|

|

Post by Entendance on May 23, 2023 15:48:35 GMT -5

McEwen Mining Reduces Debt by 39%

May 23, 2023

TORONTO, May 23, 2023 -- McEwen Mining Inc. (NYSE: MUX) (TSX: MUX) (“McEwen Mining” or the “Company”) today reported that it has repaid $25 million of its senior secured debt payable to Sprott Resource Lending (“Sprott”) and Sprott is no longer a lender.

Prior to the repayment, the Company had $50 million in senior secured debt and a $15 million unsecured promissory note, for a total debt of $65 million. Concurrent with the repayment to Sprott, the senior secured debt was amended and restated in the amount of $40 million bearing monthly interest at 9.75% per annum, and the promissory note was extinguished. The Company’s sole lender is now an entity owned by our Chairman and Chief Owner Rob McEwen.

As a result of the debt reduction, McEwen Mining’s annual borrowing costs will decrease by approximately $2.2 million or 36%.

Certain provisions of the amended and restated credit agreement have been modified, with the approval of the independent directors, specifically:

The schedule of principal repayments will now begin with amortization of $1 million per month starting on January 31st, 2025, with the remaining principal due at maturity on August 31st, 2026;

The loan can be repaid at any time, in any amount, without penalty;

The security package has been amended to exclude certain non-core assets; and

Certain other covenants, restrictions and events of default have been deleted.

The reduction of debt was funded through the secondary sale of McEwen Copper shares to FCA Argentina S.A. (Stellantis) and Nuton LLC, which closed in February and March 2023, and raised $47.5 million in gross proceeds to McEwen Mining.

|

|

|

|

Post by Entendance on Aug 10, 2023 5:25:21 GMT -5

August 10, 2023

TORONTO, Aug. 10, 2023 -- McEwen Mining Inc. (NYSE: MUX) (TSX: MUX) reported its second quarter (Q2) and half year (H1) results for the period ended June 30th, 2023.

“The year started with operational challenges at both Gold Bar and San Jos é . San Jos é appears to have turned the corner and we are confident that the plan in place for Gold Bar will do the same. Fox Complex has delivered another solid quarter and we expect even better results in the second half of the year. We thank our operating teams for their hard work. The story at Los Azules keeps getting better and better! With a strong financing, an updated Preliminary Economic Assessment (PEA) showing robust economics, unparalleled partners in Rio Tinto (through Nuton) and Stellantis, and potentially game changing copper leaching technology, we could see Los Azules provide a model for how the mine of the future should look,” said Rob McEwen, Chairman and Chief Owner.

Second Quarter Highlights and Building Our Future:

Fox Complex: Record daily mill throughput of 1,250 tonnes per day, generating $6 million in cash gross profit in Q2. Sustained higher throughput and improved grade expected to result in stronger production and margins in H2.

San José: Production increased 54% with cash costs/oz declining 24% compared to Q1, as the revised mine plan continues to be executed.

Gold Bar: Higher mining rates and gold grades, together with faster recovery and lower strip ratio from the Pick deposit setting stage for improved production and margins in H2/23 and beyond. Higher costs/oz during Q2 included the additional costs associated with the heap leach pad expansion, which is expected to be completed in Q3.

Fenix Project: We continue to advance towards a formal construction decision. During the quarter, we initiated a sonic drilling campaign, advanced permitting applications and engaged a project manager.

McEwen Copper: PEA for the Los Azules copper project issued in June 2023 with NPV8% of $2.7 Billion and payback period of 3.2 years, assuming a copper price of $3.75/lb. Based on the financing closed in Q1/23, our 52% ownership of McEwen Copper has now an implied value of $285 million, which is equal to 67% of our current market capitalization.

Early retirement of $25 million or 39% of our outstanding debt in Q2; reduction of debt service of $2.2 million annually.

We continued our safety track record of no lost time incidents at our 100% owned operating mines during Q2.

Exploration update across the portfolio to be delivered later in Q3.

Mr. McEwen continued, “At McEwen Mining, quarterly production from our mines delivered a marked improvement in terms of ounces produced over Q1. At the Fox Complex its AISC was 8% lower than the comparable period in 2022. Gold Bar continued with high costs per ounce, however we expect to see much better performance in H2 as a result of a lower strip ratio and increased mined ore grades. At San José production got back on track in Q2. We anticipate all our mines will deliver stronger results in H2 and finish the year in line with our production guidance. We are advancing two important development projects, at the Fox Complex in Canada and at the Fenix project in Mexico, both designed to extend the mine lives by 9 years.

Our biggest single asset with the greatest near-term potential to increase our share value is our 52% owned subsidiary McEwen Copper. Given my long association with gold, I view non-gold deposits in terms of their gold equivalent value. McEwen Copper’s most advanced property is its large Los Azules copper project. On June 20 th we published an updated PEA for Los Azules. Using the numbers of this PEA and a copper gold ratio of 500 to 1 (500 lbs of copper currently have the value of 1 oz of gold), Los Azules has a resource base equivalent to a 75 million ounce gold deposit with annual gold equivalent production of 800,000 oz in the 1 st 5 years, 644,000 oz over the following 22 years, low production costs of $535/oz cash costs and $820/oz AISC, generating the payback of its $2.5 Billion initial capex in 3.2 years (based on a $3.75/lb copper price). Notably, these impressive results are achieved from extracting the economically mineable portion representing just about one third of the current resource estimate, as determined by the present PEA.

Moreover, by implementing a sustainable approach, this potentially multi-generational asset could become a model for mines of the future. Compared to conventional copper mines, Los Azules is designed with a much lighter impact on the environment, emitting 1/3 the carbon initially to zero by 2038, utilizing ¼ the water, 100% powered by renewable energy sources, and producing sustainable copper cathode.

Investing with us in the future of Los Azules are two global companies, Rio Tinto and Stellantis (through their respective subsidiaries), the world’s 2 nd largest mining company and the world’s 4 th largest automaker, each owning 14.2% of McEwen Copper.

The updated Los Azules PEA surpasses the 2017 assessment in key areas, including: 1. Superior financial metrics, 2. Larger copper resource estimate, 3. Significantly lower water consumption and greenhouse-gas emission, 4. Substantial decrease in electricity consumption and 5. A design optimized for permitting and development in the next 5 years. We are now focused on our next milestone, which is to deliver a final Feasibility Study by late 2024 - early 2025.

We have invested heavily in exploration and the results have been most encouraging, particularly at Los Azules, where the resource base increased by 27%, and at the Fox Complex, where the results allow us to see the potential for significant increase in mine life. These large investments in exploration are treated on our income statement as expenses and are the primary reason for our consolidated loss this quarter. We will continue to report losses in McEwen Copper until Los Azules has reached a stage where costs can be capitalized under US accounting rules.”

Financial Results

Notice to reader: Under US GAAP, McEwen Mining consolidates 100% of the accounts of its fully owned and majority owned subsidiaries in its reported financial results, including McEwen Copper. Entities over which we exert significant influence but do not control (such as Minera Santa Cruz S.A. [MSC], the operator of the San José mine) are presented as an equity investment on our balance sheet.

Our cash gross profit(1) was $4.8 million and our gross loss in Q2 was $3.5 million, compared to a gross profit of $4.2 million and cash gross profit of $7.7 million in Q2 2022. Cash gross profit or loss excludes the non-cash depreciation included in the gross profit or loss. During Q2, gross loss was impacted by lower grades and longer recovery times at our Gold Bar mine operations, which are expected to reverse in H2, based on anticipated 25% higher mined grades, faster recoveries and a 33% lower strip ratio. This should result in higher production and improved margin expansion. Our gross loss was also impacted by an increase in non-cash depreciation rates at Gold Bar resulting from a reduction in our mineral reserve base at the end of Q4 2022. Our Fox Complex operations generated a $6.0 million cash gross profit in Q2, and we expect to build on this momentum during the second half of the year, as we mine higher grade material and maintain our higher mill throughput.

Adjusted net loss(1) was $13.0 million, or $0.27 per share in Q2, compared to $1.9 million, or $0.04 per share in Q2 2022. Adjusted net income or loss is a new non-GAAP financial measure intended to provide readers with a metric to evaluate our 100% owned precious metal business, therefore excluding McEwen Copper, with its copper assets (52% owned), and MSC, operator of the San José mine (49% owned). Together with our gross loss described above, we also invested $7.1 million in exploration and advanced project expenses, primarily at our Fox Complex operations, where we continue to develop our Stock West project. Exploration expenditures at Fox Complex are expected to decrease in the second half of the year as we complete our flow-through expenditure commitments.

