|

|

Post by Entendance on Oct 25, 2015 3:14:30 GMT -5

Here one of the best Gold Videos ever...the new video from Jim Rickards called*** 'The Great Gold Hoax.' Must watch it!

...Every gram of gold or silver you acquire using fiat currency effectively removes that many “dollars” from the current financial and economic system. What you have done is removed those “dollars” from the hands of government. They now have fewer “dollars” to use to purchase weapons of war, surveillance technology and the other weapons they use against us. Today would be a good day to remove a few “dollars” from their hands and place another weapon in your back pocket. Gold and silver are free from tyranny, accepted around the world in good faith and provides a piece of insurance from, what appears to be, a system in change...

Your Money In The Bank Will Be Gone For anyone who has money in the bank today, it is virtually guaranteed that in the next 5-7 years either the bank will be gone or the money will be worthless, or probably both.

Governments and Central Banks are now supreme experts in the total destruction of your money.

They are constantly adding new methods so let’s just look at a few of them:

*Zero or Negative interest rates – Over time, together with bank charges, your money will slowly be confiscated.

*Bail-ins – No one will bail you out. Instead the insolvent banks will take your money to save the bank.

*Ban cash – Within a few years, cash will be virtually banned in many countries. So you will not see your money again and the bank and the government will tell you what you can do with it.

*Forced savings in government bonds – Bankrupt governments will force you to invest in bonds for 30 years or longer. The bonds will be worthless at maturity.

*Money Printing – Finally if the money isn’t already gone, governments will totally destroy it by printing so much that it will become worthless.

The world is now starting the final phase of the failed experiment in creating wealth and prosperity for a select few and massive debt and misery for the masses.

It all started with the creation of the Fed in 1913. This led to a global credit creation and money printing extravaganza of a magnitude that the world has never seen before. We have now reached the point when it makes no difference who becomes US president or what the Fed or the IMF will do. No, now we are at the point that von Mises so succinctly defined:

“There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

The latter is guaranteed – Only Gold will protect you.

-Egon von Greyerz

Sell everything whose value only exists as a result of confidence in central bank(ster)s.

(By the time Ferdinand Pecora, slight, soft-spoken son of Italian immigrants, got through with the bankers, Senator Burton Wheeler of Montana was likening them to Al Capone and the public referred to them as “banksters,” rhyming with gangsters.)

Investors without the humility to admit mistakes are not going to last long. On the other hand, good investors who are willing to analyze their mistakes and be frank about what environments will and will not favor their strategies have the chance to transcend and become great. Remember: "There is only one corner of the universe you can be certain of improving, and that's your own self.”― Aldous Huxley

Nations deep in the hole China Syndrome The oil pit US Industrial Recession Stocks in bondage The big bond bust Hedge hogs head for the Hills Mideast mania Fed float fled The housing hustle hangs over us Black swans US debt problems Fundamental flaws in the foundation

“Better to preserve capital on the downside rather than outperform on the upside” – William J. Lippman

The safest places in the world to store your gold your silver and your cash

While the world’s central bankers have given us absolutely no reason to trust them, our governments have given us every reason to NOT trust them.

Governments, especially the bankrupt insolvent ones, have a long history of theft, deceit, and plunder. As we have discussed so many times before, confiscation and/or criminalization of gold is not exactly a zero-risk prospect. Not to mention other related risks as litigations and social unrest. Safety deposit boxes where you have ultimate custody of your metal and cash are the best solution.

Why we avoid banks : Allocated gold vs Unallocated gold

The Benefits of a Segregated Gold Vault Account - Silver Vault Account: here

Banks and our money - The rationale behind avoiding the banking system: here

So offshore private vaults may protect against a government and banking system treating our personal wealth as their own.

Jim Grant: "Gold is an Investment of Disorder of Money as Manipulated & Managed by the Central Bankers"

***Here*** your complete list of secure, non-bank facilities used to store valuables! Act accordingly.

“I think physical diversification is a very intelligent thing to do because you never know what various governments are going to do that may harm your financial well-being” – Eric Sprott

More here

.

They're Coming For Your Cash.

*******************************************

|

|

|

|

Post by Entendance on Oct 30, 2015 16:19:37 GMT -5

and...own physical precious metals in safe vaults in safe jurisdictions! |

|

|

|

Post by Entendance on Nov 9, 2015 9:13:11 GMT -5

|

|

|

|

Post by Entendance on Dec 16, 2015 6:39:50 GMT -5

|

|

|

|

Post by Entendance on Dec 29, 2015 11:45:31 GMT -5

"...The only way to reverse rising inequality and break the power of the super-wealthy Financial Aristocracy is to stop using their central-bank issued national currencies. When the world ceases to use the Financial Aristocracy's money, their power to accumulate more wealth at the expense of everyone else will disappear..."

If you like this beach, then you can help your friends locate it by letting them know about Fred & EntendanceInvestors Beach.

Let's all make this place a thriving sheltered Club for excellence, education and information!

Sollte dir dieser Strand gefallen, dann kannst du deinen Freunden behilflich sein, indem du sie über Fred & EntendanceInvestors Beach informierst.

