cost of sales for Q3, 2022 was $34.5 million, an increase of 31% over the cost of sales of $26.3 million for Q3, 2021. The cost of sales in Q3, 2022 was impacted by increased input costs and slightly impacted by the delay in recognition of costs associated with the increase in the quantity of silver ounces in finished goods at the end of the period. Overall costs for Q3, 2022 were impacted by higher labour, power and consumables costs as the Company is experiencing significant inflationary pressures. During Q3, 2022, the Company also recorded an allowance on the valuation of warehouse inventory of $1.3 million (Q3, 2021 – Nil).

In Q3, 2022, the Company had an operating loss of $1.3 million (Q3, 2021 – operating earnings of $3.0 million) after exploration and evaluations costs of $4.0 million (Q3, 2021 – $4.7 million), general and administrative expense of $2.2 million (Q3, 2021 – expense recovery $0.5 million), and care and maintenance expense of $0.2 million (Q3, 2021 – $0.4 million). In the three months ended September 30, 2021 operating earnings included $0.7 million in severance costs related to the suspension of the operations at the El Compas mine.

The earnings before taxes for Q3, 2022 was $1.7 million (Q3, 2021 – loss $0.8 million) after finance costs of $0.3 million (Q3, 2021 – $0.2 million), a foreign exchange gain of $0.8 million (Q3, 2021 –foreign exchange loss of $1.2 million), gain on assets disposal of $2.8 million (Q3, 2021 -$Nil) and investment and other expense of $0.3 million (Q3, 2021 –$2.4 million).

The Company realized a net loss for the period of $1.5 million (Q3, 2021 –$4.5 million) after an income tax expense of $3.2 million (Q3, 2021 – $3.7 million). In Q3, 2022 earnings were impacted by a $1.1 million mark-to-market adjustment resulting in an unrealized loss on investments included in investment and other expense (Q3, 2021 - $3.0 million).

Current income tax expense increased to $1.2 million (Q3 2021 - $0.7 million) due to increased profitability impacting the income tax and special mining duty, while deferred income tax expense of $2.0 million is primarily due to the estimated use of loss carryforwards to reduce taxable income generated at both Guanaceví and Bolañitos (Q3 2021 – $3.0 million).

Direct operating costs(2) on a per tonne basis increased to $131.61, up 14% compared with Q3 2021 due to higher operating costs at Guanaceví and Bolañitos and a reduction in ore tonnes processed. Guanaceví and Bolañitos have seen increased labour, power and consumables costs and at Guanaceví, increased third party ore purchased and operating development have increased compared to the prior year.

Consolidated cash costs per oz(2), net of by-product credits increased 27% to $10.32 driven by increased direct costs per tonne(2) and a reduction in by-product gold sales, offset by increased ore grades. AISC(2) increased by 16% on a per oz basis compared to Q3, 2021 as a result of the increased cash costs(2) and increased allocated general and administrative costs offset by a slight reduction in sustaining capital expenditures

The complete financial statements and management’s discussion & analysis can be viewed on the Company’s website, on SEDAR at www.sedar.com and on EDGAR at www.sec.gov. All shareholders can receive a hard copy of the Company’s complete audited financial statements free of charge upon request. To receive this material in hard copy, please contact Investor Relations at 604-640-4804, toll free at 1-877-685-9775 or by email at gmeleger@edrsilver.com.

Conference Call

A conference call to discuss the Company’s Q3 2022 financial results will be held today at 10:00 a.m. PST / 1:00 p.m. EST. To participate in the conference call, please dial the numbers below.

Date & Time: Tuesday, November 8, 2022 at 10:00 a.m. PST / 1:00 p.m. EST

Telephone: Toll-free in Canada and the US +1-800-319-4610

Local or International +1-604-638-5340

Please allow up to 10 minutes to be connected to the conference call.

Replay: A replay of the conference call will be available by dialing (toll-free) +1-800-319-6413 in Canada and the US (toll-free) or +1-604-638-9010 outside of Canada and the US. The replay passcode is 9479#. The replay will also be available on the Company’s website at www.edrsilver.com

|

|

|

|

Post by Entendance on Nov 23, 2022 8:03:46 GMT -5

|

|

|

|

Post by Entendance on Dec 9, 2022 3:29:08 GMT -5

VANCOUVER, British Columbia, Dec. 08, 2022 -- Endeavour Silver Corp. (“Endeavour” or the “Company”) (TSX: EDR, NYSE: EXK) announces that it has filed on SEDAR ( www.sedar.com ) a technical report (as defined in National Instrument 43-101) for the Company’s recently acquired Pitarrilla project in Durango state, Mexico. The Technical Report dated November 21, 2022 and entitled “Mineral Resource Estimate for the Pitarrilla Ag-Pb-Zn Project, Durango State, Mexico” (the “2022 Pitarrilla Report”) provides an independent estimate of the Mineral Resources identified at Pitarrilla as of October 6, 2022. The 2022 Pitarrilla Report was prepared on behalf of the Company by SGS Geological Services Inc.(“SGS”), an international firm specializing in mining and mineral estimation, engineering and evaluation services.

