|

|

Post by Entendance on Dec 20, 2022 6:18:55 GMT -5

McEwen Mining: New, Near Surface, High Grade Beside Our Mill

December 19, 2022

264.5 g/t Au Over 2.4 m Uncapped (12.6 g/t Au Over 2.4 m Capped); A Holiday STOCK-ing Stuffer

TORONTO, Dec. 19, 2022 -- McEwen Mining Inc. (NYSE: MUX) (TSX: MUX) is pleased to report the latest exploration news from its Stock property. We discuss four priority areas that illustrate the potential to expand the gold resource base around the historic Stock mine.

“We find the occurrence of near surface high grade at our Stock Mill’s doorstep very intriguing. These initial results have mineable grades and widths, which are encouraging f rom an economic perspective as they compare favourably to the Stock mine’s historic grade of 5.5 g/t Au. ”, stated Stephen McGibbon, EVP Exploration.

Area 1: Near Surface @ Stock Mine

Figure A shows a longitudinal section profiling Areas 1 & 2. Drill hole SM22-110 (shown in upper right corner) produced two attractive assay results within 30 meters (m) of surface. The first of these shallow intercepts, started after 15 m from surface, was 8.0 grams per tonne gold (g/t Au) over 4.6 m. The second intercept, following within 5 m further downhole, had an assay value of 264.5 g/t Au uncapped or of 12.6 g/t Au capped over 2.4 m, which included an assay of 1,031.6 g/t Au over 0.6 m (see Table 2). The results of SM22-110 represent an extension of mineralization east of SM22-059 and SAS-66 which delivered assay values of 11.6 g/t Au over 3.1 m and 6.3 g/t Au over 3.5 m, respectively. This result has opened a new high grade target area of some 300 m in length. Further east again, coarse and fine visible gold was encountered in SM22-116, with assay results pending.

Area 2: Around Existing Stock Mine Workings

A second area with multiple intercepts located 225 m to 280 m below surface (left side of Figure A) includes SM22-090 with 6.6 g/t Au over 6.1 m within a broader envelope of 4.4 g/t Au over 10.5 m and SM22-070 with 5.5 g/t Au over 6.5 m within 3.6 g/t Au over 15.0 m. This area is of interest as it has potential to host new mineral resources of economic gold grades with attractive widths. Proximity to our processing facilities (Stock Mill) increases the likelihood for these results to support attractive operating margins...

...The Stock property, part of the Fox Complex, covers 5 miles (8 km) along the Destor-Porcupine Fault Zone (DPFZ) and associated geological structures. It is the site of the historic Stock Mine and of the Stock Mill, where the material from our Black Fox and Froome mines is processed. When the Stock mine ceased mining in 1994, due to low gold price, it produced 137,000 gold ounces at a grade of 5.5 g/t. While most of the mines along the DPFZ have reached depths of greater 1,000 m, the Stock mine has only been mined down to a depth of 330 m.. Our recent exploration success has built a resource of 265,000 gold ounces Indicated and 119,000 gold ounces Inferred, all within 500 meters of surface. Recent drill results suggest the mineralization continues deeper... |

|

|

|

Post by Entendance on Dec 22, 2022 6:16:51 GMT -5

McEwen Mining Operations Performing Better Production Up, Costs per Ounce Down

McEwen Mining Inc. (NYSE: MUX) (TSX: MUX) is pleased to report our production for October and November along with our forecast for 2022 and guidance for 2023. The bottom line, production is increasing and costs per ounce are falling.

“As we end 2022, we would like to give our shareholders an update on our recent production results and costs which illustrate the turnaround we are executing as well as our guidance for 2023. We had a difficult start to 2022 but it is clear that we are trending up and in the right direction as we move into the new year.” said Rob McEwen, Chairman and Chief Owner.

Table 1 here provides production and cost results for 2021, October and November 2022, full year 2022 forecast, our production guidance range for full year 2022, and 2023 guidance. Our El Gallo project in Mexico produced approximately 900 GEOs in 2022 through residual heap leaching, which ceased in July 2022; these figures are not included separately.

Notes:

'Gold Equivalent Ounces' are calculated based on a gold to silver price ratio of 72:1 for Q4 2022, 90:1 for Q3 2022, 83:1 for Q2 2022, 78:1 for Q1 2022. 2022 and 2023 guidance is calculated based on 85:1 gold to silver price ratio. A ratio of 72:1 was used for 2021.

Cash costs per ounce sold, all-in sustaining costs (AISC) per ounce sold are non-GAAP financial performance measures with no standardized definition under U.S. GAAP. For definition of the non-GAAP measures see "Non-GAAP Financial Measures" section in this press release; for the reconciliation of the non-GAAP measures to the closest U.S. GAAP measures, see the Management Discussion and Analysis for the year ended December 31, 2021 (as amended) filed on Edgar and SEDAR.

Represents the portion attributable to us from our 49% interest in the San José Mine.

From the “Q3 2022 Results” news release dated November 7, 2022.

Our 100% owned El Gallo project in Mexico produced approximately 900 GEOs in 2022 through residual heap leaching, which ceased in July 2022; El Gallo produced 3,700 ounces in 2021; these figures are not included separately.

Total production for October and November was approximately 26,700 gold equivalent ounces(1) (GEOs) with preliminary costs per ounce from our 100%-owned operations of $826 for cash costs and $1,088 for all-in sustaining. At San José Mine, costs per ounce for October and November were of $1,361 for cash costs and $1,745 for all-in sustaining.

Consolidated production guidance for 2023 represents an 11% to 25% increase to 150,000 to 170,000GEOs from 2022 forecast production, with $1,200 cash costs per ounce and $1,500 all-in sustaining costs per ounce from 100%-owned operations and $1,250 cash costs per ounce and $1,550 all-in sustaining costs per ounce from the San José Mine. Cash costs per ounce are expected to decrease slightly compared to 2022 and all-in sustaining costs per ounce are expected to decrease 6% at our 100% owned operations and decrease 10% at the San José Mine in 2023 compared to 2022.

Gold Bar, Nevada

At Gold Bar we hired a new mining contractor who was moving equipment and personnel to the mine during October and November. As a consequence, there was very little mining done, thus the mining expense incurred was small. However, gold production continued as we had a large stockpile of ore that was loaded on the heap leach pad and leaching continued during this time.

Costs per ounce in 2023 are expected to be lower than in 2022, and gold production is expected to jump higher due to mining from our Gold Bar South deposit. Its ore has a higher grade (concentration of gold per ton), half the strip ratio (the amount of rock that is required to be moved to reach the ore), and no problematic carbonaceous ore is present compared to what we mined this year. Production from Gold Bar South started last week.

Fox Complex, Timmins District

At the Fox Complex, operations are expected to deliver significantly better costs per ounce and margins compared to 2022. The mining of the Froome deposit is performing well. In fact, the mine is producing more ore than the mill can process. As a result, a large stockpile of ore-grade material has been produced that will be processed during 2023. This stockpile will allow for lower costs as the mining costs have already been expended.

Exploration at Froome has successfully extended the life of mine by another year, giving more time for the transition to mining from the Stock West deposit. Based on present data, mining at Froome will continue into 2025. An aggressive exploration program is planned for 2023, with a focus on definition of near-term resources at the Stock property.

San José Mine, Argentina

The San José mine is expected to deliver significantly better costs and margins compared to 2022, at current gold and silver prices. Exploration has defined extensions of several of its high-grade veins.

McEwen Copper’s Los Azules Deposit, Argentina

There are 6 drills currently on site and another 4 are due to arrive in January and February. The update of the Preliminary Economic Assessment (PEA) is progressing on schedule to be delivered in Q1, 2023.

For the SEC Form 10-Q Financial Statements and MD&A refer to:

www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0000314203

Technical Information

The technical content of this news release related to financial results, mining and development projects has been reviewed and approved by William (Bill) Shaver, P.Eng., COO of McEwen Mining and a Qualified Person as defined by SEC S-K 1300 and the Canadian Securities Administrators National Instrument 43-101 "Standards of Disclosure for Mineral Projects."

Reliability of Information Regarding San José

Minera Santa Cruz S.A., the owner of the San José Mine, is responsible for and has supplied to the Company all reported results from the San José Mine. McEwen Mining's joint venture partner, a subsidiary of Hochschild Mining plc, and its affiliates other than MSC do not accept responsibility for the use of project data or the adequacy or accuracy of this release.

CAUTIONARY NOTE REGARDING NON-GAAP MEASURES

In this release, we have provided information prepared or calculated according to United States Generally Accepted Accounting Principles ("U.S. GAAP"), as well as provided some non-U.S. GAAP ("non-GAAP") performance measures. Because the non-GAAP performance measures do not have any standardized meaning prescribed by U.S. GAAP, they may not be comparable to similar measures presented by other companies.