Lasst uns gemeinsam diesen Ort zu einen blühenden Club für Vortrefflichkeit, Bildung und Information machen!

|

|

|

|

Post by Entendance on Jan 1, 2016 12:58:28 GMT -5

Sell everything whose value only exists as a result of confidence in central bank(ster)s.

Lo "strano fenomeno" per cui le banche detenevano sempre meno obbligazioni bancarie. Loro sapevano, gli altri no

"Exiting While We Can..." A Crisis Worse than ISIS? Bail-Ins Begin

Bail In:*** nessun conto corrente è al sicuro! Come mettersi in salvo - Claudio Borghi A.

***USCIRE MENTRE ANCORA SI PUO’

***********************

<Caro Roberto,

A volte noi leggiamo le date della Storia, senza renderci conto che tra quelle date, che noi leggiamo in pochi secondi, passano giorni interminabili. L'ascesa al potere di Adolf Hitler è di 4 anni posteriore alla crisi del '29: viene nominato Cancelliere nel Gennaio del '33 e il Reichstag gli conferisce poteri assoluti nel Marzo del '33, ma il Putsch della Birreria a Monaco è del Novembre 1923. Sono circa 3,400 giorni per prendere il potere in Germania. La marea, per usare la tua metafora,che mi pare appropriata, monta e non smette di montare fino al 1 Settembre del 1939, data dell'invasione della Polonia. Altri 1,000 giorni circa. La marea, da lì in poi, salirà fino a provocare disperazione in chi la oppone, sperando che alla fine si inverta. Nell'Agosto del '42 comincia la Battaglia di Stalingrado, che andrà avanti fino alla resa della VI Armata Tedesca a Febbraio del '43. La Battaglia di El-Alamein comincia il 23 Ottobre del 1942 e finisce l'11 Novembre con la disfatta dell'Africa Korps. Sono altri 1,000 giorni, prima che l'Armata Rossa inizi una marcia inarrestabile che si fermerà solo sulle rovine fumanti di Berlino.

Ricontali Roberto, sono oltre ....oltre 5,400 interminabili lunghissimi giorni prima che la marea si fermi, prima che il flusso si inverta. Quello che facciamo qui, quel poco che facciamo noi e quel tanto che fa il Prof. lo facciamo per i nostri figli, certamente non per noi, per me, l'unica cosa che vorrei, è poter tenere su la testa e affermare "io non ho ceduto, io ho combattuto" da uomo libero. Non è poco. E deve bastarci .> Il tempo della Storia **************************************

Bail-ins (and other confiscations) are likely coming. It is only smart to have a LARGE amount of your financial assets outside of the banking system.

The Bail-Ins Are Back! Portugal Slaps Senior Bank Bondholders With €2 Billion Loss (And for those wondering just which institutional investors are holding those, here's a list (note that Allianz and BlackRock are right at the top...) Updated: Creditors Accuse Portugal Of Unfair, Populist Short-Cut In €2 Billion Bank Bail-In

**************************

"We keep watching what is happening in Cyprus with morbid fascination. As a reminder, the unhappy island was the first major “haircut” victim in Europe. Its bankers, who had flagrantly over-traded their capital and won prizes for running “the best banks in Europe” along the way, erroneously believed the repeated promises of assorted EU commissars that Greece would never – never! – be allowed to go bankrupt. Consequently they stuffed their balance sheets to the gills with supposedly risk-free Greek government bonds, only to eventually see them get “haircut” twice in a row..."Revisiting the Greatest Crash in History

Uno Stato che si fa dettare la politica di bilancio dall'estero è un protettorato/una colonia. Chiaro?

Quelli che ‘l’euro era giusto, ma il cambio era sbagliato’

|

|

|

|

Post by Entendance on Jan 10, 2016 6:19:41 GMT -5

Steve Burns: "I base my position sizing in my trades on the fact that I never want to lose more than 1% on any one trade. If I am trading with a $100,000 account, I don’t want to lose more than $1,000 in a losing trade. A stop loss level has to start at the price level that you know you are wrong, and work back to position sizing. If the support level on your trade is $105 for your entry and you set your stop at $100, then you can trade 200 shares with a stop at the $100 price level. 200 X $105 = $21,000 position size for 200 shares. This is about 20% of your total trading capital with about a 5% stop loss on your position that equals a 1% loss of your total trading capital.

1.A 20% position of your total trading capital gives you a potential 5% stop loss on your position to equal 1% of total trading capital.

2.A 10% position of your total trading capital gives you a potential 10% stop loss on your position to equal 1% of total trading capital.

3.A 5% position of your total trading capital gives you a potential 20% stop loss on your position to equal 1% of total trading capital.

The average true range (ATR) can give you the daily range of price movement and help you position size based on your time frame and your stocks volatility. If your entry is $105, your stop is $100, and the ATR is $1, then you have a five days worth of movement against you as a stop.

Start with your stop loss level and volatility to give yourself your position size. The more room you want on your stop determines how big of a position size you can take.

If you only risk losing 1% of your trading capital when you are wrong, then every trade can become just one of the next 100 with little emotional impact. Ultimately, you can survive losing streaks and increase your odds of prosperity."