We reported a consolidated net loss of $21.6 million, or $0.46 per share in Q2, compared to $12.5 million, or $0.26 per share in Q2 2022. This was driven by an investment of $28.5 million in our Los Azules project to complete our 2022-2023 drilling program and publish our updated PEA, which we expensed under US GAAP. As we progress towards feasibility at Los Azules, we expect to continue to report losses until we meet the US GAAP requirements for capitalization, which typically require a feasibility study establishing a mineral reserve estimate and permitting. As a result of our $130 million investment in exploration since 2021, we have increased the implied valuation of McEwen Copper on a 100% basis from $257 million to over $550 million.

Liquidity and Capital Resources

Consolidated cash and equivalents increased to $84.6 million(2) at the end of Q2 from $39.8 million at the end of 2022. Additionally, investments totalled $29.2 million, primarily in equity securities held in Argentina, to mitigate the impact of high inflation and devaluation. Consolidated working capital was $92.0 million at June 30, 2023.

During Q2, we decreased our total debt by $25 million to $40 million and entered into the Third Amended and Restated Credit Agreement effective May 23, 2023. As a result, our interest expenses associated with long-term debt were decreased by $2.2 million per year.

In addition, the Company’s 52% ownership of McEwen Copper has an implied market value of $285 million, based on the last financing round with Rio Tinto (through Nuton LLC) and Stellantis (one of the world’s leading automakers and owner of 14 iconic brands including such names as Alfa Romeo, Chrysler, Dodge, Fiat, Jeep and Maserati).

The Company also maintains a portfolio of royalties including a 1.25% net smelter royalty at both our Los Azules and Elder Creek properties, together with three other royalties on properties in Nevada and in Santa Cruz, Argentina.

Gold & Silver Production

Production from our three operating mines was 35,625 gold equivalent ounces (GEOs) (3) in Q2 and 66,100 GEOs in H1, compared to 36,218 GEOs in Q2 2022 and 61,200 GEOs in H1 2022. Our consolidated production guidance remains 150,000-170,000 GEOs for 2023. Details on how we plan to achieve guidance are outlined in the section below.

Individual Mine Performance (See Table 1):

Fox Complex: Timmins, Canada

Fox performed well in the quarter and achieved its budgeted production. Mill throughput in Q2 was 31% higher than in Q4 2022, reaching a record 1,250 tonnes per day, an important achievement by our team in Canada, as we aim to consistently maintain higher throughput. Cash costs were slightly higher than our annual guidance due to moving to contractor crushing in early 2023, however we expect AISC to remain in-line with guidance as a result of reduced capital expenditure requirements. Gold grades are expected to be approximately 10-15% higher in H2, which will also bring down our per ounce costs for the second half of the year.

Gold Bar: Nevada, USA

Despite the historic difficulties at Gold Bar, we are confident in our team’s plan at the mine to ramp up gold production during H2, which will also result in lower costs and increased profitability. This will be achieved by mining 25% higher grades by prioritizing material from the Pick open pit, which also allows for a 33% lower strip ratio and faster leaching recoveries. Based on these factors we expect Gold Bar to meet production guidance of 42,000 to 48,000 GEOs for the full year. With the anticipated improvements to gold production, we also expect to lower cash costs/oz and AISC/oz in H2, to meet our annual guidance figures.

San José: Santa Cruz, Argentina

San José had a difficult start to 2023 as seen in our Q1 results. The team at San José has been quick to respond by implementing operational changes that resulted in production increasing 54% and cash costs/oz decreasing by 24% in Q2 as compared to Q1. This was achieved through mining and processing more tonnes containing higher average gold and silver grades. As a result, San José’s revised production targets were met in the quarter, and production guidance of 66,000 to 74,000 GEOs(4) for the full year is reiterated. Although San José’s cash costs and AISC per ounce sold for the full year are forecast to remain 10-20% above guidance due to the difficulties encountered in Q1 and the additional investments required to de-risk mine production, the team deserves congratulations for all their efforts in identifying the operational issues and putting in corrective measures.

Exploration

Exploration results from the Fox Complex were published in a separate press release on May 8th and an additional update is planned in early September.

Gold Bar exploration activities are focused on discovering near mine resources. Two drills will be active on the property in H2, with one drill outside the mining area testing the Wall Fault, which is believed to be a primary feeder fault for the mineralization at Gold Bar.

McEwen Copper

Infill and exploration results from Los Azules were published on April 5th, May 5th, July 12th and Aug 1st. The drilling campaign at Los Azules ended mid-June and is expected to resume in October, after the South American winter.

Additional assay results from the recently completed drilling campaign will be published over the next months. All drilling information received after the December 31, 2022 cut-off date for the PEA will be incorporated in our upcoming feasibility study.

We own a 52% interest in McEwen Copper Inc., which holds a 100% interest in the Los Azules copper project in San Juan, Argentina, and the Elder Creek exploration project in Nevada, USA. The last financings completed by McEwen Copper with Stellantis and Rio Tinto (Nuton) gave the company an implied market value of $550 million. This translates to $285 million for McEwen Mining shareholders’ 52% ownership. This value is equal to approximately 67% of the current fully-diluted market capitalization of McEwen Mining.

During Q2, McEwen Copper spent $28.5 million to advance a major drilling campaign involving up to 15 rigs, ongoing road maintenance and improvements, hyperspectral scanning of the entire drill core data, technical studies necessary for the updated PEA, environmental baseline work, project optimization and trade-off studies (including renewable power supplies and mining methods), and metallurgical test work. The Environmental Impact Report for Exploitation was submitted during the quarter to the Argentinian authorities for review, and the team is now working on advancing Los Azules to the Feasibility Study level.

At the Elder Creek project operated by Kennecott Exploration Company, a subsidiary of Rio Tinto, six exploration drill holes have been completed with results pending. Kennecott has the option to earn a 60% interest in Elder Creek by investing $18 million over a maximum of seven years.

PEA Highlights

Please refer to our June 20, 2023 news release for summary results of the Los Azules PEA update. The technical report has been filed on SEDAR and on the Company’s website: www.mcewenmining.com/investor-relations/reports-and-filings/default.aspx

Base Case Highlights (Nameplate capacity of 175 kt per year of copper cathode production, $3.75/lb Cu price)

Updated independent mineral resource estimate, which increased to 10.9 billion (B) lbs. Cu Indicated (0.40% grade) and 26.7 B lbs. Cu Inferred (0.31% grade)

Average annual Cu cathode production of 401 million lbs. (182,100 tonnes) during the first 5 years of operation, and 322 million lbs. (145,850 tonnes) over the 27-year life of the mine (LOM)

Total Cu recoverable to cathode of 8.68 billion lbs. (3.94 million tonnes), based on the LOM extraction of mineralized material containing approximately 11.90 billion lbs. of total Cu (5.40 million tonnes), and average copper recovery of 72.8%

After-tax net present value (NPV8%) of $2.659 billion, internal rate of return (IRR) of 21.2%, and a payback period of 3.2 years

Initial capital expenditure of $2.462 billion, and a project capital intensity of $7.66 per lb. Cu ($16,880 per tonne Cu)(5)

Average C1(5) cash costs of $1.07 per lb. Cu and all-in sustaining costs(5) of $1.64per lb. Cu (AISC Margin of 56%)(5)

Average EBITDA(6) per year of $1.101 billion (Years 1-5) and $692 million (Years 6-27)

Estimated carbon intensity of 826 kg CO2 equivalentper tonne of Cu (CO2-e/t Cu)(7) for Scope 1&2 GHG Emissions, well below the industry average of 1,980kg CO2-e/t Cu(8). McEwen Copper’s goal at Los Azules is to be carbon neutral by 2038, a target achievable through the use of emerging technologies and offsets

Estimated site-wide water consumption of 137 liters per second (L/s) from Years 1 to 10, increasing to 163 L/s from Years 11 to 27. This compares to approximately 600 L/s(9) for a conventional mill producing copper concentrate

Upside case with the addition of Nuton™ technologies(10) increases NPV8% to $3.701 billion, IRR to 23.9%, and mine life to 39 years, and reduces payback to 2.7 years.

Management Conference Call

Management will discuss our Q2 financial results and project developments and follow with a question-and-answer session. Questions can be asked directly by participants over the phone during the webcast.

Thursday

Aug 10 th , 2023

at 11:00 AM EDT

Toll Free (US & Canada): (888) 210-3454

Outside US & Canada: (646) 960-0130

Conference ID Number: 3232920

Event Registration Link: events.q4inc.com/attendee/300718616

An archived replay of the webcast will be available approximately 2 hours following the conclusion of the live event. Access the replay on the Company’s media page at www.mcewenmining.com/media.

|

|

|

|

Post by Entendance on Aug 11, 2023 1:48:20 GMT -5

McEwen Mining Inc. Q2 2023 Earnings Conference Call August 10, 2023 11:00 AM ET

Company Participants

Rob McEwen - Chairman and Chief Owner

William Shaver - COO

Michael Meding - VP and General Manager, McEwen Copper

Perry Ing - CFO

Conference Call Participants

Jake Selesky - Alliance Global

Heiko Ihle - H.C. Wainwright

Bill Powers

Rob McEwen

Good morning and welcome, ladies and gentlemen.