Cash Costs and All-in Sustaining Costs

Cash costs consist of mining, processing, on-site general and administrative costs, community and permitting costs related to current operations, royalty costs, refining and treatment charges (for both doré and concentrate products), sales costs, export taxes and operational stripping costs, and exclude depreciation and amortization. All-in sustaining costs consist of cash costs (as described above), plus accretion of retirement obligations and amortization of the asset retirement costs related to operating sites, sustaining exploration and development costs, sustaining capital expenditures, and sustaining lease payments. Both cash costs and all-in sustaining costs are divided by the gold equivalent ounces sold to determine cash costs and all-in sustaining costs on a per ounce basis. We use and report these measures to provide additional information regarding operational efficiencies on an individual mine basis, and believe that these measures provide investors and analysts with useful information about our underlying costs of operations. A reconciliation to production costs applicable to sales, the nearest U.S. GAAP measure is provided in McEwen Mining's Form 10-Q for the period ended September 30th, 2022.

CAUTION CONCERNING FORWARD-LOOKING STATEMENTS

This news release contains certain forward-looking statements and information, including "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. The forward-looking statements and information expressed, as at the date of this news release, McEwen Mining Inc.'s (the "Company") estimates, forecasts, projections, expectations or beliefs as to future events and results. Forward-looking statements and information are necessarily based upon a number of estimates and assumptions that, while considered reasonable by management, are inherently subject to significant business, economic and competitive uncertainties, risks and contingencies, and there can be no assurance that such statements and information will prove to be accurate. Therefore, actual results and future events could differ materially from those anticipated in such statements and information. Risks and uncertainties that could cause results or future events to differ materially from current expectations expressed or implied by the forward-looking statements and information include, but are not limited to, effects of the COVID-19 pandemic, fluctuations in the market price of precious metals, mining industry risks, political, economic, social and security risks associated with foreign operations, the ability of the corporation to receive or receive in a timely manner permits or other approvals required in connection with operations, risks associated with the construction of mining operations and commencement of production and the projected costs thereof, risks related to litigation, the state of the capital markets, environmental risks and hazards, uncertainty as to calculation of mineral resources and reserves, and other risks. Readers should not place undue reliance on forward-looking statements or information included herein, which speak only as of the date hereof. The Company undertakes no obligation to reissue or update forward-looking statements or information as a result of new information or events after the date hereof except as may be required by law. See McEwen Mining's Annual Report on Form 10-K/A for the fiscal year ended December 31, 2021 and other filings with the Securities and Exchange Commission, under the caption "Risk Factors", for additional information on risks, uncertainties and other factors relating to the forward-looking statements and information regarding the Company. All forward-looking statements and information made in this news release are qualified by this cautionary statement.

The NYSE and TSX have not reviewed and do not accept responsibility for the adequacy or accuracy of the contents of this news release, which has been prepared by management of McEwen Mining Inc.

ABOUT MCEWEN MINING

McEwen Mining is a gold and silver producer with operations in Nevada, Canada, Mexico and Argentina. In addition, it owns 68% of McEwen Copper which owns the large, advanced stage Los Azules copper project in Argentina. The Company’s goal is to improve the productivity and life of its assets with the objective of increasing its share price and providing a yield. Its Chairman and Chief Owner has personally provided the company with $220 million and takes an annual salary of $1.

|

|

|

|

Post by Entendance on Dec 29, 2022 12:33:47 GMT -5

|

|

|

|

Post by Entendance on Jan 13, 2023 7:32:09 GMT -5

|

|

|

|

Post by Entendance on Jan 17, 2023 8:51:35 GMT -5

|

|

|

|

Post by Entendance on Jan 26, 2023 3:25:25 GMT -5

Gold mining industry leader Rob McEwen shares expert insights on inflation, the BoJ's impact, the copper market and the future of McEwen Mining in this interview with @smallcapsteve

- The Deep Dive.

|

|

|

|

Post by Entendance on Jan 26, 2023 6:42:24 GMT -5

McEwen Copper: Los Azules – Robust Assay ResultsSignificant Drill Intercepts

237.2 m of 1.05% Cu including 108 m of 1.71% Cu (AZ22173)

373.9 m of 0.76% Cu including 96 m of 1.13% Cu (AZ22176)

TORONTO, January 26, 2023 -- McEwen Copper Inc., 68%-owned by McEwen Mining Inc. (NYSE: MUX) (TSX: MUX), today reports rich copper values over attractive widths resulting from infill drilling at its Los Azules project. Los Azules is a large porphyry copper-gold-silver deposit with considerable growth potential, where its ultimate depth and lateral extents remain to be determined.

Table 1 provides a summary of the assay results for eight recent drill holes for copper (Cu), gold (Au) and silver (Ag).

Highlights

Widespread mineralized magmatic hydrothermal breccias with intercepts such as 237.2 meters (m) of 1.05% Cu including 108 m of 1.71% Cu in hole AZ22173.

Continuity of an Enriched mineral zone up to 300 m, true thickness.

Northern exploration hole AZ22174 targeting a deep geophysical anomaly intersected multiple copper‑mineralized horizons including disseminated and veinlet-hosted primary copper mineralization and potassic alteration as deep as 1,100 m downhole, with assays pending.

More HERE

|

|

|

|

Post by Entendance on Jan 31, 2023 8:09:27 GMT -5

|

|

|

|

Post by Entendance on Feb 8, 2023 9:58:50 GMT -5

No Matter How You Turn It, The Global System is Already Doomed: Got Gold?

|

|

|

|

Post by Entendance on Feb 18, 2023 3:49:39 GMT -5

|

|

|

|

Post by Entendance on Feb 27, 2023 7:33:36 GMT -5

McEwen Copper Announces an Additional US$30 Million Investment by Nuton, a Rio Tinto Venture

February 27, 2023

TORONTO, Feb. 27, 2023 (GLOBE NEWSWIRE) -- McEwen Copper Inc., a subsidiary of McEwen Mining Inc. (NYSE: MUX) (TSX: MUX), is pleased to announce abinding agreement for an additional US$30 million investment by Nuton LLC, a Rio Tinto Venture, and existing McEwen Copper shareholder.

Nuton has agreed to invest US$30 million to acquire shares of McEwen Copper in a two-part transaction expected to close no later than March 10th, 2023 (the “Nuton Transaction”) consisting of: 1. Private placement of 350,000 McEwen Copper common shares, and 2. Purchase of 1,250,000 common shares owned by McEwen Mining in a secondary sale. Proceeds of the subscription and purchase are expected to be approximately US$6.5 million to McEwen Copper and US$23.5 million McEwen Mining, respectively. The proceeds of the private placement will be used to advance development of the Los Azules copper project in San Juan, Argentina, and for general corporate purposes.

After closing, Nuton will own 14.2% of McEwen Copper on a fully diluted basis, and McEwen Mining will own 51.9%. The transaction values McEwen Copper at approximately US$550 million.

McEwen Copper Chief Executive Rob McEwen said: “We are extremely pleased to have Nuton’s strong continued participation in McEwen Copper. Together we are exploring new technologies that save energy, water, time and capital in the pursuit of delivering green copper to Argentina and the world, a product that will contribute to the electrification of transportation and the protection of our atmosphere.”

In connection with the Transaction, McEwen Copper and certain of its affiliates entered into an Amended Collaboration Agreement (the "New Nuton Collaboration Agreement”) and a Copper Cathodes and Concentrates Purchase Rights Agreement (the “CCCPRA”), which are described below.

The NewNuton Collaboration Agreement provides for the following additional rights beyond those in the original Nuton Collaboration Agreement (see news release dated Aug 31, 2022):

Nuton will have the opportunity to provide local currency funding, in certain circumstances, for advancement of the Los Azules project;

Comprehensive scientific, technical and strategic planning information rights;

Extension of exclusivity over novel, trade secret or patented copper heap leach technologies until August 10, 2024;

Pre-emptive rights to maintain their ownership percentage in any follow-on equity offering; and

Agreement of McEwen Mining and Rob McEwen to not trigger Drag Along Rights in the event of a bid for McEwen Copper prior to the planned initial public offering (IPO).

The CCCPRA provides an option to Nuton that, if exercised to its maximum extent, would allow them to purchase a percentage of the copper products (cathodes, concentrates, etc.) produced from the Los Azules project equal to their equity ownership percentage in McEwen Copper at the time of exercise.