...how is Druck positioning himself to deal with the consequences of another “central bank mistake”? He recently made a massive bet on gold. The Greatest Money Manager Alive Attributes The Majority His Success To Just This One Thing

|

|

|

|

Post by Entendance on Jan 15, 2016 6:34:03 GMT -5

20 Terrible Ways to Trade Good trading is very basic; it’s trading with an edge to capture a trend in your own time frame, while managing your risk exposure carefully with the right position sizing and stop loss.

There are endless ways to trade badly. You can change these if you make an effort and become self-aware. Be on the lookout for these pitfalls.

*******************Here are the top 20

***Robert V. Green: Trading And Investing Are Different

|

|

|

|

Post by Entendance on Jan 27, 2016 5:58:28 GMT -5

"If the risk-on euphoria of punters borrowing billions of dollars in margin debt doesn't materialize, stocks could languish for years after falling 50%..."

Illusion of Safety: Index Funds Are Not Low-Risk

“When dealing with people, let us remember we are not dealing with creatures of logic. We are dealing with creatures of emotion, creatures bristling with prejudices and motivated by pride and vanity.”

"Why prove to a man he is wrong? Is that going to make him like you? Why not let him save face? He didn't ask for your opinion. He didn't want it. Why argue with him? You can't win an argument, because if you lose, you lose it; and if you win it, you lose it. Why? You will feel fine. But what about him? You have made him feel inferior, you hurt his pride, insult his intelligence, his judgment, and his self-respect, and he'll resent your triumph. That will make him strike back, but it will never make him want to change his mind. A man convinced against his will is of the same opinion still." - Dale Carnegie How to Win Friends and Influence People [PDF here] |

|

|

|

Post by Entendance on Feb 11, 2016 20:34:01 GMT -5

|

|

|

|

Post by Entendance on Feb 15, 2016 11:43:41 GMT -5

|

|

|

|

Post by Entendance on Feb 20, 2016 6:26:57 GMT -5

Sell everything whose value only exists as a result of confidence in central bank(ster)s.

Planets aligning for gold – Macroeconomic unstoppable forces

That’s what happened in Cyprus. The banks were going to the wall. So, they confiscated deposits to help make themselves whole again

The War On Cash Is Increasing

Many don’t notice the stealth war on cash but it’s quite real.

As countries move to negative interest rates the thrust of the policies are to force people to spend. No mattress money allowed thank you. Nations like Japan, Sweden, Denmark and Switzerland have already implemented these policies.

Central Banks are basically charging member banks to hold cash. The superficial belief is to force loan making and spending which will stimulate inflation and growth. The minus rates being applied by the ECB, Denmark, Switzerland, Sweden, and Japan havefailed to juice growth, or stocks, or inflation.

A clear ulterior motive is by eliminating cash, countries will increase tax revenues by negatively effecting the private economy and illegal activities at the same time. A recent move by the ECB is to eliminate the €500 note. This was followed this week by influential economist Larry Summers desires to eliminate the $100 bill. And, so it goes. But clearly the government wishes to squeeze cash transactions. The Central Banks hate physical cash. So much so they there will likely try to ban it in the near future.

You see, almost all of the “wealth” in the financial system is digital in nature.

◾The total currency (actual cash in the form of bills and coins) in the US financial system is a little over $1.36 trillion.

◾When you include digital money sitting in short-term accounts and long-term accounts then you’re talking about roughly $10 trillion in “money” in the financial system.

◾In contrast, the money in the US stock market (equity shares in publicly traded companies) is over $20 trillion in size.

◾The US bond market (money that has been lent to corporations, municipal Governments, State Governments, and the Federal Government) is almost twice this at $38 trillion.

◾Total Credit Market Instruments (mortgages, collateralized debt obligations, junk bonds, commercial paper and other digitally-based “money” that is based on debt) is even larger $58.7 trillion.

◾Unregulated over the counter derivatives traded between the big banks and corporations is north of $220 trillion.

When looking over these data points, the first thing that jumps out at the viewer is that the vast bulk of “money” in the system is in the form of digital loans or credit (non-physical debt).

Put another way, actual physical money or cash (as in bills or coins you can hold in your hand) comprises less than 1% of the “money” in the financial system.

As far as the Central Banks are concerned, this is a good thing because if investors/depositors were ever to try and convert even a small portion of this “wealth” into actual physical bills, the system would implode (there simply is not enough actual cash).

Remember, the current financial system is based on debt. The benchmark for “risk free” money in this system is not actual cash but US Treasuries.

In this scenario, when the 2008 Crisis hit, one of the biggest problems for the Central Banks was to stop investors from fleeing digital wealth for the comfort of physical cash. Indeed, the actual “thing” that almost caused the financial system to collapse was when depositors attempted to pull $500 billion out of money market funds.

A money market fund takes investors’ cash and plunks it into short-term highly liquid debt and credit securities. These funds are meant to offer investors a return on their cash, while being extremely liquid (meaning investors can pull their money at any time).

This works great in theory… but when $500 billion in money was being pulled (roughly 24% of the entire market) in the span of four weeks, the truth of the financial system was quickly laid bare: that digital money is not in fact safe.

To use a metaphor, when the money market fund and commercial paper markets collapsed, the oil that kept the financial system working dried up. Almost immediately, the gears of the system began to grind to a halt.

When all of this happened, the global Central Banks realized that their worst nightmare could in fact become a reality: that if a significant percentage of investors/ depositors ever tried to convert their “wealth” into cash (particularly physical cash) the whole system would implode.