Today, I will be discussing the highlights of our operating and financial results in Q2 and the first half of this year as well as our expectations for the balance of the year. Our press release of this morning discusses these matters in greater detail, and members of senior management are on the line to answer your questions.

As many of you are aware, our gold and silver assets had a weak start for the year. While activities at McEwan Copper's Los Azules project we're running at a rapid pace. I'm pleased to say that our mines delivered better results in Q2 than Q1 and the outlook for the second half of the year is significantly better.

But I'd like to share with you the highlights of the first quarter - this quarter that's passed second quarter. One, the Fox Complex generated gross profits of $6 million and is expected to deliver on our guidance. The San Jose performance was much stronger in Q2 than in Q1, and it too is expected to deliver on its production guidance, but costs will be 10% to 20% higher on a cost per ounce basis. At Gold Bar, the outlook, again, is looking significantly better as a result, and we are increasing the mining rate we'll be mining with a lower strip ratio and processing a higher grade of ore. McEwen Copper released in June, its updated preliminary economic assessment. It displays a project with robust economics, a long life, low production costs and based on an environmentally sensitive approach to mining.

Safety at all of our sites was the way we like it. No lost times at Fox and Gold Bar. We improved our balance sheet by reducing our debt by 39% to $40 million. And financially, we consolidate the financials of our 52% owned subsidiary, McEwen Copper. And as I said, we've invested heavily in exploration and other work in order to complete the updated PEA.

So our quarter end, our consolidated liquid assets were $85 million, with an additional $29 million in investments. Our working capital was $92 million, and our consolidated net loss in the quarter was $22 million and in the first half, $65 million, again, reflecting the very heavy investment in moving the Los Azules project forward. And we've increased the value of Los Azules significantly during this period, it now has a value of about $555 million implied based on the last financing we did. Our investment in exploration at Fox has given us a resource base and confidence to see a mine life being extended by 9 years. And in Mexico, construction of the Phoenix project is expected to start later this year and provide a 9 year mine life.

In terms of our share performance since the beginning of the year to present day, we're up just under 18% in U.S. dollars. And that compares against the GDX, which is down 1.8%, the GDXJ, down 5.2%. Gold's up 4%, the Dow's up 6%. And the NASDAQ is the early one of those that has outperformed. It's up 32%, largely driven appears by generative AI development. And I have to say that the mining world will be embracing generative AI as we go forward like many other industries.

I'd now like to open the conference call for questions.

Jake Selesky, Alliance Global So just starting off at the Fox Complex. You mentioned grades should tick a bit higher in the second half of this year. Are you able to quantify that at all? I'm just trying to get a handle on how that might impact costs for Q3 and Q4 heading into next year.

Rob McEwen

Bill, would you like to answer that?

William Shaver

Yes, sure. Yes, Jake, we expect that the grade in the second half of the year is going to be closer to 4 grams per tonne. The second quarter, the grade was closer to 3 grams per tonne. And that goes back to our original budget and mine plan for this year. So it - the original plan had us with a lower grade in the first half of the year and a little bit higher grade. And we're now into the higher grade to the stock we're in, right this week is the grade is more like 5 grams per tonne. So we'll see the grade increase, and so that will move our costs down by a significant amount. And so we'll finish the year following our guidance almost exactly right.

The upside, I would say, is the fact that the mill has run significantly better in the second quarter. We had some more or less record months of around 1,250 tonnes per day for the quarter. May and June was actually closer to 1,320 tonnes per day. So if there's upside, it's in the fact that we're - we've been able to increase the tonnage through the mill. And if the grade stays where we think it will, and there's no reason to think it won't be predictable, then we'll have a slightly better second half.

Jake Sekelsky

Okay. That's helpful. And good to see there. And just switching over to Los Azules. Any color on the work that's left for the feasibility study, the timing of the report and maybe the specifics that are milestones that need to be hit just to switch over from expensing investments there to capitalizing them.

Rob McEwen Michael?

Michael Meding

Sure. So we slate the delivery of the feasibility study to the end of 2024, beginning of 2025. We have confirmed the main consultants that are working with us to the delivery, mainly the most important one I would say, is [Semel engineering] and [indiscernible]. Semel has helped us in the PEA and as well as [indiscernible] was also delivering our environmental impact assessment report. So that is well under the way. We need to drill about 45,000 meters. We have secured already 16 drills to be able to do that. We own 4 drill rigs and bought another two and import permits. We're looking to get another two to ensure that we can get through the drilling program to be able to get all the information required to feasibility level of detail.

So I think we are very optimistic going forward. Now with regards to the capitalization criteria, especially the environmental permanent issues plus the feasibility study. Perry, I'm not sure whether you would like to give additional insights?

Perry Ing

Yes. Now, I think that's an accurate statement, Michael. And just for context, I mean, that's a result of us obviously being a U.S. GAAP reporter.

And assuming if we IPO McEwen copper at some point, we could have a situation where if McEwen to report under IFRS, it would actually capitalize those costs. The criteria under IFRS are a lot looser, whereas McEwen Mining would still have to continue expensing those costs. So that's just a unique feature of the differences in accounting policies.

Jake Sekelsky

Got it. Okay. That makes sense. That's all on my end. Thanks again.

Rob McEwen

Thanks Jake.

Heiko Ihle, H.C. Wainwright Would you be able to provide me with the approximation of your labor cost increases from the past, call it, 6 or 12 months by asset. I assume there are some pretty meaningful differences in what you've seen between Timmins or I guess, rather Canada, Nevada and Argentina, please?

Rob McEwen

William, would you like to venture into that?

William Shaver

Yes. I guess that's a question I'm not totally prepared to answer. But I guess our cost in Canada in terms of labor cost is around 7% or 8%. And I would say our material costs are probably somewhere in the range of 10%. And I think we anticipated that we would see a higher fuel price than we're actually seeing. So I think there's some positives there. And I think there's some other, I guess, consumables that we're seeing, which seem to have smoothed out to some extent and not being steel in terms of grinding balls and also cyanide. So I think - if I had to say what the cost increase has been on a year-over-year basis, I'd say it's around 10% or maybe a little bit higher than that. But I think if you use 10%, you wouldn't be wrong.

Heiko Ihle

Moving on to drilling at Gold Bar a little bit. As per your release, your expiration for the second half of the year is on the nearby resources there. You're operating two drills there in the second half, if more is correct. And you were talking about the cedar halt. Now what exactly do you think that will do to the ore body? Are your geologists telling you that's more or less the same type of ore. So metallurgy would be the same? Or is this just creating else? What exactly is the goal, I guess, is what I'm saying. Thank you.

William Shaver

Yes. So the goal of that drilling program is kind of two or threefold. First, we're defining the parameters for ore that we will mine in the relatively near future, meaning next year and the year after. The second part is to find more ore that will - that we'll mine into the future. And it's to -- in both cases, we're trying to get a very good understanding of what the strip ratios are going to be and also where there might be carbon associated with some of these resources so that we're able to mine that in a proper fashion to make sure we can segregate the carbonaceous ore from the ore that doesn't have carbon

There's also of - there's also some deeper drilling that we're doing there where I would say we're kind of exploring for perhaps some elephants that are similar to some properties that are just north of us, say, about 20 kilometers away. So - but the focus of the drilling program is to make sure we know what we're doing over the next 18 to 24 months.

Heiko Ihle

I appreciate it. we'll get back in queue. Thank you, all.

Rob McEwen

Thanks Heiko.

Bill Powers Good morning. Thanks for setting this up today I just had a couple of questions. I guess, starting in Canada, you - during the AGM, you mentioned that you had a capacity of 1,400 tons per day. And I guess my question would be, is the stockpile has that been able to be reduced at all at the higher rate of mill running? Or is that just - or is that still there? And I guess, are you planning to move towards 1,400 tonnes per day in Q3 and the rest of the year?

William Shaver

Yes. So thanks for the question. The mill tonnage in May and June has increased up to about 1,320 tonnes a day. But meanwhile, the stockpile is still very close to 100,000 tonnes. So although we're increasing the tonnes through the mill, the mine is operating very well. The whole operation is kind of in a sweet spot in terms of the mining operation. So we're keeping up with the milling process even though we've increased it by something more than 15% over last year. So we would like to get the stockpile lower to transfer it over into actual cash. But we also want to keep the mine running at that sweet spot so that we get the optimum mining cost. So yes, I would say we're doing better on the milling where the mine is fine, keeping up and we're continuing to try to improve the throughput through the mill.

Bill Powers Okay. Thank you on that. As far as Nevada goes, I know there was some exploration around the Atlas pit that was done last year and seemed to have some promising results. Have those - has that been followed up on? And I guess, is that a target for later this year? Or is that something - or if you focus elsewhere you're drilling near term?