About Nuton

Nuton is an innovative new venture that aims to help grow Rio Tinto’s copper business. At the core of Nuton is a portfolio of proprietary copper leach-related technologies and capability – a product of almost 30 years of research and development. Nuton™ Technologies offer the potential to economically unlock copper sulphide resources, copper bearing waste and tailings, and achieve higher copper recoveries on oxide and transitional material, allowing for a significantly increased copper production. One of the key differentiators of Nuton is the potential to deliver leading environmental performance, including more efficient water usage, lower carbon emissions, and the ability to reclaim mine sites by reprocessing mine waste.

About Rio Tinto

Rio Tinto is the second largest mining and metals company in the world, operating in 35 countries, and producing the raw materials essential to human progress. It aims to help pioneer a more sustainable future, from partnering in the development of technology that can make the aluminum smelting process entirely free of direct greenhouse gas (GHG) emissions, to providing the world with the materials it needs – such as copper – to build a new low-carbon economy and products like electric vehicles, charging infrastructure and smartphones.

About McEwen Copper

McEwen Copper Inc. holds 100% interest in the Los Azules copper project in San Juan, Argentina and the Elder Creek project in Nevada, USA (subject to an earn-in by Rio Tinto).

Los Azules was ranked in the top 10 largest undeveloped copper deposits in the world by Mining Intelligence (2022). Its current copper resources are estimated at 10.2 billion pounds at a grade of 0.48% Cu (Indicated category) and an additional 19.3 billion pounds at a grade of 0.33% Cu (Inferred category).

After closing the Nuton Transaction, McEwen Copper will have 28,885,000 common shares outstanding on a fully diluted basis, and its shareholders are: McEwen Mining Inc. 51.9%, Stellantis 14.2%, Nuton 14.2%, Rob McEwen 13.8%, Victor Smorgon Group 3.5%, and other shareholders 2.4%.

About McEwen Mining

McEwen Mining is a gold and silver producer with operations in Nevada, Canada, Mexico and Argentina. In addition, it owns approximately 52% of McEwen Copper which owns the large, advanced stage Los Azules copper project in Argentina. The Company’s goal is to improve the productivity and life of its assets with the objective of increasing its share price and providing a yield. Its Chairman and Chief Owner has personally provided the company with $220 million and takes an annual salary of $1.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale would be unlawful.

McEwen Copper Closes ARS $30 Billion Investment by Stellantis

February 27, 2023

TORONTO, Feb. 27, 2023 (GLOBE NEWSWIRE) -- McEwen Copper Inc., a subsidiary of McEwen Mining Inc. (NYSE: MUX) (TSX: MUX), is pleased to announce closing of an ARS $30 billion investment by Stellantis, one of the world’s leading automakers and mobility providers with iconic brands including Abarth, Alfa Romeo, Chrysler, Citroën, Dodge, DS Automobiles, Fiat, Jeep®, Lancia, Maserati, Opel, Peugeot, RAM, Vauxhall, Free2Move and Leasys.

FCA Argentina S.A., a subsidiary of Stellantis N.V. (“Stellantis”), has invested ARS $30 billion in Argentina to acquire shares of McEwen Copper in a two-part transaction that closed on February 24th, 2023 (the “Transaction”) consisting of: 1. Private placement of 2,850,000 common shares, and 2. Purchase of 1,250,000 common shares indirectly owned by McEwen Mining in a secondary sale. The proceeds of the private placement will be used to advance development of the Los Azules copper project in San Juan, Argentina, and for general corporate purposes. After the closing of the Transaction, McEwen Mining will be separately compensated for the secondary sale by McEwen Copper in U.S. dollars.

Giving effect to the upcoming investment by Nuton LLC, also announced today, Stellantis owns 14.2% of McEwen Copper and McEwen Mining owns 51.9% on a fully diluted basis. The Transaction values McEwen Copper at approximately US$550 million.

Stellantis Chief Executive Officer Carlos Tavares said: “Stellantis intends to lead the industry with the commitment to be carbon net zero by 2038 – a goal that requires innovation and a complete redefinition of the entire business. We are taking important steps in Argentina and Brazil, with the aim of decarbonizing mobility and ensuring strategic supplies of clean energy and raw materials necessary for the success of the company’s global plans.”

McEwen Copper Chief Executive Officer Rob McEwen said: “We are delighted to have Stellantis as a partner in the future development of our Los Azules copper project. Together, we share a vision to build a mine for the future based on regenerative principles that can achieve net-zero carbon emissions by 2038. We are committed to delivering green copper to Argentina and the world, a product that will contribute to the electrification of transportation and the protection of our atmosphere.”

In connection with the Transaction, McEwen Copper and certain of its affiliates entered into an Investor Rights Agreement with Stellantis (the "Stellantis IRA”) and a Copper Cathodes and Concentrates Purchase Rights Agreement (the “CCCPRA”), which are described below.

The Stellantis IRA provides for the following principal terms:

Stellantis will have the right to nominate one director to the Board of McEwen Copper;

Comprehensive scientific, technical and strategic planning information rights;

Pre-emptive right to maintain their ownership percentage in any follow-on equity offering;

McEwen Copper commits to achieve net-zero carbon emissions from the Los Azules project by 2038; and

Other terms and conditions consistent with a transaction of this nature.

The CCCPRA provides an option to Stellantis and its affiliates that, if exercised to its maximum extent, would allow them to purchase a percentage of the copper cathodes or copper concentrates or both produced from the Los Azules project, in each case equal to their equity ownership percentage in McEwen Copper at the time of exercise.

About Stellantis

Stellantis N.V. (NYSE: STLA / Euronext Milan: STLAM / Euronext Paris: STLAP) is one of the world's leading automakers and a mobility provider. Its storied and iconic brands embody the passion of their visionary founders and today’s customers in their innovative products and services, including Abarth, Alfa Romeo, Chrysler, Citroën, Dodge, DS Automobiles, Fiat, Jeep®, Lancia, Maserati, Opel, Peugeot, RAM, Vauxhall, Free2Move and Leasys. Powered by their diversity, Stellantis leads the way the world moves – aspiring to become the greatest sustainable mobility tech company, not the biggest, while creating added value for all stakeholders as well as the communities in which it operates. For more information, visit www.stellantis.com.

About McEwen Copper

McEwen Copper Inc. holds 100% interest in the Los Azules copper project in San Juan, Argentina and the Elder Creek project in Nevada, USA.

Los Azules was ranked in the top 10 largest undeveloped copper deposits in the world by Mining Intelligence (2022). Its current copper resources are estimated at 10.2 billion pounds at a grade of 0.48% Cu (Indicated category) and an additional 19.3 billion pounds at a grade of 0.33% Cu (Inferred category).

After closing the pending investment by Nuton, also announced today, McEwen Copper will have 28,885,000 common shares outstanding, and its shareholders are: McEwen Mining Inc. 51.9%, Stellantis 14.2%, Nuton 14.2%, Rob McEwen 13.8%, Victor Smorgon Group 3.5%, and other shareholders 2.4%.

|

|

|

|

Post by Entendance on Mar 6, 2023 7:01:16 GMT -5

McEwen Copper: Los Azules – Initial Exploration and Solid Delineation Results

March 6, 2023

Exploration: 1,052 m of 0.29% Cu including 480 m of 0.42% Cu (AZ22174)

Delineation: 236 m of 1.39% Cu and 0.19 g/t Au including 42 m of 2.78% Cu (AZ23191)

“Strong team performance is accelerating our Los Azules program in 2023, ” commented Michael Meding, Vice President and General Manager of McEwen Copper. “Exciting results in hole AZ22174 highlight the potential of exploration to create additional value for McEwen Copper, and continuity of mineralization in the infill program is de-risking our mineral resource.”

TORONTO, March 06, 2023 (GLOBE NEWSWIRE) -- McEwen Copper Inc., 52%-owned by McEwen Mining Inc. (NYSE: MUX) (TSX: MUX), today reports new copper values over extensive widths resulting from infill and step-out exploration drilling at its Los Azules Project. Los Azules is a large porphyry copper-gold-silver deposit with considerable growth potential, where its ultimate depth and lateral extent remain to be determined.

The Los Azules project, located in the San Juan province, Argentina, has many attributes comparable to world-class copper-gold deposits in South America. Table 1 provides a summary of the assay results for the two drill holes for copper (Cu), gold (Au) and silver (Ag).

Highlights

Exploration: 1,052 meters (m) of 0.29% Cu including 480.0 m grading 0.42% Cu(AZ22174), which is coincident with a prominent deep geophysical anomaly and showcases the potential to meaningfully expand Los Azules through exploration.

Delineation: 236 m of 1.39% Cu and 0.19 g/t Au, including 42 m of 2.78% Cu (AZ22191) demonstrates strong internal continuity of the high grade mineralization from the current infill program and further de-risks our geological model.