As a result of this, virtually every monetary action taken by the Fed since this time has been devoted to forcing investors away from cash and into risk assets. The most obvious move was to cut interest rates to 0.25%, rendering the return on cash to almost nothing.

However, in their own ways, the various QE programs and Operation Twist have all had similar aims: to force investors away from cash, particularly physical cash.

After all, if cash returns next to nothing, anyone who doesn’t want to lose their purchasing power is forced to seek higher yields in bonds or stocks.

The Fed’s economic models predicted that by doing this, the US economy would come roaring back. The only problem is that it hasn’t. In fact, by most metrics, the US economy has flat-lined for several years now, despite the Fed having held ZIRP for 5-6 years and engaged in three rounds of QE.

As a result of this… mainstream economists at CitiGroup, the German Council of Economic Experts, and bond managers at M&G have suggested doing away with cash entirely.

If you think this sounds like some kind of conspiracy theory, consider that France has a cash ban on any transaction over €1,000 Euros from using physical cash. Spain has a cash ban on transactions over €2,500. Uruguay has cash bans on transactions over $5,000. And on and on.

A cash ban will be coming to the US in the near future. Already, the big banks (the ones with the closest ties to the Federal Reserve) have begun turning away deposits OR charging them.

State Street Corp. , the Boston bank that manages assets for institutional investors, for the first time has begun charging some customers for large dollar deposits, people familiar with the matter said. J.P. Morgan Chase & Co., the nation’s largest bank by assets, has cut unwanted deposits by more than $150 billion this year, in part by charging fees…

And here’s another big “tell”…

“At some point you wonder whether there will be a shortage of financial institutions willing to take on these balances,” said Kelli Moll, head of Akin Gump Strauss Hauer & Feld LLP’s hedge-fund practice in New York, saying that where to hold cash has become an increasing topic of conversation as hedge funds are shown the door by longtime banking counterparties.

So where is the physical cash meant to go?

Jerome Schneider, head of Pacific Investment Management Co.’s short-term and funding desk, which advises corporate and institutional clients, said that as a result of the bank actions, he and his customers have discussed as cash alternatives boosting investments in U.S. Treasury bonds, ultrashort-duration bond funds and money-market funds.

When it comes to cash, Mr. Schneider said, “Clients have been put on warning.”

Source: Wall Street Journal.

This is just the beginning. Indeed… -Graham Summers |

|

|

|

Post by Entendance on Feb 22, 2016 2:46:01 GMT -5

"...When Italy finally succumbs to reality, this year or next, the European project as they call it will face insurmountable hurdles and collapse on itself. In our view, seeing the parasitical edifice in Brussels disappear can only lead to good things.

Maybe the Brits will save us the agony and end it June 23rd. One can only hope."

How Italy will fail and drag down the European Project

Sell everything whose value only exists as a result of confidence in central bank(ster)s. |

|

|

|

Post by Entendance on Mar 3, 2016 17:26:11 GMT -5

***This 4,000-year old financial indicator says that a major crisis is looming ***This 4,000-year old financial indicator says that a major crisis is looming

The Collapse Of Italy’s Banks Threatens To Plunge The European Financial System Into Chaos The Collapse Of Italy’s Banks Threatens To Plunge The European Financial System Into Chaos

GOLD – GETTING SET FOR THE GREATEST BULL MARKET OF ALL TIME  "Gold, unlike all other commodities, is a currency...and the major thrust in the demand for gold is not for jewellery. It's not for anything other than an escape from what is perceived to be a fiat money system, paper money, that seems to be deteriorating." "Gold, unlike all other commodities, is a currency...and the major thrust in the demand for gold is not for jewellery. It's not for anything other than an escape from what is perceived to be a fiat money system, paper money, that seems to be deteriorating."

Alan Greenspan, ex-US Federal Reserve Chairman, August 23, 2011

"Gold still represents the ultimate form of payment in the world. Fiat money in extremis is accepted by nobody. Gold is always accepted."

Alan Greenspan, May 20, 1999

Gold And Silver: Governments And Central Banks Are Losing Control

"You’re never going to save everyone. There are some people that are never going to get it. It’s sad, but true.

There will always be investors that can’t help themselves or get out of their own way.

I used to think everyone could be saved if they would only learn. But changing behavior is simply too difficult for many.

In order for one group of investors to prosper, another group has to fail. It’s an unfortunate truth of the financial markets."

-Ben Carlson

Got Silver?

Fred & EntendanceInvestors Beach Top Silver Stock: EXK Endeavour Silver Corp

|

|

|

|

Post by Entendance on Mar 23, 2016 14:32:48 GMT -5

"...you don’t have to be a radical to review your bank’s financial statements and find, for example, that US Bank maintains cash reserves amounting to just 3.5% of its customer deposits.

Or that Italy’s Unicredit Bank holds cash reserves of just 1.7% of its customer deposits..."

If your country’s broke, don’t hold all of your savings there |

|

|

|

Post by Entendance on Apr 5, 2016 9:08:08 GMT -5

That says it all as far as any ECB's credibility left. Banksters.

“Why do they hate gold so much?”