William Shaver

We're actually focusing on other portions of our property. The drill holes at the Atlas pit I guess, we found a small amount of ore in one pit wall that at some point, we may go and take, but we're talking about something in the order of 10,000. It hasn't turned out as positive as we hope.

Bill Powers And thank you for the update. And I guess my last question would be - I was a little late to the call this morning, but the - if you could - maybe you've gone over this, so this question was asked earlier. But the expansion of the ramp, I know you - are you still planning to put out a study for that? Or I guess, a larger study for that? Or is that something that is going to be moving forward in the balance of this year.

William Shaver

So yes, and we're talking now about the ramp at the stock mine?

Bill Powers Yes.

William Shaver

Yes, that ramp will be moving ahead. We're doing the final bit of delineation drilling with regard to that part of the project. And we are putting together, I guess, what we're calling an economic analysis, which we'll have early in - late in the third quarter or early in the fourth quarter. But we don't plan to do a revised PEA or pre-feasibility study on that. We're going to basically produce an economic analysis to make the final decision to go ahead. But at this point, we're basically working at full speed to move that project ahead.

Rob McEwen

Assuming the metal prices stay where they are and we're delivering on guidance, we don't anticipate having to come to the capital markets to fund any of our development projects. We're in a good position from our liquidity, and we're quite excited about the projects we're advancing. We - there will be exploration news coming out throughout this latter part of the summer and into the fall, both from Los Azules and coming from the Fox Complex. So quite excited by that.

Thank you very much, and have a great day.

|

|

|

|

Post by Entendance on Aug 15, 2023 0:58:54 GMT -5

|

|

|

|

Post by Entendance on Aug 17, 2023 7:21:08 GMT -5

Canadian mining entrepreneur Rob McEwen said he’s weighing financing options for a copper project in Argentina, with an initial public offering possible as soon as November. |

|

|

|

Post by Entendance on Aug 21, 2023 7:44:31 GMT -5

McEwen Mining Appoints a New Director

TORONTO, Aug 21st, 2023 - McEwen Mining Inc. (NYSE: MUX) (TSX: MUX) is pleased to welcome Michelle Makori as our newest member of our Board of Directors.

Michelle is an internationally acclaimed broadcast journalist, news anchor, reporter, and producer. Currently she is the Editor-in-Chief and Lead Anchor at Kitco News, focusing on commodities and precious metals. Michelle has worked as an anchor, reporter and producer for Bloomberg, CNN Money, i24News and SABC. As an anchor and reporter, Michelle has covered and analyzed the biggest global economic, financial, and geopolitical events of the past two decades. She has interviewed heads of state, CEOs of Fortune 500 companies, and other political, business, and entertainment leaders. Michelle also serves as MC, host and panel moderator for conferences and events around the globe.

“On behalf of our Board of Directors, we are very pleased to welcome Michelle as a new Director. I look forward to working with Michelle; she brings a valuable expertise and market insights to McEwen Mining” said Rob McEwen, Chairman & Chief Owner.

ABOUT MCEWEN MINING

McEwen Mining is a gold and silver producer with operations in Nevada, Canada, Mexico and Argentina. In addition, it owns approximately 52% of McEwen Copper which owns the large, advanced stage Los Azules copper project in Argentina. Rob McEwen, Chairman and Chief Owner, has a personal investment in the company of US$220 million. His annual salary is US$1.

|

|

|

|

Post by Entendance on Aug 24, 2023 3:27:23 GMT -5

|

|

|

|

Post by Entendance on Aug 25, 2023 7:06:20 GMT -5

|

|

|

|

Post by Entendance on Aug 31, 2023 0:59:54 GMT -5

The United States is in serious trouble after exporting a record amount of gold since 2001 while domestic mine supply collapsed. This will likely go down in history as one of the United States’ biggest Blunders. More here |

|

|

|

Post by Entendance on Sept 20, 2023 4:30:56 GMT -5

|

|

|

|

Post by Entendance on Oct 3, 2023 16:51:19 GMT -5

Potential Impact: Shorter Payback, Longer Mine Life

Drillhole SM23-201: 21.6 g/t Au over 5.1 m in the Ramp Portal Zone (Fig. 2)

Drillhole SM23-308: 38.5 g/t Au over 7.4 m Down-plunge of Stock West (Fig. 1)

Drillhole SM23-281: 98.8 g/t Au over 0.9 m in Footwall Timiskaming Sediments (Fig. 3)

TORONTO, October 3, 2023 -- McEwen Mining Inc. (NYSE: MUX) (TSX: MUX) is pleased to report new assay results from the Stock Property, part of the Fox Complex near Timmins, Ontario...

|

|

|

|

Post by Entendance on Oct 11, 2023 7:23:22 GMT -5

TORONTO, Oct. 11, 2023 McEwen Copper Inc., a subsidiary of McEwen Mining Inc. (NYSE: MUX) (TSX: MUX), is pleased to announce abinding agreement for an additional $10.0 million investment by Nuton LLC, a Rio Tinto Venture, and existing McEwen Copper shareholder.

Nuton has agreed to invest US$10.0 million to acquire shares of McEwen Copper in a two-part transaction expected to close by October 19th, 2023 (the “Nuton Transaction”) consisting of a private placement of 152,615 McEwen Copper common shares, and the purchase of 232,000 common shares owned by McEwen Mining in a secondary sale. Proceeds of the subscription and purchase are expected to be approximately $4.0 million to McEwen Copper and $6.0 million to McEwen Mining, respectively. The proceeds of the private placement will be used to advance the development of the Los Azules copper project in San Juan, Argentina, and for general corporate purposes.

After closing, Nuton will own 14.5% of McEwen Copper on a fully diluted basis, and McEwen Mining will own 47.7%. The transaction values McEwen Copper at approximately US$800 million.

In connection with the Transaction, McEwen Copper and certain of its affiliates agreed to amend the Nuton Collaboration Agreement to extend the period of exclusivity over novel, trade secret or patented copper heap leach technologies until February 1st, 2025.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale would be unlawful.

About Nuton

Nuton is an innovative new venture that aims to help grow Rio Tinto’s copper business. At the core of Nuton is a portfolio of proprietary copper leach-related technologies and capability – a product of almost 30 years of research and development. Nuton™ Technologies offer the potential to economically unlock copper sulphide resources, copper bearing waste and tailings, and achieve higher copper recoveries on oxide and transitional material, allowing for a significantly increased copper production. One of the key differentiators of Nuton is the potential to deliver leading environmental performance, including more efficient water usage, lower carbon emissions, and the ability to reclaim mine sites by reprocessing mine waste.

About McEwen Copper

McEwen Copper Inc. holds a 100% interest in the Los Azules copper project in San Juan, Argentina and the Elder Creek project in Nevada, USA.

Los Azules was ranked in the top 10 largest undeveloped copper deposits in the world by Mining Intelligence (2022). Its current copper resources are estimated at 10.9 billion pounds at a grade of 0.40% Cu (Indicated category) and an additional 26.7 billion pounds at a grade of 0.31% Cu (Inferred category). A PEA published in June 2023 estimated a $2.7 billion after-tax NPV8% at $3.75/lb Cu and a 27-year mine life.

After closing the Stellantis investment, also announced today, and the pending investment by Nuton, McEwen Copper will have 30,937,615 common shares outstanding, and its shareholders are: McEwen Mining Inc. 47.7%, Stellantis 19.4%, Nuton 14.5%, Rob McEwen 12.9%, Victor Smorgon Group 3.2%, and other shareholders 2.3%.

TORONTO, Oct. 11, 2023 -- McEwen Copper Inc., a subsidiary of McEwen Mining Inc. (NYSE: MUX) (TSX: MUX), is pleased to announce the closing of an additional ARS $42 billion investment by Stellantis, one of the world’s leading automakers and mobility providers with iconic brands including Abarth, Alfa Romeo, Chrysler, Citroën, Dodge, DS Automobiles, Fiat, Jeep®, Lancia, Maserati, Opel, Peugeot, RAM, Vauxhall, Free2Move and Leasys.

Stellantis N.V. (“Stellantis”), which in February 2023 invested ARS $30 billion, has today invested an additional ARS $42 billion in Argentina to acquire shares of McEwen Copper in a private placement of 1,900,000 common shares. The proceeds of the private placement will be used to advance development of the Los Azules copper project in San Juan, Argentina, and for general corporate purposes.

Giving effect to the pending investment by Nuton LLC, also announced today, Stellantis increases its ownership to 19.4% of McEwen Copper and McEwen Mining owns 47.7% on a fully diluted basis. The Transaction values McEwen Copper at approximately US$800 million.