Drilling

Over 13,500 m of drilling were completed between January and May in 2022. Activity at Los Azules restarted in October, focused on completing a drill program covering over 25,000 m in 75 new holes, designed to:

Increase infill drilling to upgrade the Cu, Au and Ag resource classification to measured and indicated, leading to improved geological and economic estimates in a planned 2024 Feasibility Study (FS).

Provide metallurgical, hydrological and geotechnical data to facilitate mine design.

Demonstrate extensions of Los Azules to the North, South and at depth.

From October to the 3rd week of February, a further 16,900 m in 66 holes have been completed for the current program, making this the most extensive annual drill campaign in the history of the project. A more comprehensive update of results from the current campaign will be released soon.

Exploration Drilling

Figure 1 - AZ22174 Assay Results versus 2017 PEA 3D Pit Shell

Our initial exploration hole of the program, AZ22174, was drilled to a depth of 1,128 m with copper mineralization observed along its entire length including a 1,052 m intercept averaging 0.29% Cu. Mineralization along the drillhole is more prevalent below 500 m, where more than 66% of the overall contained copper (480 m grading 0.42% Cu) resides. The hole was planned based on the center of a geophysical anomaly sitting at about 800 m depth, near the termination of a historic hole. The results from hole AZ22174 reinforce our belief that the deposit continues to be open at depth and to the North and represents a sizeable opportunity. The sub-interval of 26 m grading 1.46% Cu includes early mineral porphyry and quartz veinlets that also typify the core of Los Azules.

Delineation Drilling

Figure 2 - Section 37 - AZ23191 shown with mineral zones and 30-year PEA pit (looking north)

Delineation drilling continues at Los Azules with a focus on upgrading to Measured mineral resources the Enriched zone as shown on Section 37 in Figure 2. Hole AZ23191 lies 50 m north of Section 36 (See Figure 2 in the January 26th, 2023 press release) and graded 1.39% Cu over 236 m including 2.78% Cu over 42 m. There remain assays pending along the final 31 metres of the hole. The interpretation of the enriched mineralization was drafted prior to the results from AZ23191 being available, but overall, the shape still conforms well. What is most striking is the grade of the intercept versus nearby hole AZ22180 as shown by the histogram lengths and colours. This reflects the structurally controlled nature of mineralization, particularly in the core of the deposit where grades are highest.

Technical Information

The technical content of this press release has been reviewed and approved by Stephen McGibbon, P. Geo., McEwen Mining's Senior Consulting Geologist, and a qualified person as defined by NI 43-101.

All samples were collected in accordance with generally accepted industry standards. Drill core samples usually taken at 2 m intervals were split and submitted to the Alex Stewart International laboratory located in the Province of Mendoza, Argentina, for the following assays: gold determination using fire fusion assay and an atomic absorption spectroscopy finish (Au4-30); a 39 multi-element suite using ICP-OES analysis (ICP-AR 39); copper content determination using a sequential copper analysis (Cu-Sequential). An additional 19 element analysis (ICP-ORE) was performed for samples with high sulfide content.

The company conducts a Quality Assurance/Quality Control program in accordance with NI 43-101 and industry best practices using a combination of standards and blanks on approximately one out of every 25 samples. Results are monitored as final certificates are received and any re-assay requests are sent back immediately. Pulp and preparation sample analyses are also performed as part of the QAQC process. Approximately 5% of the sample pulps are sent to a secondary laboratory for control purposes. In addition, the laboratory performs its own internal QAQC checks, with results made available on certificates for Company review.

Table 2 - Hole Locations and Lengths for AZ22174 and AZ23191

Link to location, lengths and geochemical results of the different drill holes, for January to February 2023 at Los Azules:

www.mcewenmining.com/files/doc_news/archive/2023/2023_02_Los_Azules/2023_02_Los_Azules_Assays_Composites_CollarLocations.xls

ABOUT MCEWEN MINING

McEwen Mining is a gold and silver producer with operations in Nevada, Canada, Mexico and Argentina. In addition, it owns approximately 52% of McEwen Copper which owns the large, advanced stage Los Azules copper project in Argentina. The Company’s goal is to improve the productivity and life of its assets with the objective of increasing its share price and providing a yield. Its Chairman and Chief Owner has personally provided the company with $220 million and takes an annual salary of $1.

|

|

|

|

Post by Entendance on Mar 8, 2023 12:31:14 GMT -5

McEWEN MINING Q4 & 2022 RESULTS CONFERENCE CALL

TORONTO, March 8, 2023 - McEwen Mining Inc. (NYSE: MUX) (TSX: MUX) invites you to join our conference call following the release of our Q4 and year-end 2022 financials results on Tuesday, March 14th, 2023 at 11:00 AM EST, where management will discuss our financial results and project developments and follow with a question-and-answer session. Questions can be asked directly by participants over the phone during the webcast.

An archived replay of the webcast will be available approximately 4 hours following the conclusion of the live event. Access the replay on the Company’s media page at www.mcewenmining.com/media/overview/default.aspx

|

|

|

|

Post by Entendance on Mar 11, 2023 8:14:08 GMT -5

|

|

|

|

Post by Entendance on Mar 14, 2023 5:38:52 GMT -5

Stage Is Now Set for Increased Production and Lower Costs in 2023

Welcoming Nuton & Stellantis as Shareholders of McEwen Copper

TORONTO, March 14, 2023 ( GLOBE NEWSWIRE) -- McEwen Mining Inc. (NYSE: MUX) (TSX: MUX) today reported fourth quarter and full year results for the period ended December 31, 2022.

“2022 was an important transition year for McEwen Mining. Our Fox operation in Timmins showed the largest improvement from 2021, with a 22% increase in gold production, 8% lower cash costs per ounce and steady all-in sustaining costs per ounce. Our operation in Nevada has now transitioned production to our Gold Bar South pit, a new mining contractor has been instated, and production is increasing,” commented Rob McEwen, Chairman and Chief Owner. “Our McEwen Copper subsidiary reached several milestones during 2022 and early 2023, including, building a seasoned Argentine management team, improving critical access to Los Azules with the completion of a second route to site, advancing technical studies, cementing our commitments to government and local stakeholders, and welcoming two strategic investors: Nuton (a Rio Tinto Venture and part of the world’s 2nd largest mining company) and Stellantis, the world’s 4th largest automobile manufacturer and mobility provider.”

Looking Ahead

For 2023, our production guidance is 150,000 to 170,000 GEOs (see Table 1).

Subsequent to the year end, a subsidiary of Stellantis N.V. invested ARS$ 30 billion, and Nuton LLC, a Rio Tinto Venture, agreed to increase its investment by $30 million, to acquire shares of McEwen Copper. Subsequent to these transactions, each of Stellantis and Nuton own 14.2% of McEwen Copper, and McEwen Mining owns 52%. As a result, the implied valuation of McEwen Copper is now approximately $550 million on a 100% basis.

Looking at 2022

Our McEwen Copper subsidiary completed three tranches of financing during 2021-2022, raising a total of $81.9 million for Los Azules exploration and pre-development activities.

In 2022, production was 133,300 gold equivalent ounces (GEOs)(1), slightly below our revised guidance range of 134,600 to 141,600 GEOs due to lower than planned production at the Fox Complex during the final days of the year (see Table 2).

Our 100%-owned mines (Fox Complex and Gold Bar) generated a cash gross profit of $19.2 million(2) in 2022 and a gross loss of $0.5 million. Cash gross profit is calculated by adding back non-cash depletion and depreciation to gross profit (loss).

We incurred advanced project expenditures of $41.3 million at Los Azules net of foreign exchange gains, or, on a gross basis, a $61.1 million contribution to net loss. Under U.S. GAAP, we continue to expense our Los Azules project costs.

Our consolidated net loss in 2022 of $81.1 million, or $1.71 per share, relates primarily to investment of $81.7 million in advanced projects and exploration (including 100% of Los Azules expenses) offset by a gain of $19.8 million on foreign exchange transactions, general and administrative costs of $11.9 million, tax expenses of $5.8 million, and a gross loss of $0.5 million from our operations (see Table 4).

Cash and liquid assets(2) at December 31, 2022 were $46.2 million.

Production costs per ounce for 2022 were $1,276 for cash costs(2) per GEO sold from our 100%-owned mines, representing a decrease of 12% compared to 2021, and $1,688 for all-in sustaining costs (AISC)(2) per GEO sold, representing an increase of 3% compared to 2021 (see Table 3).

We continued to invest aggressively in exploration, completing 181,100 feet (55,200 meters) of drilling at the Fox Complex, 16,900 feet (5,200 meters) of drilling at the Gold Bar Mine, and 73,500 feet (22,400 meters) at the Los Azules project.