That one is easy—the central bankers and their crony politicians hate gold for the same reason tanning salons hate the sun. Because gold cannot be printed or destroyed, it exists in limited and quantifiable amounts, and therefore, unlike paper money, there is a limit, a tether, on the amount of incompetence and financial mismanagement our elected governments can get away with without being called to account.

On the other hand, the amount of paper (or digital) currency that a government can create (usually through the mechanism of its “agent,” or third-party central bank) is limited only by the amount of available ink and paper, the processing capacity of its computer systems, and the ignorance of its citizens. And all of these are now in plentiful supply, it would seem.

Everything that needs to be said has already been said. But since no one was listening, everything must be said again.

-André Gide

|

|

|

|

Post by Entendance on Apr 18, 2016 4:49:38 GMT -5

|

|

|

|

Post by Entendance on May 3, 2016 10:45:58 GMT -5

"When you see that in order to produce, you need to obtain permission from men who produce nothing;

when you see that money is flowing to those who deal not in goods, but in favors;

when you see that men get rich more easily by graft than by work;

and your laws no longer protect you against them, but protect them against you;

...you may know that your society is doomed."

Atlas Shrugged - Ayn Rand

Act accordingly. E.

|

|

|

|

Post by Entendance on May 18, 2016 11:54:29 GMT -5

WAR ON CASH UPDATE

The Shift to a Cashless Society is Snowballing

Love it or hate it, cash is playing an increasingly less important role in society.

In some ways this is great news for consumers. The rise of mobile and electronic payments means faster, convenient, and more efficient purchases in most instances. New technologies are being built and improved to facilitate these transactions, and improving security is also a priority for many payment providers.

However, there is also a darker side in the shift to a cashless society. Governments and central banks have a different rationale behind the elimination of cash transactions, and as a result, the so-called “war on cash” is on.

On the Path to a Cashless Society

The Federal Reserve estimates that there will be $616.9 billion in cashless transactions in 2016. That’s up from around $60 billion in 2010.

Despite the magnitude of this overall shift, what is happening from country to country varies quite considerably. Consider the contradicting evidence between Sweden and Germany.

In Sweden, about 59% of all consumer transactions are cashless, and hard currency makes up just 2% of the economy. Yet, across the Baltic Sea, Germans are far bigger proponents of modern cash. This should not be too surprising, considering that the German words for “debt” and “guilt” are the exact same.

Within Germany, only 33% of consumer transactions are cashless, and there are only 0.06 credit cards in existence per person.

The Dark Side of Cashless

The shift to a cashless society is even gaining momentum in Germany, but it is not because of the willing adoption from the general public. According to Handelsblatt, a leading German business newspaper, a proposal to eliminate the €500 note while capping all cash transactions at €5,000 was made in February by the junior partner of the coalition government.

Governments have been increasingly pushing for a cashless society. Ostensibly, by having a paper trail for all transactions, such a move would decrease crime, money laundering, and tax evasion. France’s finance minister recently stated that he would “fight against the use of cash and anonymity in the French economy” in order to prevent terrorism and other threats. Meanwhile, former Secretary of the Treasury and economist Larry Summers has called for scrapping the U.S. $100 bill – the most widely used currency note in the world.

“Smoother” Aggregate Demand?

It’s not simply an argument of the above government rationale versus that of privacy and anonymity. Perhaps the least talked-about implication of a cashless society is the way that it could potentially empower central banking to have more ammunition in “smoothing” out the way people save and spend money.

By eliminating the prospect of cash savings, monetary policy options like negative interest rates would be much more effective if implemented. All money would presumably be stored under the same banking system umbrella, and even the most prudent savers could be taxed with negative rates to encourage consumer spending.

While there are certainly benefits to using digital payments, our view is that going digital should be an individual consumer choice that can be based on personal benefits and drawbacks. People should have the voluntary choice of going plastic or using apps for payment, but they shouldn’t be pushed into either option unwillingly.

Forced banishment of cash is a completely different thing, and we should be increasingly wary and suspicious of the real rationale behind such a scheme.

|

|

|

|

Post by Entendance on May 26, 2016 7:22:51 GMT -5

No productivity growth. None.

"...If one simply looks at the following line-items, it is clear for anyone to see something is about to hit the fan and it’s not anything anyone wants hitting the fan.

•45 million people in the U.S. on food stamps

• some estimates as high as 10 million refugees flooding into the European Union

•non-stop wars of aggression involving NATO, Russia, Syria and several other countries

• financial crisis that began in 2008 has not been addressed and the problems that started that year have grown larger and far deeper

•banking system in the European Union, especially Italy, is under enormous stress due to faulting/fraudulent accounting

•Federal Reserve balance sheet at $4 TRILLION – U.S. debt at $20 TRILLION and counting

•United Kingdom/Britain and the Brexit movement that is taking root

•U.S. Presidential candidates, Donald Trump and Bernie Sanders, garnering global attention as the citizens of the U.S. seek alternatives to the current embedded criminal politicians.