In connection with the Transaction, McEwen Copper and certain of its affiliates amended the Investor Rights Agreement with Stellantis (the "Stellantis IRA”) and the Copper Cathodes and Concentrates Purchase Rights Agreement (the “CCCPRA”), further described below.

The Stellantis IRA was amended to make the Carbon Neutral Commitment by 2028 not contingent on Stellantis maintaining a certain minimum ownership percentage in McEwen Copper. McEwen Copper intends to implement this commitment independent of Stellantis’ involvement in the Los Azules project.

The CCCPRA was amended to provide for a minimum 10,000 tonne per annum copper cathode offtake, subject to certain restrictions and exclusions, and further defined ‘market price’ to be paid by Stellantis on future copper cathode purchases pursuant to the CCCPRA.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale would be unlawful.

About McEwen Copper

McEwen Copper Inc. holds a 100% interest in the Los Azules copper project in San Juan, Argentina and the Elder Creek project in Nevada, USA.

Los Azules was ranked in the top 10 largest undeveloped copper deposits in the world by Mining Intelligence (2022). Its current copper resources are estimated at 10.9 billion pounds at a grade of 0.40% Cu (Indicated category) and an additional 26.7 billion pounds at a grade of 0.31% Cu (Inferred category). A PEA published in June 2023 estimated a $2.7 billion after-tax NPV8% at $3.75/lb Cu and a 27-year mine life.

After closing the Nuton LLC investment, also announced today, McEwen Copper will have 30,937,615 common shares outstanding, and its shareholders are McEwen Mining Inc. 47.7%, Stellantis 19.4%, Nuton 14.5%, Rob McEwen 12.9%, Victor Smorgon Group 3.2%, and other shareholders 2.3%.

About Stellantis

Stellantis N.V. (NYSE: STLA / Euronext Milan: STLAM / Euronext Paris: STLAP) is one of the world’s leading automakers and a mobility provider. Its storied and iconic brands embody the passion of their visionary founders and today’s customers in their innovative products and services, including Abarth, Alfa Romeo, Chrysler, Citroën, Dodge, DS Automobiles, Fiat, Jeep®, Lancia, Maserati, Opel, Peugeot, Ram, Vauxhall, Free2move and Leasys. Powered by our diversity, we lead the way the world moves – aspiring to become the greatest sustainable mobility tech company, not the biggest, while creating added value for all stakeholders as well as the communities in which it operates. For more information, visit www.stellantis.com.

Au and Ag in 2023  Gold is important to me because... Gold is important to me because...

|

|

|

|

Post by Entendance on Oct 30, 2023 6:55:24 GMT -5

McEwen Mining Inc. (NYSE: MUX) (TSX: MUX) is pleased to report production for Q3 2023 was 38,600 gold equivalent ounces (“GEOs”) and 104,800 GEOs for the nine months ended September 30th, 2023. Our consolidated production guidance for 2023 is maintained, despite the Gold Bar Mine’s production forecast being 13% below its guidance range. Our forecast for the full year 2023 (see Table 1) reflects actual productions to September 30th and management's current estimates for Q4 2023.

Gold Bar Mine, Nevada

Good progress has been made at Gold Bar recovering from a challenging first half of the year, as demonstrated by steadily increasing production quarter after quarter. Gold Bar has also maintained an excellent safety record with 1,313 days without a lost time injury as of September 30th. Crushing and stacking of ore on the heap leach pad reached a rate of 9,300 tonnes per day (tpd) in September, a major improvement over the average in the prior eight months of 6,150 tpd. Year-to-date, ore containing 41,600 ounces of gold has been loaded onto the heap leach pad with an average expected recovery rate of 68%. Due to the gold inventory on the heap leach pad, we are confident in a reasonably strong Q4 continuing into the start of 2024. The 2023 production forecast is 13% below the guidance established in December 2022, due to a combination of factors including flooding and extreme weather in the Spring and a slower leach recovery rate of Gold Bar South ore.

Fox Complex, Timmins District

Fox performed well during Q3 and it is on track to slightly exceed the mid-point of our guidance range. Fox has achieved 738 days without a lost time injury as of September 30th. Mining at Froome is on track and the Stock mill continues to increase average throughput. We are pleased with the good exploration drilling results seen at our Stock Complex including the ‘Ramp Portal Zone’, which may represent an early mining horizon for our upcoming Stock West project (see news release dated October 3rd, 2023).

San José, Argentina

San José, which is operated by our joint venture partner Hochschild Mining, delivered Q3 production in line with our expectations for the quarter and guidance for the year. San José reported one lost time injury in August 2023, the worker has since recovered and returned to regular duty.

McEwen Copper

On October 11th our McEwen Copper subsidiary announced additional investments by Stellantis and Nuton of ARS$42 billion and US$10 million, respectively. Since the creation of McEwen Copper, shareholders have invested $397 million (including investments by Stellantis in Argentine Pesos at official exchange rates at the time of each transaction) to acquire shares even though that the Company has remained private. The recent transactions occurred at $26.00 per share of McEwen Copper, giving it a market value of approximately $800 million. McEwen Mining retains 47.7% ownership of McEwen Copper, with an implied market value of $380 million, this represents a value accretion for McEwen Mining shareholders of $98 million or two (2) dollars per share since March 2023.

McEwen Copper is now well financed for the remainder of 2023 and well into 2024. The funds raised will be used to advance the feasibility study on the Los Azules project and for other corporate purposes. McEwen Mining also received proceeds of $6 million to augment its balance sheet.

Currently, we have fourteen drill rigs on site at Los Azules, scaling up to 18 drill rigs for our drilling campaign targeting more than 45,000 meters. This program will generate all the remaining data required to complete the planned feasibility study by Q1 2025.

ABOUT MCEWEN MINING

McEwen Mining is a gold and silver producer with operations in Nevada, Canada, Mexico and Argentina. In addition, it owns approximately 47.7% of McEwen Copper which owns the large, advanced stage Los Azules copper project in Argentina. The Company’s goal is to improve the productivity and life of its assets with the objective of increasing its share price and providing a yield. Its Chairman and Chief Owner has personally provided the company with $220 million and takes an annual salary of $1.

|

|

|

|

Post by Entendance on Nov 6, 2023 11:08:06 GMT -5

McEWEN MINING Q3 2023 RESULTS CONFERENCE CALL

TORONTO, November 3, 2023 - McEwen Mining Inc. (NYSE: MUX) (TSX: MUX) invites you to join our conference call following the release of our Q3 2023 financial results on Thursday, November 9th, 2023 at 11:00 AM EST, where management will discuss our financial results and project developments and follow with a question-and-answer session. Questions for the call can be emailed in advance to info@mcewenmining.com, or can be asked directly by participants over the phone during the webcast.

Q3 Results Conference Call - Thursday, November 9th, 2023, at 11:00 AM EST

Calling in:

Participant Toll-Free Dial-In Number: (888) 210-3454

Participant Toll Dial-In Number: (646) 960-0130

Conference ID: 3232920

Webcast Registration Link:

events.q4inc.com/attendee/253960288

An archived replay of the webcast will be available approximately 2 hours following the conclusion of the live event. Access the replay on the Company’s media page at www.mcewenmining.com/media.

ABOUT MCEWEN MINING

McEwen Mining is a gold and silver producer with operations in Nevada, Canada, Mexico and Argentina. In addition, it owns approximately 47.7% of McEwen Copper which owns the large, advanced stage Los Azules copper project in Argentina. The Company’s goal is to improve the productivity and life of its assets with the objective of increasing its share price and providing a yield. Its Chairman and Chief Owner has personally provided the company with $220 million and takes an annual salary of $1.

|

|

|

|

Post by Entendance on Nov 9, 2023 3:33:13 GMT -5

McEwen Mining Inc. (NYSE: MUX) (TSX: MUX) reports its results for the third quarter (Q3) and nine months ended September 30th, 2023. Operational and Financial Highlights

Consolidated GEO production in Q3 improved by 8% compared to both Q2/23 and Q3/22. We produced 38,500 GEOs(1) in Q3, and 104,400 GEOs for the nine months ended September 30th. We reiterate our consolidated production guidance is at the lower end of our range of 150,000 to 170,000 GEOs for the year (see Table 1). We continue to meet safety standards at our 100% owned operations. During Q3, we had no lost-time incidents at our Fox Complex, Gold Bar Mine, and El Gallo operations.

In Q3, our Fox Mine Complex performed well, producing 11,200 ounces (oz) gold and remains on track to meet guidance of 42,000 to 48,000 oz gold for the year. Cash costs(4) and AISC per GEO(4) sold for the Fox Complex were $1,078 and $1,288, respectively . We expect annual cash costs(4) per GEO(4) sold to be 10% above of our 2023 guidance. Figure 1 highlights the turnaround in production at Fox that has occurred since 2021.