A webcast will be held on Tuesday, March 14th at 11:00 am EDT. Please see the details further below.

Notes:

'Gold Equivalent Ounces' are calculated based on a gold to silver price ratio of 77:1 for Q4 2021, 72:1 for 2021, 85:1 for Q4 2022 and 84:1 for 2022. 2023 production guidance is calculated based on 85:1 gold to silver price ratio.

Cash gross profit, cash costs per ounce, all-in sustaining costs (AISC) per ounce, and liquid assets are non-GAAP financial performance measures with no standardized definition under U.S. GAAP. For definition of the non-GAAP measures see "Non-GAAP- Financial Measures" section in this press release; for the reconciliation of the non-GAAP measures to the closest U.S. GAAP measures, see the Management Discussion and Analysis for the year ended December 31, 2022 filed on Edgar and SEDAR.

McEwen Mining shares issued and outstanding at Dec 31, 2021 were 459,187,391 and at Dec 31, 2022 was 47,427,584, following a reverse share split effective July 28, 2022.

Represents the portion attributable to us from our 49% interest in the San José Mine.

Operations Update

Fox Complex, Canada (100% Interest)

Production from the Black Fox Mine stopped in Q4, 2021 and started at the Froome Mine. As a result, production in 2022 increased 22% year over year, costs were slightly lower, and the safety record improved.

In addition, Froome’s production exceeded mill capacity; therefore 120,000 tonnes of mineralized material was stockpiled at the end of 2022, ready for processing in 2023.

The Froome Mine produced 9,870 GEOs in Q4 2022, bringing the full year 2022 production to 36,650 GEOs. This represents increases of 4% and 22% respectively from the comparable periods in 2021.

Cash cost per GEO sold in 2022, was $1,020 and AISC per GEO was $1,465 compared to costs in 2021 of $1,108 and $1,461, respectively.

In recent years, we have invested significant capital in exploration. The principal focus has been on discovering resources adjacent to our existing operations in order to increase gold production, extend the mine life and shorten the payback period of the PEA. During 2022, we incurred $11.4 million in exploration activities at Fox. The exploration budget for 2023 at the complex is $15.0 million.

The Preliminary Economic Assessment (PEA) for the Fox Complex published on January 26, 2022 details our expansion plans for the Fox Complex, to occur after we complete mining at the Froome Mine. As a result of our investment in exploration, we have found sufficient new gold resources that allow for extending the mine life, planning a doubling of gold production and significantly reducing costs per ounce. The economics are attractive, providing for a mine life of an additional 9-years where the average annual gold production is 80,800 oz with average cash costs and AISC per ounce of $769 and $1,246, respectively.

Gold Bar Mine, USA (100% Interest)

A record safety milestone was achieved in 2022, operating for over 1,000 days without a lost-time incident.

Production at Gold Bar was adversely impacted by encountering carbonaceous ore that could not be processed and the delay in mining as we transitioned to a new mining contractor. As a result, the mine production was 39% lower year-over-year with 7,940 GEOs in Q4, and 26,620 in 2022.

Cash cost and AISC per GEO sold were $1,622 and $1,989 for the year 2022. The year-over-year 4% decrease in cash cost per GEO was primarily a result of reduced contract mining costs. AISC per GEO for the year 2022 was 14% higher due to expenditures on reclamation, exploration, plant and equipment, and securing environmental credits for the Gold Bar South (GBS) project.

In 2023, production has shifted to GBS, which does not contain carbonaceous ore, has a lower waste stripping ratio and a higher average gold grade compared to previous mined areas at Gold Bar. The change of the mining contractor in Q4 2022 is expected to drive improved production efficiencies in 2023.

In 2022, $4.8 million was invested in exploration, including drilling 16,900 feet (5,200 meters) of core and reverse circulation drilling focused on targets around the mine, such as near-mine extensions at Cabin North, Pick and potential extensions at the Atlas Pit. The exploration budget for 2023 is $5.5 million.

San José Mine, Argentina (49% Interest)

Our share of the San José mine production was 69,130 GEO in 2022, 10% lower than in 2021. The decrease is attributable to lower processed tonnes due to the impact of COVID-19 and mill availability issues in Q1 2022. Together with a decrease in gold and silver prices in 2022 compared to 2021, the dividend received was only $0.3 million in 2022, compared to $9.8 million received during 2021.

Q4 2022 cash costs and AISC per GEO of $1,321 and $1,701 respectively. These costs were still high but substantially better than in Q4 2021, decreasing by 23% and 17% respectively compared to Q4 2021. Production costs in 2021 were adversely impacted by COVID-19.

2022 cash costs and AISC per GEO were $1,306 and $1,714, an increase of 3% and 7% respectively compared to 2021, as a result of lower GEOs sold partially offset by lower production costs.

McEwen Copper (52% Interest)

On August 31, 2022, McEwen Copper completed a US$81.9 million offering including a $25 million investment by Nuton, a Rio Tinto Venture.

On October 24, 2022, McEwen Copper signed an option agreement with Kennecott Exploration Company (“Kennecott”), a subsidiary of Rio Tinto. By spending $18 million over up to seven years, Kennecott can earn a 60% interest in the Elder Creek property and form a 60:40 joint venture with McEwen Copper.

Subsequent to December 31, 2022, we announced the closing of an ARS $30.0 billion investment by FCA Argentina S.A., a subsidiary of Stellantis N.V. (“Stellantis”) to acquire shares of McEwen Copper and of a second investment of $30 million by Nuton that increases their investment to $55 million. The Stellantis transaction consisted of a private placement of 2,850,000 common shares, and the purchase of 1,250,000 common shares indirectly owned by McEwen Mining in a secondary sale. The Nuton transaction consisted of a private placement of 350,000 common shares, and the purchase of 1,250,000 common shares indirectly owned by McEwen Mining in a secondary sale. The proceeds of the private placement will be used to advance the development of the Los Azules copper project in San Juan, Argentina, and for general corporate purposes. Subsequent to the transactions, Stellantis and Nuton each own 14.2% of McEwen Copper, while McEwen Mining’s ownership is reduced to approximately 52%. McEwen Mining plans to use the proceeds from the secondary sales to reduce its debt by 38% and increase its treasury to fund production growth.

About Stellantis

Stellantis N.V. is one of the world's leading automakers and a mobility provider. Its storied and iconic brands embody the passion of their visionary founders and today’s customers in their innovative products and services, including Abarth, Alfa Romeo, Chrysler, Citroën, Dodge, DS Automobiles, Fiat, Jeep®, Lancia, Maserati, Opel, Peugeot, RAM, Vauxhall, Free2Move and Leasys.

About Nuton

Nuton is an innovative new venture that aims to help grow Rio Tinto’s copper business. At the core of Nuton is a portfolio of proprietary copper leach-related technologies and capability – a product of almost 30 years of research and development. Nuton™ Technologies offer the potential to economically unlock copper sulphide resources, copper bearing waste and tailings, and achieve higher copper recoveries on oxide and transitional material, allowing for a significantly increased copper production.

Exploration Drilling

Drilling has focused on increasing drill hole density to upgrade the copper mineral resource classification to measured and indicated and to better define the payback pit design; providing metallurgical, hydrological, and geotechnical data to support mine design; and testing for potential extensions of the copper resource to the north, south and at depth. Drilling started in January and went to May, when it stopped for the winter in the southern hemisphere, then restarted in October and is currently ongoing. There were 6 drill rigs on site in 2022, and 5 more were added in early 2023.

From 2022 to date we have drilled over 105,000 feet (32,000 meters) in 98 drill holes. Recent results include 236 m of 1.39% Cu and 0.19 g/t Au including 42 m of 2.78% Cu (hole AZ23191) for delineation and 1,052 m of 0.29% Cu including 480 m of 0.42% Cu (hole AZ22174) for exploration.

A total of $61.2 million was spent in 2022 at the Los Azules project to advance drilling, engineering and project feasibility work. The first step is updating the PEA that is expected to be published in Q2 2023.