• Japan instituting a Negative Interest Rate Policy (NIRP) for their sovereign bonds – Japan has basically been in a recession for over 20 years

•China is manufacturer to the world and with economies slowing down or shutting down, there is no reason to manufacture products..." A Crisis Unlike We Have Seen In Human History

|

|

|

|

Post by Entendance on May 31, 2016 16:01:35 GMT -5

|

|

|

|

Post by Entendance on Jun 12, 2016 3:31:24 GMT -5

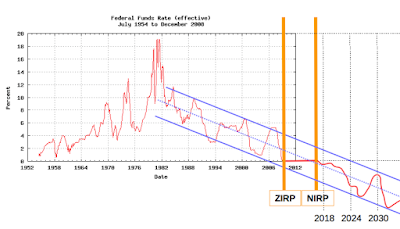

1. Why did zero interest rates become necessary?

2. Why are negative interest rates now necessary? and,

3. Why are negative interest rates a really excellent idea?*

* if you ignore certain unintended consequences (which is what everyone does all the time, so let’s not worry about them just yet).

1. Interest rates went to zero because economic growth went to zero. If you are just now wondering why that happened, just google “Limits to Growth” by clicking this link. (A public notice about the scheduled end of growth has been on display at your global planning office for four decades now. It is not anyone else’s fault if people of this planet don’t take an interest in their global affairs. I mean, seriously…)

Interest rates and rates of growth are related: a positive interest rate is little more than a bet that the future is going to be bigger and more prosperous, enabling people to pay off the debts with interest. This is an obvious point: if your income increases, it becomes easier to repay your debts; if it stagnates, it becomes harder; if it shrinks, it eventually becomes impossible.

Yes, you can nitpick and split hairs, and claim that there was still some growth, but in the developed economies most of this growth has been in financial shenanigans, fueled by an explosion in debt, and most of the benefits of this last bit of growth accrued to the wealthiest 1%, and did next to nothing for anyone else. Did this growth help support a large, stable and prosperous middle class? No, it didn’t.

In fact, wages in the US, which was once the world’s largest economy, have been stagnant for generations. In response, the Federal Reserve has been continuously reducing interest rates, until they hit zero in 2008. And there they have stayed ever since. But now, it turns out, that’s not good enough. If the Federal Reserve wants to keep the party going, they have to do more, because…

2. Once you are faced with a continuously shrinking economy, just holding interest rates at zero is not sufficient to forestall financial collapse. The interest rates must go negative.

Here are just a couple of particularly striking examples.

Australia has amassed a huge pile of debt—over 120% of GDP—and most of it is mortgage debt on overvalued real estate. Now that Australia’s economy, which was driven by commodity exports to China, has tanked, a lot of this debt is being turned into interest-only loans, because Australians no longer have the money to repay any of the principal. But what if they can’t make the interest payments either? The obvious solution is to refinance their mortgages as interest-only at zero percent; problem solved! Of course, as conditions deteriorate further, the Australians will become unable to afford taxes and utilities. Negative interest rates to the rescue! Refinance them again at a negative rate of interest, and now the banks will pay them to live in their overpriced houses.

Another example: energy (oil and gas) companies in the US have accumulated a fantastic pile of debt. All of this money was sunk into developing marginal and very expensive resources such as shale oil and deep offshore. Since then, energy prices have fallen, making all of these investments unprofitable and dramatically reducing revenue. As a result, energy companies in the US are a few months away from having to spend their entire revenue on interest payments. The solution, of course, is to allow them to roll over their debt at zero percent, and if you want them to ever start drilling again (their production has been falling by around 10% annualized) then please make that interest rate negative.

3. Are you starting to see how this works? Whereas before you had to be careful about taking on debt, and had to have a plan for how you will repay it, with negative interest rates that is simply not a consideration. If your debt pays you, then more debt is always better than less debt. It no longer matters that the economy continuously shrinks because now you can get paid just for twiddling your thumbs!

But are there any unintended consequences of negative interest rates? Unintended consequences are hard to think about, and most people get a headache even trying. How can it be that clean, plentiful nuclear energy will eventually pollute the whole planet with long-lived radionuclides, resulting sky-high cancer rates? How can it be that wonderful genetically modified seeds will render us sickly and infertile in just a few generations? And how can it be that ingenious mobile computing technology has turned our children into zombies who are constantly twiddling their smartphones as they sleepwalk through life? It’s hard to think about any of this without taking some happy pills; and how can it be that taking those happy pills has… you get the idea.

The unintended consequence of negative interest rates is that they destroy money. This is true in an entirely trivial sense: if you deposit x dollars at -ρ% annual, then a year later you will only have x(1-ρ) dollars because xρ dollars has been destroyed. (In case you prefer to count on your fingers and toes, if you deposit $10 at -10% annual, then a year later you will only have $9 because $1 has been destroyed.) But what I mean is something slightly more profound: negative interest rates erode the very concept of money.

To get at the reason for this, we have to ask a slightly more profound question: What is money? I think that money is the cult of the god Mammon. Look at the following symbols:

€ $ ¥ £

Don’t they resemble religious symbols? In fact, that’s what they are: they are symbols of faith in money. They are also units—dimensionless units, of a peculiar kind. There are quite a few dimensionless units in math and science, such as π, e, %, ppm, but they are all ratios that relate physical quantities to other, identical, physical quantities. They are dimensionless because the units cancel out. For instance, π is the ratio between a circle’s circumference and diameter; length over length gives nothing. But monetary quantities do not directly relate to any physical quantity at all. It can be said that some number of monetary units (let's call them "yarbles") is equivalent to some number of turnips, but that, you see, is a matter of faith. Should the turnip farmer turn out to be an unbeliever, he would be within his rights to say, “I am not taking any of your damn yarbles!” or, if he were a polite turnip farmer, “Your money is no good here, Sir!”