In Q3, the Gold Bar Mine produced 9,500 oz of gold, an increase of 20% compared to Q2/23. Production continues to increase quarterly, though delays from extreme weather and labor constraints during 2023 have impacted our annual outlook. We now expect production from Gold Bar to be between 36,500 to 40,000 oz gold. Cash costs(4) and AISC per GEO(4) sold for the Gold Bar mine were $1,529 and $2,160, respectively. AISC was affected by a $4.5 million sustaining capital investment in a heap leach pad expansion, which was substantially completed during the quarter. Additional mining crews and the completion of our heap leach expansion are expected to result in increased production in Q4/23 (see Figure 2), allowing Gold Bar to quickly realize recoveries on material stockpiled during the last quarter. While this should reduce costs per ounce in the fourth quarter, we still expect the average costs for the year to be 10% to 15% higher than our 2023 guidance.

In Q3, the San José Mine produced 17,800 GEOs, an increase of 3% compared to Q2/23 due to a modest improvement in processed tonnes. Our joint venture partner and mine operator, Hochschild Mining, reiterates production guidance of 66,000 to 74,000 GEOs for the year. Cash costs(4) and AISC per GEO(4) sold for San José were $1,445 and $1,953, respectively. We expect costs to remain approximately 15% above 2023 guidance due to additional capital development costs associated with the operator’s revised mine plan.

We continue to advance our exploration program at Los Azules aiming to deliver all information required for the feasibility study. During Q3, we completed planning and preparation work for the 2023-2024 drilling campaign, which has a target of 157,000 feet (48,000 meters) and includes additional exploration, infill, geotech, hydrological and hydrogeological drilling. 14 out of a total of 18 to 20 planned drill rigs are currently operating and we have drilled 19,600 feet (6,000 meters) to date. We invested $18.5 million in our Los Azules copper projectduring Q3 primarily to build a winter camp, further improve our road access, and to construct a logistics facility in San Juan.

Subsequent to the quarter end, McEwen Copper closed financings with Stellantis and Nuton, a Rio Tinto Venture, raising ARS$42 billion (Argentine Pesos) and $10.0 million, respectively, at a price of $26 per share, which implies a market value of $800.0 million for McEwen Copper. As part of these private placements, McEwen Mining received $6.0 million from the sale of 232,000 McEwen Copper common shares. McEwen Copper’s share ownership structure is now: McEwen Mining 47.7%, Stellantis 19.4%, Nuton 14.5%, Rob McEwen 12.9% and 5.5% other shareholders. The implied market value represents a value accretion of $207 million for McEwen Mining (from $175 million to $382 million of implied ownership value), representing a value of $7.48 per fully diluted McEwen Mining share.

Consolidated cash and cash equivalents were $49.1 million (of which $47.5 million is to be used towards advancing the Los Azules copper project) and consolidated working capital $72.3 million as of September 30, 2023. We also reported investments of $40.8 million, which consist of liquid securities held in Argentina to mitigate inflation and devaluation risks.

In Q3, we reported a gross profit of $3.8 million and cash gross profit(4) of $11.9 million from our 100% owned precious metal operations , compared to a gross profit of $1.5 million and cash gross profit(4) of $5.8 million in Q3/22. Higher revenues driven by a 34% increase in GEOs sold and a 10% increase in realized gold prices led to improvements in gross profit and cash gross profit(4). Including our 49% ownership of the San José Mine, we reported a total cash gross profit(4) of $22.3 million compared with a total cash gross profit(4) of $13.8 million in Q3/22.

In Q3, we reported a net loss of $18.5 million, or $0.39 per share, compared to a net loss of $10.5 million, or $0.21 per share in Q3/22. Compared to our gross profit, our net loss was the result of higher year-over-year exploration and advanced project expenditures, including an $18.5 million investment in exploration activities at our Los Azules copper project.

In Q3, we reported an adjusted net loss(4) of $4.2 million compared to an adjusted net income(4) of $6.4 million in Q3/22. Adjusted net loss(4) excludes the expenses of McEwen Copper and our interest in the San José mine, a metric that we believe best represents the results of our 100% owned precious metal operations. Compared to our cash gross profit(4) of $11.9 million, the adjusted net loss(4) includes $6.6 million in exploration and advanced project expenditures at our Fox Complex, Gold Bar mine and Fenix Project operations, $8.5 million in non-cash depreciation, and $3.7 million in general and administrative expenses.

Revenues of $38.4 million were reported from the sale of 20,620 GEOs from our 100% owned operations at an average realized price(4) of $1,920 per GEO . Including our 49% ownership of San José Mine, Q3 revenue would have increased by $31.6 million. This compares to Q3/22 revenues of $26.0 million from the sale of 15,400 GEOs from our 100% owned operations at a realized price of $1,742 per GEO. Including our 49% ownership of San José Mine, Q3/22 revenue would have increased by $32.0 million.

It is important to note that because of the recent McEwen Copper financing, MUX’s ownership in McEwen Copper is below 50%, and we expect to no longer consolidate the financials of McEwen Copper. From Q4/23 onward we expect to begin to account for McEwen Copper as an equity investment . The Company expects to conclude soon on the accounting impacts of our recent financing. The resulting impact on our financials on a go-forward basis, should McEwen Copper be deconsolidated, will be noticeable. Specifically, the carrying value of our investment in McEwen Copper ownership may increase significantly in line with the recent financings, and we expect that our cash and liquid assets and expenses will decline markedly.

Webcast

A webcast will be held on Thursday, November 9th, 2023 at 11:00 AM EST, where management will discuss our financial results and project developments and follow with a question-and-answer session. Questions for the call can be emailed in advance to info@mcewenmining.com, or can be asked directly by participants over the phone during the webcast.

Q3 Results Conference Call - Thursday, November 9 th , 2023, at 11:00 AM EST

Calling in: Participant Toll-Free Dial-In Number: (888) 210-3454

Participant Toll Dial-In Number: (646) 960-0130

Conference ID: 3232920

Webcast Registration Link:

events.q4inc.com/attendee/253960288

An archived replay of the webcast will be available approximately 2 hours following the conclusion of the live event. Access the replay on the Company’s media page at www.mcewenmining.com/media.

Table 1 provides production and cost results for Q3 & 9M 2023 with comparative results for Q3 & 9M 2022 and our Forecast and Guidance for 2023. Our Forecast for 2023 reflects production to September 30th and management's current estimates for Q4 2023. Notes:

(1) Gold Equivalent Ounces (GEOs) are calculated based on a gold-to-silver price ratio of 90:1 for Q3 2022, 83:1 for 9M 2023, 82:1 for Q3 2022, and 83:1 for 9M 2022. 2023 production guidance is calculated based on an 85:1 gold-to-silver price ratio.

(2) The San José Mine is 49% owned by McEwen Mining Inc. and 51% owned and operated by Hochschild Mining plc. Production is shown on a 49% basis.

(3) El Gallo Mine (on care and maintenance) is expected to recover 2,300 oz gold in 2023 from plant and pond cleanout.

(4) See disclosure below about Non-GAAP Financial Performance Measures used in this release.

(5) Production figures may not add due to rounding.

Figure 1 below shows the Fox Mine Complex actual annual production 2018-2022 and the 2023 forecast.