Dan Dickson, Chief Executive Officer, stated “With a verified current resource of nearly 600 million ounces of silver, the 2022 Pitarrilla Report validates the merits of acquiring one of the world’s largest undeveloped silver deposits. Through historic drilling, the Pitarrilla project has benefitted from over 225,000 metres of drilling and was advanced to a prefeasibility study of an underground operation and an open pit feasibility study in 2009 and 2012, respectively. The comprehensive work done to date, combined with the size and the scale of the deposit, provide flexibility and versatility for various mining scenarios. We will use the data collected to guide our exploration path going forward, with the potential to add significant value to the Company.”

The following information is derived from the 2022 Pitarrilla Report: The following information is derived from the 2022 Pitarrilla Report:

The total Indicated Mineral Resources (open pit and underground) at Pitarrilla totals 158.6 million tonnes containing 491.6 million ounces (oz) silver (Ag) grading 96.4 grams per tonne (gpt), 1.1 million pounds (lbs) of lead (Pb) grading 0.31%, 2.6 million pounds of Zinc (Zn) grading 0.74% for a total of 693.9 million ounces of silver equivalent (AgEq) grading 136 gpt.

The Inferred Mineral Resource (open pit and underground) totals 35.4 million tonnes containing 99.4 million oz Ag grading of 87.2 gpt, 281 million lbs Pb grading 0.36%, 661 million lbs Zn grading 0.85% for a total of 151.2 million ounces AgEq grading 132.7 gpt.

Silver equivalent grades are calculated using this formula: Ag (gpt) + [Pb (%) X 2204.6 X Pb Price / Ag Price X 31.1] + [Zn (%) X 2204.6 X Zn Price / Ag Price X 31.1] with price assumptions of Pb $1.00, Zn $1.30 and Ag $22.00.

Pitarrilla Mineral Resources Summary (effective as of October 6, 2022)

Notes:

(1) The classification of the current Mineral Resource Estimate into Indicated and Inferred Mineral Resources is consistent with current 2014 CIM Definition Standards - For Mineral Resources and Mineral Reserves.

(2) All figures are rounded to reflect the relative accuracy of the estimate and numbers may not add due to rounding.

(3) All Mineral Resources are presented undiluted and in situ, constrained by continuous 3D wireframe models, and are considered to have reasonable prospects for eventual economic extraction.

(4) Mineral Resources which are not mineral reserves do not have demonstrated economic viability. An Inferred Mineral Resource has a lower level of confidence than that applying to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of Inferred Mineral Resources could be upgraded to Indicated Mineral Resources with continued exploration.

(5) It is envisioned that parts of the Pitarrilla deposit (oxide and transition mineralization) may be mined using open pit mining methods. In-pit mineral resources are reported at a cut-off grade of 50 g/t AgEq within a conceptual pit shell, which has been limited to the base of the transition mineralization.

(6) The results from the pit optimization are used solely for the purpose of testing the “reasonable prospects for economic extraction” by an open pit and do not represent an attempt to estimate mineral reserves. There are no mineral reserves on the Property. The results are used as a guide to assist in the preparation of a Mineral Resource statement and to select an appropriate resource reporting cut-off grade.

(7) It is envisioned that parts of the Pitarrilla deposit (sulphide mineralization) may be mined using underground mining methods. Underground (below-pit) Mineral Resources are estimated from the bottom of the pit (base of transition mineralization) and are reported at a base case cut-off grade of 150 g/t AgEq. The underground Mineral Resource grade blocks were quantified above the base case cut-off grade, below the constraining pit shell and within the constraining mineralized wireframes. At this base case cut-off grade the deposit shows good deposit continuity with limited orphaned blocks. Any orphaned blocks are connected within the models by lower grade blocks and are included in the Mineral Resource estimate.

(8) Based on the size, shape, location and orientation of the Pitarrilla deposit, it is envisioned that the deposit may be mined using low cost underground bulk mining methods (i.e. longhole mining).

(9) High grade capping of Ag, Pb and Zn was done on 1.50 metre composite data.

(10) Bulk density values were determined based on physical test work from each deposit model and waste model.

(11) AgEq Cut-off grades consider metal prices of $22.00/oz Ag, $1.00/lb Pb and $1.30/lb Zn and considers variable metal recoveries for Ag, Pb and Zn: oxide and transition mineralization - 75% for silver, 70% for Pb and 65% for Zn; sulphide mineralization - 86% for silver, 91% for Pb and 85% for Zn.