Of course, if our turnip farmer were to do that, he’d land in quite a bit of trouble because, you see, the cult of Mammon is a state cult. You have no choice but to be a believer, because only by worshiping Mammon can you earn the money to pay your taxes, and if you don’t pay your taxes you get jailed. Nor can you produce money on your own, because that right is reserved for Mammon’s high priests, the bankers. Making your own money makes you a heretic, and gets you the modern equivalent of being burned at the stake, which is a $250,000 fine and a 20-year prison sentence.

But it goes beyond that, because the state insists that just about everything there is must be valued in units of its money. And the way everything must be valued is through a mystical legitimizing process that is central to the cult of money: Mammon’s “invisible hand” makes itself apparent within the “free market,” which is Mammon's virtual temple. The “invisible hand” sets the price of everything as a mystical revelation and, as with any revelation, it is beyond criticism. It is a redemptive ritual, in which people acting out of their basest, most antisocial instincts—greed and fear—manage, through Mammon's divine intervention, to serve the common good. The “free market” is also believed to have all sorts of miraculous properties, and as with all miracles it is all a matter of smoke and mirrors and suspension of disbelief. For example, the “free market” is said to be “efficient.” But it sets the price of turnips, and the result is that fully 40% of the food in the US ends up being wasted. That’s definitely not efficient.

This sort of inefficiency can be tolerated while resources are plentiful. Should throwing away 40% of the turnips cause a shortage of turnips develop, turnip producers can grow more turnips and sell them at prices that turnip consumers can still afford. But when resources are no longer plentiful, this trick stops working, and what you end up with is something called market failure. The current state of the global oil industry is a good example: either the price is so high that marginal consumers cannot afford it (as was the case until quite recently), or the price is so low that the marginal producers can’t break even (as is the case now).

And so a bout of supply destruction follows a bout of demand destruction, and then the pattern repeats. Everybody loses, plus this is terribly inefficient. It would be far more efficient to appoint some central planner to calculate the optimum price of oil once a month. Then all the marginal producers would jump out the window, all the marginal consumers would slit their wrists, and equilibrium conditions would prevail. As the oil supply dwindled (it is depleting at around 5% per year), some additional number of producers and consumers would need to sacrifice themselves for the greater good, and so on until the last barrel is produced and burned, leaving whatever producers and consumers still remained lying in pools of their own blood.

As natural resources dwindle, our faith in the cult of Mammon is being sorely tested. But what alternatives are there? Well, there is an even older, ancient cult that’s based on idolatry: the worship of precious metals. Gold has some industrial and aesthetic uses, but it is primarily useful for making a golden calf for you to worship (or, if you are former Ukrainian president Viktor Yanukovich, a golden toilet). Economists tell us that gold is a “pet rock” or a “barbarous relic,” and they are right, but what is one to do when there is a Götterdämmerung (twilight of the gods) going on? Nature abhors a vacuum, and in a Götterdämmerung older pagan deities sometimes emerge and demand virgin sacrifices—such as poisoning entire river ecosystems by mining gold using mercury, or squandering prodigious amounts of fossil fuels in mining, crushing and sifting through millions of tons of hard rock to get at just 3 parts per million of gold.

Negative interest rates are Mammon’s Götterdämmerung. The money cult is bolstered by the idea that its huge and all-powerful deity will be even more huge and all-powerful tomorrow; if the opposite is demonstrably the case, then people’s faith in it begins to falter and fade. Negative interest rates are like an icy-cold bath for Mammon, causing its godhead to shrink a little more with every dip. People see that, and think, “I don’t want to worship his shrinking yarbles.” Then they go and spend their own yarbles on anything they can find—fallow land, vacant houses, golden calves, boxes of brass knobs... They don’t bother investing their yarbles in growing turnips, because what’s the use of turnips if all you can do with them is sell them for even more shrinking yarbles?

Negative interest rates are an excellent idea—and perhaps the only way to keep the financial game going a bit longer—but, given these unintended consequences, they are also a terrible idea. The bankers know that. They want to preserve their cult’s status, and constantly talk about raising interest rates. But they haven’t yet, because they also know that just a small increase will result in trillions of dollars of losses, triggering widespread business failures and ushering in the Greatest Great Depression Ever. This is not a problem for them to solve; this is a predicament. They will delay and pray, and make pronouncements loaded with keywords designed to please the high-frequency trading algorithms that are in charge of artificially levitating the “free market” with judiciously timed injections of “free money.” But in the end all they can do is act brave, wait for a distraction and then… run for the exits!

And your job is to make it to the exits before they do. -ClubOrlov

"...The time to rebel against it is now, while we still have the chance before that boot tramples the face of humanity…forever..."

|

|

|

|

Post by Entendance on Jul 13, 2016 18:47:07 GMT -5

"...the banking crisis of 2008 never fully healed.

It just got shuffled under the carpet while the public was fed a phony narrative that everything is fantastic.

This turned out to be a gigantic farce; many of the world’s banking systems are just as risky as they were back in 2008.