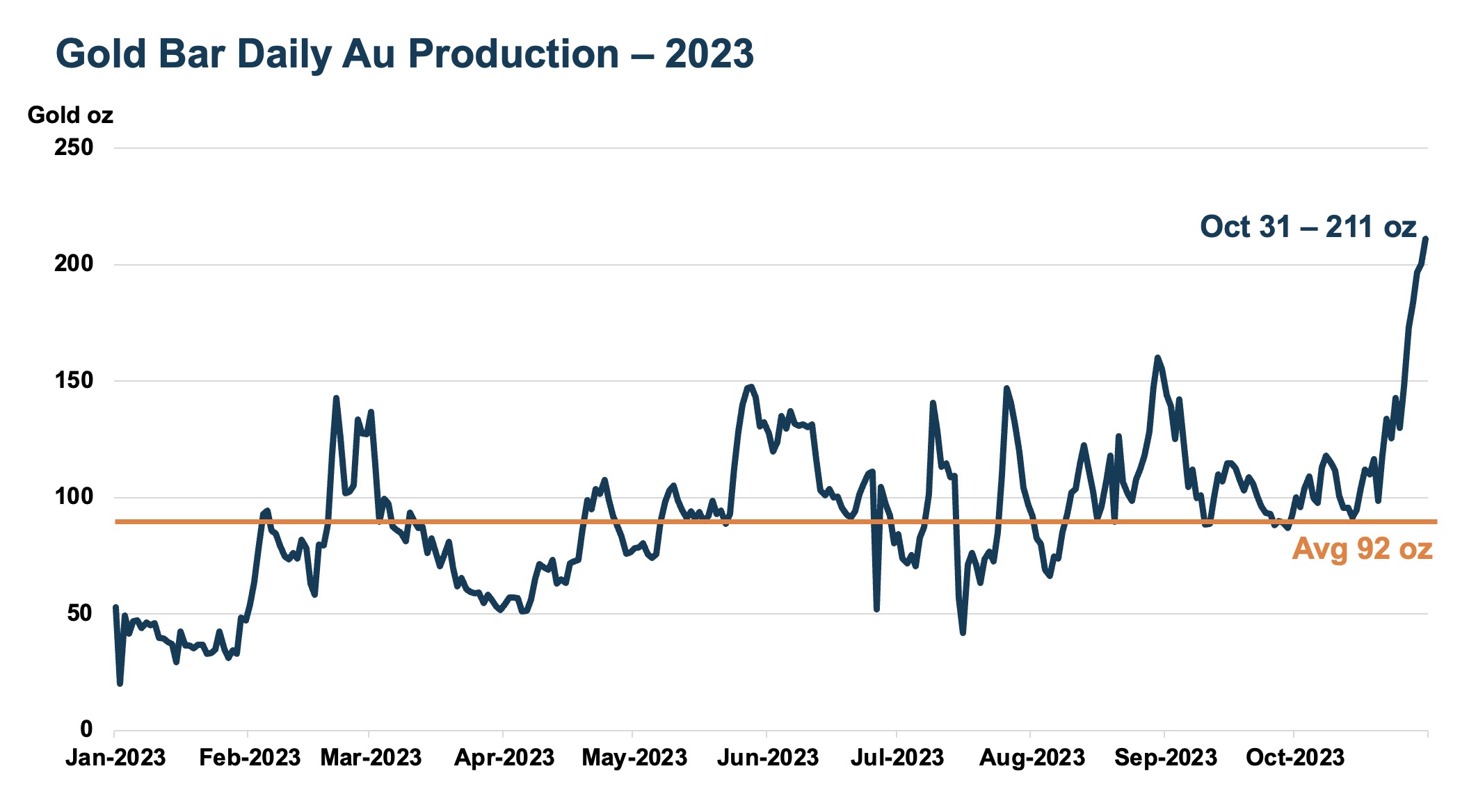

Figure 2 below shows Gold Bar Mine’s daily ounces processed through the process plant from Jan 1, 2023 to Oct 31, 2023.

Financial Statements and MD&A refer to: www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0000314203

Technical Information The technical content of this news release related to financial results, mining and development projects has been reviewed and approved by William (Bill) Shaver, P.Eng., COO of McEwen Mining and a Qualified Person as defined by SEC S-K 1300 and the Canadian Securities Administrators National Instrument 43-101 "Standards of Disclosure for Mineral Projects."

Reliability of Information Regarding San José

Minera Santa Cruz S.A. (“MSC”), the owner of the San José Mine, is responsible for and has supplied to the Company all reported results from the San José Mine. McEwen Mining's joint venture partner, a subsidiary of Hochschild Mining plc, and its affiliates other than MSC do not accept responsibility for the use of project data or the adequacy or accuracy of this release.

NON-GAAP FINANCIAL PERFORMANCE MEASURES

We have included in this report certain non-GAAP financial performance measures as detailed below. In the gold mining industry, these are common performance measures but do not have any standardized meaning and are considered non-GAAP measures. We use these measures in evaluating our business and believe that, in addition to conventional measures prepared in accordance with GAAP, certain investors use such non-GAAP measures to evaluate our performance and ability to generate cash flow. Accordingly, they are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with GAAP. There are limitations associated with the use of such non-GAAP measures. We compensate for these limitations by relying primarily on our U.S. GAAP results and using the non-GAAP measures supplementally. We do not provide a reconciliation of forward-looking non-GAAP financial measures to their most directly comparable GAAP financial measures on a forward-looking basis because we are unable to predict items contained in the GAAP financial measures without unreasonable efforts.

The non-GAAP measures are presented for our wholly-owned mines and the San José mine. The GAAP information used for the reconciliation to the non-GAAP measures for the San José mine may be found in Note 9, Investment in Minera Santa Cruz S.A. (“MSC”) – San José Mine. The amounts in the tables labeled “49% basis” were derived by applying to each financial statement line item the ownership percentage interest used to arrive at our share of net income or loss during the period when applying the equity method of accounting. We do not control the interest in or operations of MSC and the presentations of assets and liabilities and revenues and expenses of MSC do not represent our legal claim to such items. The amount of cash we receive is based upon specific provisions of the Option and Joint Venture Agreement and varies depending on factors including the profitability of the operations.

The presentation of these measures, including those for MSC, has limitations as an analytical tool. Some of these limitations include:

The amounts shown on MSC’s individual line items do not represent our legal claim to its assets and liabilities, or the revenues and expenses; and

Other companies in our industry may calculate their cash gross profit, cash costs, cash cost per ounce, all-in sustaining costs, all-in sustaining cost per ounce, average realized price per ounce, and liquid assets differently than we do, limiting the usefulness as a comparative measure.

Adjusted Net Income or Loss and Adjusted Net Income or Loss Per Share

Adjusted net income or loss is a non-GAAP financial measure and does not have any standardized meaning. We use adjusted net income to evaluate our operating performance and ability to generate cash flow from our wholly-owned operations in production; we disclose this metric as we believe this measure provides valuable assistance to investors and analysts in evaluating our ability to finance our precious metal operations and capital activities separately from our copper operations. The most directly comparable measure prepared in accordance with GAAP is net income or loss. Adjusted net income is calculated by adding back McEwen Copper and MSC’s income or loss impacts to our consolidated net income or loss...

|

|

|

|

Post by Entendance on Nov 9, 2023 13:43:47 GMT -5

McEwen Mining Inc. (NYSE:MUX) Q3 2023 Earnings Conference Call November 9, 2023 11:00 AM ET

Company Participants

Rob McEwen - Chairman, Chief Owner

Perry Ing - Chief Financial Officer

William Shaver - Chief Operating Officer

Michael Meding - Vice President, General Manager, McEwen Copper

Jeff Chan - Vice President, Finance

Carmen Diges - General Counsel and Secretary

Stefan Spears - Vice President, Corporate Development

Conference Call Participants

Marcus Giannini - H.C. Wainright

Jake Sekelsky - Alliance Global Partners

Joseph Reagor - Roth MKM

John Tumazos - John Tumazos Very Independent Research

Rob McEwen

Thank you, operator. Good morning fellow shareholders and guests. Welcome to our Q3, 2023 conference call. The individuals you all heard on the call with me will be participating in our question-and-answer period.

I'm going to start by highlighting our share performance over the past 13 months, from September 1, 2022 to present. I picked that date because that is when the market began to see the value of our strategy to finance our McEwen Copper assets separately. Since that time, our share price has increased 133% and has far outperformed the performance of the Dow Jones Industrial Average, NASDAQ, the price of gold, price of copper, and the ETFs of GDX and GDXJ, representing the gold sector.

I believe our superior share performance has been driven by the success we have achieved financing our subsidiary, McEwen Copper, where we have raised privately equity of close to US$400 million during this period.

Recognizing the impressive size and value of McEwen Copper's Los Azules project are two global giants, who have provided three quarters of these funds. Stellantis, the world's fourth largest car manufacturer, and Rio Tinto, the world's second largest mining company, through its Nuton Venture arm.

With the end of winter in the southern hemisphere, we are back up at Los Azules and moving aggressively to complete all the activities necessary to deliver a feasibility study in the first quarter of 2025.As a result of the latest financing, the implied value of McEwen Copper has increased to $800 million, which gives McEwen's 47.7% ownership interest a value of $382 million, which translates into a value of $7.48 per fully diluted share of McEwen Mining.

I expect our investment in McEwen Mining will continue to grow in value as we advance our large Los Azules project and the demand for copper increases. McEwen Copper is one of our assets. The others are gold and silver mines and a portfolio of five royalties.

I believe these assets represent considerable underlying value. The range of our estimated value per share is from $9.32 a share to $29.17 a share, and our share price is currently trading around $7.20 a share. Details of these calculations can be found on our website under our latest corporate presentation.

I believe our next performance driver will be our gold and silver mines. After enduring a very challenging three years, we are seeing very encouraging signs that the fortunes of these operations are finally turning around. Production is increasing at all three of our mines, and it appears that we could achieve the low end of the range of guidance we gave for production this year of just over 150,000 ounces of gold equivalent.

Regarding cost per ounce, we expect the Fox Mine Complex should deliver within our guidance range, while Gold Bar and San Jose are likely to come in 10% to 15% over the cost guidance we've given. Gold Bar had a particularly difficult nine months. However, this quarter we are putting on a big push to drive up production, and that would result in lower cost per ounce.