Road Construction

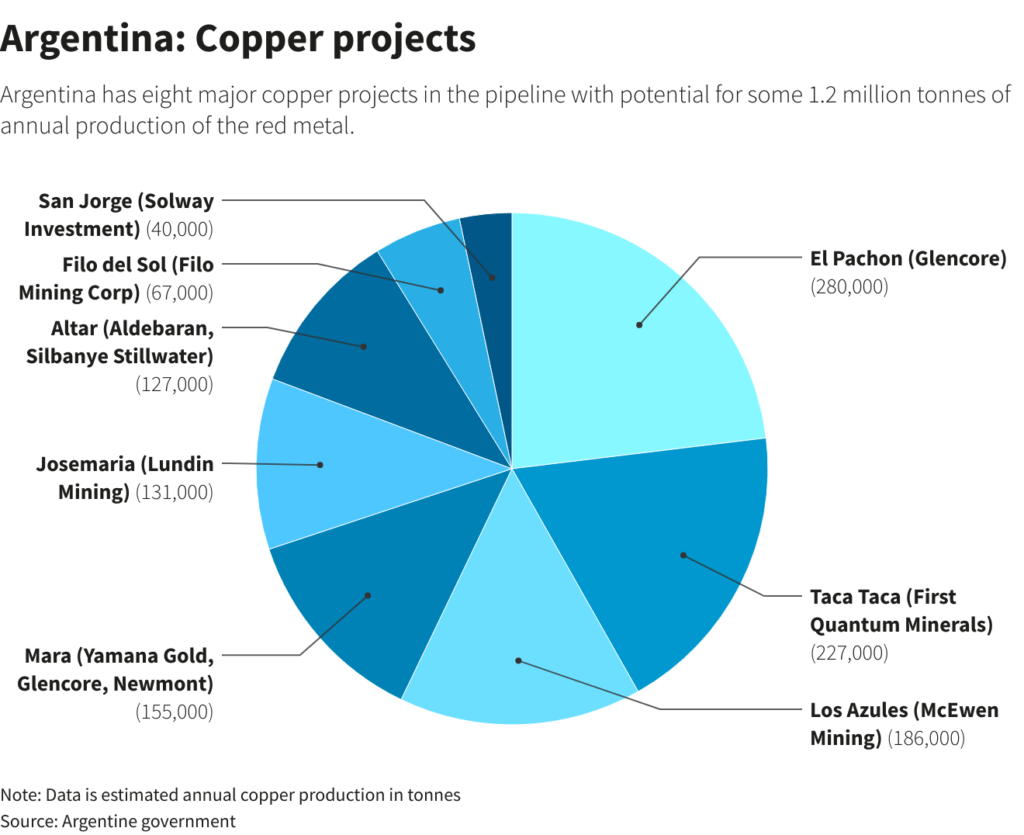

In 2022, a major advance was made that will accelerate the development of Los Azules with the completion of a new low altitude access road (maximum 11,155 feet ASL), which we share in part with other mining projects, including El Pachón and Altar. The importance of having a second road into the site at 2,000 feet lower altitude means we now have almost year-round access.

Technical Studies

The updated PEA will include all available information on drilling, assay and metallurgical testing obtained during the 2017, 2018 and 2022 exploration seasons. During the quarter we continued work on trade-off studies (related to power supply and the potential for renewables, mining methods and processing options), an updated glacier study, and initial geotechnical field of work for the design of heap leaching, tailings and waste storage facilities. Hydro-geological holes have commenced and complement the works on assessing historical information and re-establishing existing water monitoring locations.

Currently, we are developing a scenario for Los Azules as an open pit mine that initially processes leachable copper content in a heap leach, with a solvent extraction and electrowinning facility to produce LME Grade A copper cathodes. This scenario would greatly reduce capital expenditures as compared to 2017’s PEA using concentrator technology, in addition it would be more environmentally sensitive due to its much lower water consumption and carbon footprint. The project design makes use of renewable energy, reducing overall complexity and improves its financial attractiveness.

Metallurgical studies continue, including with Nuton’s technology for heap leaching of copper ore. Initial results show promising recoveries and reduced acid consumption for the scenario described above.

The Exploitation Environmental Impact Report preparation has been awarded to Knight Piesold, with the drafting of the report underway and on track for submitting to permitting authorities in April 2023.

El Gallo Mine and Fenix Project (100% Interest)

Activities at the El Gallo mine in 2022 were limited to residual leaching as part of closure and reclamation plans. The residual leaching activities of the El Gallo mine, ceased in July 2022.

The capital required to build the Fenix Project was reduced materially in September 2022 with the purchase of a second-hand gold processing plant and associated equipment for $2.8 million. The purchase includes substantially all the major components required to start the Fenix Project. This equipment was estimated at $25.3 million in our Fenix Project feasibility study, published in February 2021.

Multiple strategic alternatives continue to be evaluated for the project including financing options, lower capital costs, potential base metal evaluation.

Conference Call and Webcast Management will discuss our Q4 and Year-End 2022 financial results and project developments and follow with a question and answer session. Questions can be asked directly by participants over the phone during the webcast.

Tuesday

Mar 14 th 2023

11:00 AM EDT

Toll Free (US & Canada): (888) 330-2398

Outside US & Canada: (240) 789-2709

Conference ID Number: 67121

Event Registration Link: conferencingportals.com/event/ZSafhHZi

Webcast Link: events.q4inc.com/attendee/387697089

The webcast will be archived on McEwen Mining's website at www.mcewenmining.com/media following the call.

Technical Information

The technical content of this news release related to financial results, mining and development projects has been reviewed and approved by William (Bill) Shaver, P.Eng., COO of McEwen Mining and a Qualified Person as defined by SEC S-K 1300 and the Canadian Securities Administrators National Instrument 43-101 "Standards of Disclosure for Mineral Projects."

Reliability of Information Regarding San José

Minera Santa Cruz S.A., the owner of the San José Mine, is responsible for and has supplied to the Company all reported results from the San José Mine. McEwen Mining’s joint venture partner, a subsidiary of Hochschild Mining plc, and its affiliates other than MSC do not accept responsibility for the use of project data or the adequacy or accuracy of this release.

CAUTIONARY NOTE REGARDING NON-GAAP MEASURES

In this release, we have provided information prepared or calculated according to United States Generally Accepted Accounting Principles (“U.S. GAAP”), as well as provided some non-U.S. GAAP ("non-GAAP") performance measures. Because the non-GAAP performance measures do not have any standardized meaning prescribed by U.S. GAAP, they may not be comparable to similar measures presented by other companies.

Cash Costs and All-in Sustaining Costs

Cash costs consist of mining, processing, on-site general and administrative costs, community and permitting costs related to current operations, royalty costs, refining and treatment charges (for both doré and concentrate products), sales costs, export taxes and operational stripping costs, and exclude depreciation and amortization. All-in sustaining costs consist of cash costs (as described above), plus accretion of retirement obligations and amortization of the asset retirement costs related to operating sites, sustaining exploration and development costs, sustaining capital expenditures, and sustaining lease payments. Both cash costs and all-in sustaining costs are divided by the gold equivalent ounces sold to determine cash costs and all-in sustaining costs on a per ounce basis. We use and report these measures to provide additional information regarding operational efficiencies on an individual mine basis, and believe that these measures provide investors and analysts with useful information about our underlying costs of operations. A reconciliation to production costs applicable to sales, the nearest U.S. GAAP measure is provided in McEwen Mining's Annual Report on Form 10-K for the year ended December 31, 2022.

Cash Gross Profit

Cash gross profit is a non-GAAP financial measure and does not have any standardized meaning. We use cash gross profit to evaluate our operating performance and ability to generate cash flow; we disclose cash gross profit as we believe this measure provides valuable assistance to investors and analysts in evaluating our ability to finance our ongoing business and capital activities. The most directly comparable measure prepared in accordance with GAAP is gross profit. Cash gross profit is calculated by adding depletion and depreciation to gross profit. A reconciliation to gross profit, the nearest U.S. GAAP measure is provided in McEwen Mining's Annual Report on Form 10-K for the year ended December 31, 2022.

Liquid Assets

The term liquid assets used in this report is a non-GAAP financial measure. We report this measure to better understand our liquidity in each reporting period. Liquid assets is calculated as the sum of the Balance Sheet line items of cash and cash equivalents, restricted cash and investments, plus ounces of doré held in precious metals inventories valued at the London PM Fix spot price at the corresponding period. A reconciliation to the nearest U.S. GAAP measure is provided in McEwen Mining's Annual Report on Form 10-K for the year ended December 31, 2022.