Do yourself a favor: don’t keep 100% of your savings trapped in a risky banking system.

What’s the point? They’re only paying you 0.1% anyhow. Why take on so much risk?

If you have savings of even more than $10,000 (and definitely if you’re in the six to seven figure range), move some funds to a stronger, better capitalized banking system abroad.

And definitely consider owning precious metals, plus holding at least a month’s worth of expenses in physical cash in a safe at your home.

Given how low interest rates are, you won’t be any worse off. But should Bancopalypse 2.0 be upon us, cash and gold could end up being a phenomenal insurance policy."

***Some disturbing figures about the upcoming banking crisis

|

|

|

|

Post by Entendance on Jul 28, 2016 12:51:43 GMT -5

"...The crucial thing to understand about credit bubble dynamics is that borrowing money from people desperate to lend and using the proceeds to overpay for assets requires only monkey-level intelligence. So while a bubble is inflating it’s impossible for most of the media, banking and political communities to tell the legitimate operators from the hopelessly corrupt and/or extremely stupid. That’s the world we’ve created by handing monetary printing presses to governments, and by extension to corporate CEOs.

Today’s bubble is global, as capital sloshes from one country to the next in search of safety and/or yield. So this time around virtually all major governments have been corrupted, and now every country’s major corporations are about to suffer the same fate. We have, in short, the mother of all crack-up booms coming our way..."

Corrupt Or Just Stupid? Markets Hand Corporations An Unlimited Credit Card

|

|

|

|

Post by Entendance on Aug 15, 2016 4:14:51 GMT -5

New: Welcome to Eurabia, formerly known as Europe.

"...avoid banking in countries that are heavily-indebted; those are the places most likely to run into serious problems, and you don’t want your money anywhere near them. Physical cash and precious metals can be an excellent substitute for bank deposits, especially as interest rates continue to slide below zero...." The worst place in the world to bank:*** Europe |

|

|

|

Post by Entendance on Aug 24, 2016 3:59:43 GMT -5

|

|

|

|

Post by Entendance on Sept 1, 2016 11:26:57 GMT -5

Great traders, like great poker players, know when to play and when to fold their cards and wait for something worth betting on. Too often, the love of trading expresses itself as a need to trade, and the need to trade leads players to play the wrong hands. Worse yet, the need to trade leads players to sit at the wrong tables. If you're at the wrong poker table, the hands you draw won't really matter.

Folding your cards means that you're properly focused on opportunity, but the opportunity isn't present, right here and right now. Yesterday, I wanted to be a buyer of stocks, but volume was waning through the day. That tells me that momentum and follow-through on moves will be limited. I want to buy weakness, not try to ride breakout strength. If the market is showing me strength and I don't want to chase it, I've got the wrong hand and I'll wait for the pullback to give me better cards. A great poker player is a patient one.

But let's say that I'm stumble onto a Vegas floor and plop myself down at the first table where I see an opening. Had I stood by and watched play for a while, I would have recognized that these are experienced sharks waiting for some bait. Instead, I start playing at the wrong table and become the bait. That happens in markets when we force our trading style onto markets that are moving a very different way. If I'm a trend following investor who places bets based on central bank policy and those policies have radically changed from their norm, I'm at the wrong table. I'm playing the wrong game.

If you're in drawdown mode, it's important to ask if the problem is with your betting versus folding or if the problem is sitting at the wrong table or playing the wrong game altogether. Are your tactics needing adjustment, or do you need a different strategy? The most important thing you can do when you're in an unusual drawdown is figure out why you're drawing down.

There are three big reasons why people have big drawdowns:

1) They're trading a strategy that doesn't fit the present market;

2) They're trading the right strategy, but their head isn't in the game and they're not following their strategy;

3) They're trading the right strategy with a good mindset, but they're employing the wrong tactics and thus not implementing their strategy the right way.

You can't cure a drawdown if you can't come up with the right diagnosis. Sometimes coming up with that diagnosis means you fold the cards for a while and focus on studying yourself and your trading rather than just studying markets. Risk management is key because it keeps drawdowns manageable, so that you're sure to have time to learn from them. The key is folding your cards before you lose your stack. -Brett Steenbarger, Ph.D.

|

|

|

|

Post by Entendance on Sept 22, 2016 4:52:45 GMT -5

Recall the Cypriot banking crisis a few years back. Ultimately, 47.5% of bank deposits over €100,000 were confiscated overnight as they were converted

into bank equity for a loss of roughly €4 billion! Your Bank Deposits May Become Your Worst Nightmare

Bank Bail-Ins – Depositors’ Worst Nightmare

***How You Could Lose Your Money in The Bank |

|

|

|

Post by Entendance on Oct 7, 2016 6:34:25 GMT -5

|

|

|

|

Post by Entendance on Nov 7, 2016 9:56:36 GMT -5

NEW!

Michael Krieger: The following video is a must watch.

It’s called “Rules for Rulers” and it brings home the point that, if we want to make the world a better place, we better understand how the world works.

Enjoy.

For eighteen years, Bruce Bueno de Mesquita and Alastair Smith have been part of a team revolutionizing the study of politics by turning conventional wisdom on its head. They start from a single assertion: Leaders do whatever keeps them in power. They don’t care about the “national interest”—or even their subjects—unless they have to.

|

|