You might ask, what are these encouraging signs? At the Fox Mine, annual gold production in 2020 had fallen to 24,400 ounces. Since then, it has increased steadily, and we are expecting to reach 45,500 ounces by year end, an improvement of 86%. At the Gold Bar Mine, daily gold production was a meager 50 ounces at the start of the year. But as the year progressed, the daily gold recovery increased and has averaged year-to-date 92 ounces. And in late October, it really began to accelerate, and by month end it was over 210 ounces, and has continued to climb higher since then.

These improvements are a very welcome change, but our share price still has a long way to climb before many of you and myself get back to our cost. I believe the combination of the advancement of Las Azulas, the improving operating performances of our mines, and our continuing exploration efforts will continue to lift our share price, hopefully to the levels we were all expecting when we invested.

Many of you have asked the very important question, when will we make a profit? I'm sorry to say, I'm unable to give an exact date, but this might surprise you. It could be as early as year-end. Our Fox and San Jose mines are now generating positive cash flow, and Gold Bar is expected to generate positive cash flow this quarter. Our expenses have been large for two principal reasons. One, we've been consolidating the financials of McEwen Copper and its Las Azulas project, where exploration and development expenses are high.

In addition, we have invested heavily in exploration at Fox and at Gold Bar, a major leach pad expansion and exploration expenses represented more than $200 an ounce just in the third quarter.

Starting this quarter, our financial statements are likely to change significantly. We expect to be no longer consolidating McEwen Copper's financials due to our ownership interest dropping below 50% as a result of the recent McEwen Copper financing. The impact will significantly lower our cash balance, our total expenses, and produce a large unrealized capital gain that will be reflected in both our income statement and balance sheet.

Recently, we put out a press release that we filed a new base shelf prospectus, and we've had some calls this morning and yesterday. Are we going to do an issue? I want to emphasize that this is not an offering prospectus. We, like most other companies, routinely file these base prospectus just to provide updated information, to put us into a position where we could react if we saw an opportunity, and we've done this in the past every few years with a similar base shelf prospectus.

I think the market right now is a very attractive market to be looking for opportunity, and we will continue to do so. The price is right. We were established to grow, but the prior year's challenges effectively put any consideration of that on hold. Today, the timing is right, and we want to be positioned to act defensively.

Marcus Giannini, H.C. Wainright

Hi, Rob and team. This is Marcus Giannini calling in for Heiko. Thanks for taking our questions.

Rob McEwen

Happy to.

Marcus Giannini

So, at Gold Bar, you stated in your release that costs increased due to delays from extreme weather and labor constraints during 2023, and then you expect the average cost for the year to be 10% to 15% higher than your guidance. Given these projections, how much of these increases do you view as, say, transitory, and how much of this should we model into 2024? And can you provide any color on the different factors contributing to these expected increases?

Rob McEwen

Bill, would you like to handle that?

Bill Shaver

Yeah, sure. Thanks very much for the question. Yeah, we expect going into 2024 that we will be at or below the guidance that we gave for this year for the following reasons. This year we have spent about $5 million on exploration drilling, and that will continue into next year, probably at about that same value.

But this year we also built a new leach pad, which was completed about two or three weeks ago, at a cost of about $7 million. And so that has – those two things have plus or minus $200 impact on our cost per ounce.

So, the pad is finished. It was finished basically in the scheduled amount of time and was completed on budget. And as well, if you remember, we changed contractors at the end of 2022. And so the ramp up early in the year was challenging, in part because of the weather and so on.

But now our contractor is doing very well. Their production numbers are higher than required. And the amount of material that we're putting onto the old leach pad is now approximately 6,000 tons per day. And we're also putting 4,000 tons a day onto the new leach pad, where we have permission at this point to put material on the pad, but we still don't have permission to put cyanide onto that pad. But we anticipate getting that permit this week or next week.

And basically, so we see the production of gold going to increase for sure for the next two months and hopefully carry on into the New Year. As Rob mentioned earlier, we're basically at something like plus 200 ounces per day right now. So we're looking for, in the range of 6,000 ounces per day or per month for the next couple of months.

And I guess we anticipated that that would have started earlier, but we started the construction on a new leach pad late, because of the winter weather from last winter. And we finished it in exactly the amount of time that we said we would, but it was a month late. So rather than the gold production popping up in October, it hasn't happened until while the last couple of days of October and now November and December. So that kind of explains what the situation is going to look like going forward.

Production of funds in good shape, and so we should have a reasonable start to the year next year.

Marcus Giannini

Okay. Yeah, no awesome, that was great. And then just one quick follow-up regarding Los Azules, given that $18.5 million spent this quarter, can you maybe provide some color on where you see this figure trending over the next few quarters? Are there any additional, big ticket items, apart from the feasibility work and drilling?

Rob McEwen

Mike, would you like to answer that?

Michael Meding

Yeah, sure. So the majority of the cost will be mainly on drilling. We have a very comprehensive campaign. We aim to drill more than 48,000 meters. We already have 14 rigs mobilized and will scale up to more than 18. So that is the driver of investment in Los Azules.

Marcus Giannini

Okay, perfect. Yeah, that's it for me. Thanks a lot, guys.

Jake Sekelsky, Alliance Global Partners

Hey, Rob and team. Thanks for taking my questions.

So it looks like costs at Fox were lower in the quarter as the turnaround's taking hold. I'm just curious, is this related mainly to the grade profile or do you think this $1,300 an ounce level is something you can expect going forward?

Rob McEwen

Bill?

Bill Shaver

So yeah, I mean, as you probably know, we've increased the production at the Fox Complex from something like 950 tons a day up to now closer to say 1,275. And maybe even a little bit more than that right now. We're up closer to 1,400 tons a day.

And I guess we did have a few issues with some stoke sequencing where the grade wasn't quite behaving itself, nothing extreme. But – so as we, we expect the grade to be in the back up into the four gram range as we move forward here. So the production for the last quarter – well, as we've gone through the whole year, every quarter we improved the production. So we're in a position now where we think the production going into next year will look pretty much like the last quarter.

Jake Sekelsky

Okay, that's helpful. And then, Rob, you touched on the M&A landscape a bit towards the end of your remarks. Obviously, valuations have come down across the board, whereas you've held up pretty well in a difficult market. I'm just curious, if you expect to take a proactive approach here, if the right opportunity pops up or if you feel that you have your plate full right now? Any thoughts there would be helpful.

Rob McEwen

I'd like to see our currency value a little better and share price before acting. But in terms of the market environment, I think it's offering terrific value, particularly in the junior and in the explorer space. It's just, we've seen these cycles before, and this just looks like we're getting ready for a big run up in the price of gold, and it's good to be looking for opportunity to get a larger mass.

Jake Sekelsky

Makes sense, and I couldn't agree more there. Thanks again, guys.

Joseph Reagor, Roth MKM

Hey, Rob and team. Thanks for taking my questions.

So, kind of following on what Jake just asked, should we look at it like, you guys would be looking for a certain type of asset, whether it be early stage exploration that's highly promising or something that's late stage that's in permitting. Where is your thoughts there?

Rob McEwen

That's a good question. Well, one, we're contemplating and looking, because we feel our assets are starting – they've turned around, and we have a more stable, solid base to push off from. I think if one's looking, we could use more cash flow, probably a producer or someone who's, I think, more attractive space would be someone who's got a permit, so you don't have to worry about the time delays. It isn't going to cost a lot of money to put into production, and has some good exploration potential.

Joseph Reagor

Okay, fair enough. And then…

Rob McEwen

Probably within the Americas.

Joseph Reagor

Yeah, fair thing to add there. And then looking at the balance sheet, so if we ex out the cash that's in McEwen Copper, you got $6 million in to start the quarter. Do you feel comfortable with that, call it $7 million to $8 million level of cash moving forward? Is there like a certain minimum you guys would like to maintain? Or is there room there to add, say, flow through or something like that in the future to keep advancing projects like stock?

Rob McEwen

We expect our cash balance to grow during the quarter considerably. Flow through, in that we always have exploration. That might be a consideration going forward, just as a way of – an inexpensive way of exploring.

Joseph Reagor

Okay, and if the cash balance does grow a bit for the McEwen parent company, like is there a certain level you'd like to maintain once you get above it, going forward to just provide the proper financial flexibility quarter-to-quarter?

Rob McEwen

That will be very dependent on the market, our share price? We think it's undervalued at the moment, so not keen to release many shares into an environment like this.

Joseph Reagor

Fair enough. All right, thanks for the color, Rob. I'll turn it over.

John Tumazos, Very Independent Research

Congratulations on all the different progress, especially in Argentina. Rob, how do you think Los Azulis is going to transition from the equity placement stage with a consortium of shareholders and McEwen Mining running the exploration project to one of those great big company mine operators?

You know how they like to get presents from their suppliers and act like they are in command. How long do you expect that McEwen will continue to run the exploration project? And when is the right time to let one of those great big beasts tell you what to do?

Rob McEwen