(12) The pit optimization and in-pit base case cut-off grade of 50 g/t AgEq considers a mining cost of US$2.50/t rock and processing, treatment and refining, transportation and G&A cost of US$22.40/t mineralized material, an overall pit slope of 42° for oxide and 48° for transition and metal recoveries. The below-pit base case cut-off grade of 150 g/t AgEq considers a mining cost of US$46.50/t rock and processing, treatment and refining, transportation and G&A cost of US$30.90/t mineralized material.

(13) The estimate of Mineral Resources may be materially affected by environmental, permitting, legal, title, taxation, socio-political, marketing, or other relevant issues.

The database used for the current mineral resource estimate comprises data for 804 surface reverse circulation and diamond drill holes completed in the deposit area, which total 254,386 metres. The database totals 134,441 assay intervals for 188,816 metres.

The mineral resource estimate is based on 19 three-dimensional (“3D”) resource models representing oxide, transition and sulphide mineralization, as well as 9 lithological 3D solids and a digital elevation surface model. The main Pitarrilla deposit generally strikes 330° to 335° and dips/plunges steeply east-northeast (-60° to -65°). The oxide mineralization in the Cordon Colorado and Javelina Creek Zones extend for 700 to 900 metres southwest and northeast of the main Breccia Ridge Zone.

Silver, lead and zinc were estimated for each mineralization domain in the Pitarrilla deposit. Blocks within each mineralized domain were interpolated using 1.5 metres capped composites assigned to that domain. To generate grade within the blocks, the inverse distance squared (ID 2 ) interpolation method was used for all domains.

Project Description

Pitarrilla is a large undeveloped silver, lead, and zinc project located 160 kilometres north of Durango City, in northern Mexico. The project is within the Municipality of Santa María del Oro and Indé on the eastern flank of the Sierra Madre Occidental mountain range. The property comprises 4,950 hectares across five concessions and has significant infrastructure in place with direct access to utilities.

As a grassroots discovery in 2002 by SSR Mining Inc. (NASDAQ/TSX: SSRM; ASX: SSR) ("SSR Mining"), the project was held and owned by its subsidiary, SSR Durango, S.A. de C.V. From 2003 to 2012, SSR Mining conducted extensive drill campaigns on the project. Concurrently, SSR Mining published two technical reports, consisting of a prefeasibility study in 2009 focused on a high-grade underground mine scenario and a feasibility study in 2012 which evaluated an open-pit concept. In September of 2020, SSR Mining merged with Alacer Gold, whereby the resulting entity became a gold focused company.

Endeavour completed the purchase of the Pitarrilla Project from SSR Mining in July 2022, for total consideration of US$70 million and a 1.25% net smelter returns royalty. The acquisition is an excellent fit for Endeavour’s regional team in Mexico and enhances the Company’s growth pipeline together with the Terronera and Parral projects. Endeavour agreed to incur a minimum of US$10 million in exploration expenditures on Pitarrilla over the next five years. Endeavour plans to evaluate various production alternatives, including an underground option, which would strengthen the long-term production profile of the Company and provide significant value to shareholders.

National Instrument 43-101 Disclosure

The 2022 Pitarrilla NI 43-101 technical report is authored by Allan Armitage, Ph.D., P. Geo., (“Armitage”) of SGS Geological Services, and the Mineral Resource Estimate presented in the report was estimated by Armitage. Armitage is an independent Qualified Person as defined by NI 43-101 and is responsible for the Mineral Resource Estimate and all sections of the technical report. Armitage has reviewed and approved the contents of this news release.

The Technical Report is available for download under the Company's profile on SEDAR (www.sedar.com) and on the Company's website ( www.edrsilver.com ). There are no material differences in the Technical Report from the information disclosed in the News Release and the date of filing.

About Endeavour Silver

Endeavour Silver is a mid-tier precious metals mining company that operates two high-grade, underground silver-gold mines in Mexico. Endeavour is currently advancing the Terronera mine project towards a development decision, pending financing and final permits and exploring its portfolio of exploration and development projects in Mexico, Chile and the United States to facilitate its goal to become a premier senior silver producer. The Company’s philosophy of corporate social integrity creates value for all stakeholders.

SOURCE Endeavour Silver Corp.

Contact Information

Galina Meleger, Vice President of Investor Relations

Tel: (604) 685-9775

Email: gmeleger@edrsilver.com |

|

|

|

Post by Entendance on Dec 25, 2022 8:03:33 GMT -5

|

|

|

|

Post by Entendance on Dec 30, 2022 3:43:22 GMT -5

|

|

|

|

Post by Entendance on Jan 10, 2023 7:34:27 GMT -5

Endeavour Silver tops full-year production target on Guanacevi strength