CAUTION CONCERNING FORWARD-LOOKING STATEMENTS

This news release contains certain forward-looking statements and information, including "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. The forward-looking statements and information expressed, as at the date of this news release, McEwen Mining Inc.'s (the "Company") estimates, forecasts, projections, expectations or beliefs as to future events and results. Forward-looking statements and information are necessarily based upon a number of estimates and assumptions that, while considered reasonable by management, are inherently subject to significant business, economic and competitive uncertainties, risks and contingencies, and there can be no assurance that such statements and information will prove to be accurate. Therefore, actual results and future events could differ materially from those anticipated in such statements and information. Risks and uncertainties that could cause results or future events to differ materially from current expectations expressed or implied by the forward-looking statements and information include, but are not limited to, effects of the COVID-19 pandemic, fluctuations in the market price of precious metals, mining industry risks, political, economic, social and security risks associated with foreign operations, the ability of the corporation to receive or receive in a timely manner permits or other approvals required in connection with operations, risks associated with the construction of mining operations and commencement of production and the projected costs thereof, risks related to litigation, the state of the capital markets, environmental risks and hazards, uncertainty as to calculation of mineral resources and reserves, and other risks. Readers should not place undue reliance on forward-looking statements or information included herein, which speak only as of the date hereof. The Company undertakes no obligation to reissue or update forward-looking statements or information as a result of new information or events after the date hereof except as may be required by law. See McEwen Mining's Annual Report on Form 10-K for the fiscal year ended December 31, 2022 and other filings with the Securities and Exchange Commission, under the caption "Risk Factors", for additional information on risks, uncertainties and other factors relating to the forward-looking statements and information regarding the Company. All forward-looking statements and information made in this news release are qualified by this cautionary statement.

The NYSE and TSX have not reviewed and do not accept responsibility for the adequacy or accuracy of the contents of this news release, which has been prepared by management of McEwen Mining Inc.

ABOUT MCEWEN MINING

McEwen Mining is a gold and silver producer with operations in Nevada, Canada, Mexico and Argentina. In addition, it owns approximately 52% of McEwen Copper which owns the large, advanced stage Los Azules copper project in Argentina. The Company’s goal is to improve the productivity and life of its assets with the objective of increasing its share price and providing a yield. Rob McEwen, Chairman and Chief Owner, has personally provided the company with $220 million and takes an annual salary of $1.

|

|

|

|

Post by Entendance on Mar 15, 2023 6:15:21 GMT -5

McEwen Mining Inc. (NYSE:MUX) Q4 2022 Earnings Conference Call March 14, 2023 Company Participants

Rob McEwen - Chairman and Chief Owner

Perry Ing - Chief Financial Officer

William Shaver - Chief Operating Officer

Michael Meding - Vice President and General Manager of McEwen Copper

Stefan Spears - Vice President, Corporate Development

Conference Call Participants

Jake Sekelsky - Alliance Global Partners

Heiko Ihle - H.C. Wainwright

Mike Kozak - Cantor Fitzgerald

John Tumazos - John Tumazos Very Independent Research

Rob McEwen

Good morning, ladies and gentlemen.

Today, I'll start with a discussion about gold and then our share price performance and follow up with factors driving our future.

With all the uncertainties in the world, many people are asking why the price of gold hasn't climbed much higher. I believe that most investors feel that we have entered into a new era where very low interest rates and massive monetary stimulation are here to stay. And the gold's reputation as a store of wealth is no longer relevant or needed in a world of awash with easy money.

However, as we all know, the unexpected happens quickly. Rising interest rates and an unexpected bank failure are vivid reminders, gold still has a role to play in your portfolio. I suspect more investors will start adding gold and gold shares to their portfolio and they will follow the lead of a select number of central banks who became large gold buyers in 2022. In fact, their purchases were the largest purchases made in the past 50 years by central bankers. Perhaps they too are concerned about holding too much of their reserves in fiat currencies.

So, during 2022, the price of gold outperformed not only gold equities, but also the Dow Jones. Gold increased 1% year-over-year, and at the yesterday's close, it was up 6% since December 31, 2021. During that same period, the senior and junior gold equities as measured by the ETFs, the GDX and the GDXJ registered losses of 10.5% and 15%, respectively in 2022, while the Dow was down 3.7%. But if we look back another year to December 31, 2021, and come forward to yesterday's close, the GDX was down 9.1%, the GDXJ down 16.2%, and the Dow was down 12.4%.

We weren't as lucky in 2022. Our share price was hammered. It was down a painful 36%. Fortunately, it has recovered much of this loss and has increased an impressive 136% since the end of last year, December 31, 2022. And if we look back to December 31, '21, our share price is only down 13.1%, which is less than the GDX decline of 16.2%, and very close to the decline of the Dow Jones Industrial Average of 12.4%.

So, looking at our stock chart, from a technical perspective, it looks very promising. With our share price having broken out on the upside through its 50, 100, 300 day moving averages. Driving this price improvement is our demonstration of improving operational performance, good exploration results, production growth, and lower cost per ounce, along with the growing recognition that McEwen Copper's Los Azules project is a large copper resource with large strategic shareholders, Rio Tinto, the world's second largest mining company, and Stellantis, the world's fourth largest automobile manufacturer and mobility provider.

For 2023, we are looking at a production increase of 12.5% to 27.5% over what we did in 2022, and our costs are expected to decline by about 5%. In 2022, our Fox Complex and Gold Bar mines generated operating profits, but the accelerated activities at our subsidiary McEwen Copper and its Los Azules project and our heavy investment in exploration contributed significantly to our large reported loss.

I will now ask Perry to provide details on how we performed financially in 2022 and more importantly what we see going forward in 2023. He will be followed by our Director and Interim Chief Operating Officer, Bill Shaver, who will comment on our success in stabilizing our mine operations and where we see growth in those operations. Bill will be followed by Michael Meding, our Vice President and General Manager of McEwen Copper, who will outline our progress at Los Azules and the financings we recently completed and the strategic shareholders we have.

Perry, off to you.

Perry Ing

Thank you, Rob. Good morning, everyone.

As Rob mentioned, I'll provide an overview of our fourth quarter and full year results for 2022, and then I'll discuss the impact of the recent Stellantis and Nuton, Rio Tinto transactions for our balance sheet.

These transactions are, obviously, transformative for the company. We'll deleverage our balance sheet in a rising interest rate environment and allow the company to advance its Fenix project in Mexico, as well as continue to explore aggressively in Ontario and Nevada without issuing additional equity, especially at these current gold prices.

For the Los Azules project, these transactions will bring two things. First, it brings on a key partner in the project in Stellantis and strengthens the relationship with another in Rio Tinto. It also provides significant funding to Argentina to continue our aggressive exploration efforts and provide McEwen Copper further flexibility in the timing of a potential IPO.

First off though, I'll start with a review of McEwen Mining's consolidated results for the prior year. It is important to note that we report McEwen Copper as a consolidated entity and reflect 100% of its expenditures on Los Azules on our income statement. As a U.S.-listed company reporting under U.S. accounting standards, we do not have the option of capitalizing the exploration and development costs at the project or any of our other projects for that matter until we have a completed feasibility study and permits for development, unlike many of our Canadian listed peers that often capitalize these costs at a much earlier stage.

In terms of looking at our headline figures, we reported a loss for the quarter and year of $37.4 million and $81.1 million, respectively. This translates into $0.79 per share and $1.71 per share, respectively. As ** for the loss for the year is due to the expensing of costs at Los Azules net of foreign exchange gains realized. A further 25% roughly is due to exploration and development costs at our 100% owned properties. The remainder of the loss figures per share reflect our G&A costs and certain one-time tax charges. I also note that the per share amounts reflect the 10 for 1 share consolidations completed in July of last year, which re-established the company's compliance with NYSE share price listing requirements.

Looking at our 100% owned mines, we generated a cash gross profit of $7.9 million for the quarter and $19.2 million for the full year, respectively. On a gross profit basis, these operations were essentially breakeven, a significant improvement over 2021 performance.

Looking at gold equivalent production, production for the fourth quarter of 37,300 gold equivalent ounces was down just under 10% compared to the fourth quarter of 2021, driven by a decrease of approximately 2,000 ounces at Gold Bar as they transition into the new Gold Bar South pit during the quarter.

Full year production of 133,300 gold equivalent ounces was down approximately 14% year-over-year. Again, the decrease was primarily driven at Gold Bar due to carbonaceous ore issues experienced earlier in the year as well as the transition into Gold Bar South in the fourth quarter of the year.

At the San Jose mine, production was down approximately 10% year-over-year due to issues with COVID and at the mill in the first quarter of 2022. Bill Shaver will cover off these line operations in further detail.

So, the revenue and cost standpoint realized gold prices were roughly unchanged at the $1,800 level for both 2022 and the prior year. Gold prices were slightly lower in the fourth quarter of 2022, but appears to have rebounded well into the first quarter of this year so far.

Looking at costs, we noted significant improvement in cash costs at our 100% owned operations at $1,276 per ounce, which have decreased steadily since 2020, but lower cost reported at both the Fox Complex and Gold Bar compared to the prior year. All-in sustaining costs were largely consistent with the prior year and reflect the cost of bringing Gold Bar South into production at -- in Nevada. At the San Jose mine, both cash costs and all-in sustaining costs increased incrementally over the prior year, reflecting lower production due to the issues I noted previously.

Finally, looking at our treasury, at the end of the year, our cash and equivalent balance stood at $44 million compared to $60 million at the beginning of the year.

Now, I'll turn the attention to the recent transactions with Stellantis and Nuton, Rio Tinto and how it impacts our balance sheet and working capital on a go-forward basis. These transactions all closed within the past three weeks. The transaction included an offering of primary shares directly from the McEwen Copper and a component of secondary shares, which are the shares of McEwen Copper owned by McEwen Mining. The details are summarized in our news release, so I'll just try to encapsulate it at a high level.

Essentially, McEwen Mining, if we look at it as a standalone company, it receives $48 million. McEwen Copper receives approximately ARS30 billion. The price point of these transactions -- the price point at which these transactions are valued from McEwen Copper standpoint has nearly doubled the initial $10 per share amount when we did the investments in June and August of last year. Following these transactions, McEwen Mining's ownership of McEwen Copper reduces from approximately 68% at the end of 2022 to 51.9% today.

In terms of the proceeds to McEwen Mining, we intend to use $25 million of the proceeds to retire the secured debt to Sprott Lending, which will reduce our total debt from $65 million to $40 million, saving the company significant interest costs going forward.

With our enhanced treasury, we believe we now have the funds on hand to build Phase 1 of the Fenix project in Mexico and bring that operation into production within the next year without raising additional capital.

As far as McEwen Copper's treasury, the ARS30 billion is a significant amount. At official exchange rate, this is equivalent to over $150 million. Using less official measures, such as a Blue Chip Swap rate, this is approximately equal to about $80 million. With this round of financing completed, McEwen Copper is well positioned to execute its drilling and development program for the remainder of the year and into 2024, which Michael will outline.

So, based on these transactions, the urgency to complete an IPO in the first half of 2023 has been eliminated.

So, with that, I'll turn the presentation over to Bill Shaver.

William Shaver

Thank you very much, Perry. Good morning, shareholders.

This morning, I'd like to leave you with three messages with regard to our operations. We have improved mining operations at the Fox Complex and are improving milling operations, which will result in higher output and lower cash costs in 2023. At Gold Bar, we have successfully transitioned to a new contractor and we have moved the operations to Gold Bar South pit, which will produce most of the ore in 2023. And based on the first two months of production, we are fully transitioned on both fronts, that being the new contractor and full operations. Cash costs for these operations will be approximately $1,100 per ounce in 2023, which is a significant improvement of approximately 15% from 2022. And lastly, at the Fenix project, as Perry has mentioned, we have moved the plant -- that we purchased last year to the plant site and are at -- in the working stages of planning production in early 2024.

The last quarter of 2022 was challenging, but hard work by all our mining operations helped us overcome these hurdles, making Q4 a reasonable quarter. We are also making progress in stabilizing and improving operations, so we can obtain predictable outcomes for gold production and costs in 2023 and into the future. And so far, this year, we are on track.

On the safety front, in 2022, we had two low severity lost-time incidents in January and March at our El Gallo operations. And for the rest of the year, we were lost-time accident free. At the Fox Complex, we have operated for a full year in 2022 with no lost-time injuries. And at Gold Bar, we recently passed three years without a lost-time injury.

On the environmental front, we -- there were no environmental events recorded in 2022.

Now, I'll turn it over to each of the operations. At the Fox Complex, we had a very challenging year with our mill, which continued to have significant availability issues, which hampered our throughput. This resulted in us missing our gold production last year. At the same time, the mine had an excellent year, which resulted in a stockpile build up to 120,000 tonnes by year-end. This represents a value of approximately $15 million after milling and recovery.

On a positive note, we have now undertaken crushing of the ore at the mine prior to it being shipped to the mill. This lowers the amount of work that the mill needs to do in processing the ore. This decision was followed -- was following a test program to prove this concept last year. We have been able to get our production tonnage through the mill successfully in Q1 of 2023 and are looking forward to improving the throughput when we get the contract crushing plant that we have planned for the remainder of the year at Froome into place. This plant will be commissioned in early April, which will allow us to reduce the size of stockpile we have at the Fox mill, transforming it into gold and therefore cash. We anticipate we will meet our budgeted cash call for the year of $922 per ounce.

At the Gold Bar mine in Nevada, 2022 was also challenging with our issues of preg-robbing ore and our parting of ways with our mining contractor at the start of Q4. Notwithstanding these issues, we transitioned the mine plan successfully to main production in Q4, and we are happy to tell you we have successfully transitioned to a new contractor who is now in full production. We also completed the move to the Gold Bar South pit and are now in full production in this pit. Gold production from Gold Bar has been on budget for the first two months of this year and we're looking forward to a good year from operations.

At the Fenix project in Mexico, we have been able to develop an approach to get the Fenix project in production in a timely manner and at a significantly lower capital cost. We will reprocess the heap leach pad, which has a grade of 0.6 grams per tonne. To accomplish this, we have acquired a used 7,000 tonne per day gold processing plant, which operated recently at a local mining operation. We have moved 80% of this plant to our site. And for Fenix, we will initially assemble only the grinding circuit, the cyclones and the leaching portion of the plant and use the present El Gallo gold recovery circuit. This will reduce the CapEx to approximately $12 million with the potential to increase the throughput as we move into production and prove that this plant will give the required outputs. There are a few minor changes in our permits that are required, but we hope to have this plant operating late this year or early in 2024.

With that, I thank you very much. And now I'll turn it over to Michael for an update on our world-class Los Azules project.

Michael Meding

Thank you so much, Bill.

I will quickly highlight our financing and strategic importance of our new shareholders, then report on our drilling, exploration and study work, and finally mention what we did last year and in 2023 concerning our enhanced organizational and ESG competence in Argentina.

McEwen Copper completed $81.9 million offering, including a $25 million investment by Nuton, a Rio Tinto Venture, on August 31, 2022, followed on October 24, by an option agreement with Kennecott Exploration, another subsidiary of Rio Tinto, for potential earn in of 60% for Elder Creek by investing $18 million over seven years. Subsequent to December 31, 2022, we announced the closing of an ARS30 billion investment by Fiat Chrysler Argentina, a subsidiary of Stellantis, to acquire shares of McEwen Copper and of a second investment of $30 million by Nuton that increased the investment to $55 million.

Now, Nuton is an innovative new venture with the portfolio of proprietary copper heap leach related technologies and capabilities at the core, a product of almost 30 years of research and development. Those have the potential to economically unlock copper sulfide resources and achieve higher copper recoveries on oxide and transitional material. Rio Tinto is the world's second biggest mining company, bringing significant financial and technical resources to McEwen Copper and the Los Azules project.

Stellantis, on the other hand, is one of the world's leading automakers. It produces iconic brands such as Alfa Romeo, Chrysler, Citroen, Dodge, Fiat, Jeep, Lancia, Maserati, Opel, Peugeot, Ram, Vauxhall and others. And in Argentina, Stellantis produces about 160,000 cars yearly, has about 3,000 employees and is present with manufacturing in Buenos Aires and in Cordoba, Argentina. Partnering with Stellantis is an expression of a paradigm shift for downstream customers of copper. Companies realize that copper is a mineral critical to the green energy and mobility transition. And to my knowledge, it's the first time an automotive company has invested in a copper company.

Subsequent to those transactions, Stellantis and Nuton each own 14.2% of McEwen Copper. McEwen Mining's ownership is now approximately 52%.

Now I'm going to talk about drilling, exploration, site and study work. A total of $41.3 million was incurred in 2022 at the Los Azules project to advance drilling, engineering and project feasibility work. Drilling has focused on increasing drill hole density to upgrade the copper mineral resource classification to measured and indicated and to define the payback pit design better, to provide metallurgical, hydrological and geotechnical data to support mine design and [step-out] (ph) exploration testing for potential extensions of the copper resource to the north, south and the depth of this already vast deposit, which Mining Intelligence ranked in 2022 as the ninth largest undeveloped copper project by copper resource size.

In 2022, drilling started in January and went to May when it stopped for the winter in the southern hemisphere, then restarted in October and is currently ongoing. Since October 2022, there were six drill rigs on site and five more were added in early 2023. From 2022 to date, we have drilled over 105,000 feet, approximately 32,000 meters, in 98 drill holes to increase geological confidence and we see that drill results are generally consistent with our model.

Beyond our robust delineation results, published in January and March this year, we recently published our northern step-out exploration results with 1,052 meters of 0.29% copper including an interval of 480 meters of 0.42% copper, which demonstrates the potential of the deposits to the north. The updated PEA will include all available information on drilling, assay and metallurgical testing obtained until early 2023 and is now slated for publishing during Q2 this year.